This is the second part of a summary of a Fannie Mae sponsored analysis by the Urban Institute (UI) of the role home equity could play in retirement security. The study utilized longitudinal data from the bi-annual National Institute on Aging's Health and Retirement Study (HRS) survey for the years 1998 through 2012.

In the first part of the summary UI explained that, despite ups and downs in the economy, households over the age of 65 have more equity than in 1998 but they also have more home debt, both in the number of seniors with debt and the balance of that debt. Loan-to-value ratios also tend to be higher than in earlier generations.

There are several ways homeowners can tap into their equity; a home equity loan, referred to here as a second mortgage, a home equity line of credit (HELOC), a cash-out refinance, or a reverse mortgage. They can also sell their home, purchase a less expensive home or rent, and pocket the net proceeds.

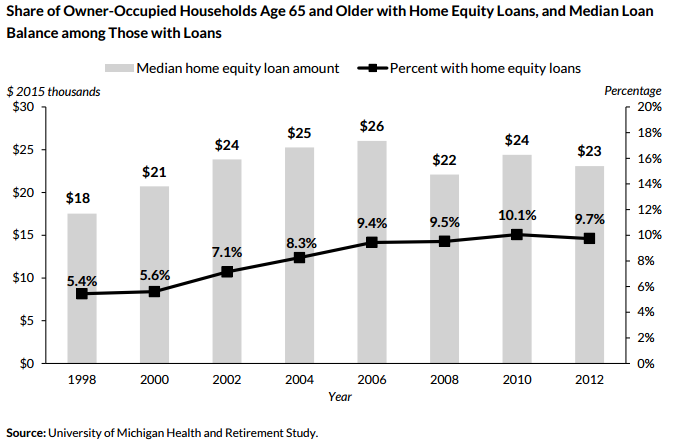

The proportion of owner-occupied households age 65 and older who withdrew equity from their home through home equity loans or HELOCs increased from 5.4 percent in 1998 to 9.7 percent in 2012 while the median loan balance increased from $18,000 to $23,000. The authors cite other studies that suggest the numbers might be higher if more homeowners correctly estimated the value of their equity.

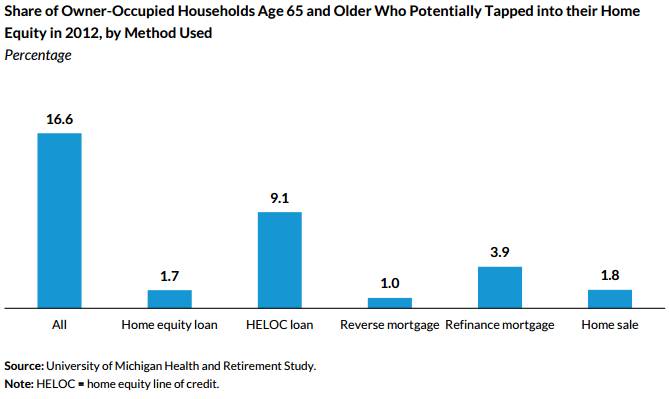

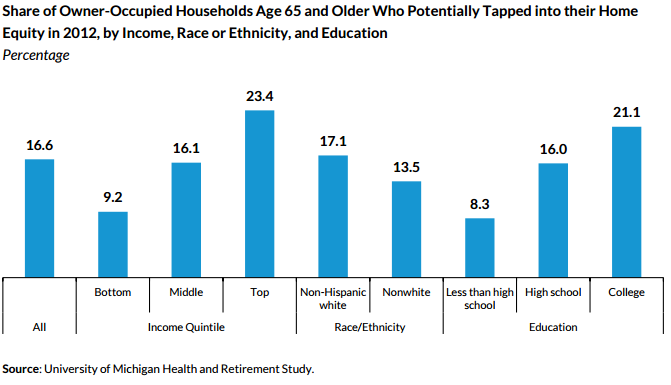

HRS data allows the UI analysts to observe households tapping into their home equity through refinancing or selling their home, but unless there is a second mortgage or a HELOC balance, they cannot be certain equity was withdrawn. With this in mind, the study concludes the 9.7 percent above increases to 16.6 percent if those other ways of tapping equity are factored in. Nine percent of households borrowed against their HELOC, 3.9 percent refinanced their mortgage, 1.8 percent profited from the sale of their home, 1.7 percent took out a second mortgage, and 1 percent took a reverse mortgage.

The median balance among older households with home equity loans was $27,000 in 2012. Among those who borrowed against their home equity lines of credit, the median balance was $24,000, and among those who made money off the sale of their homes, the median profit was $97,000.

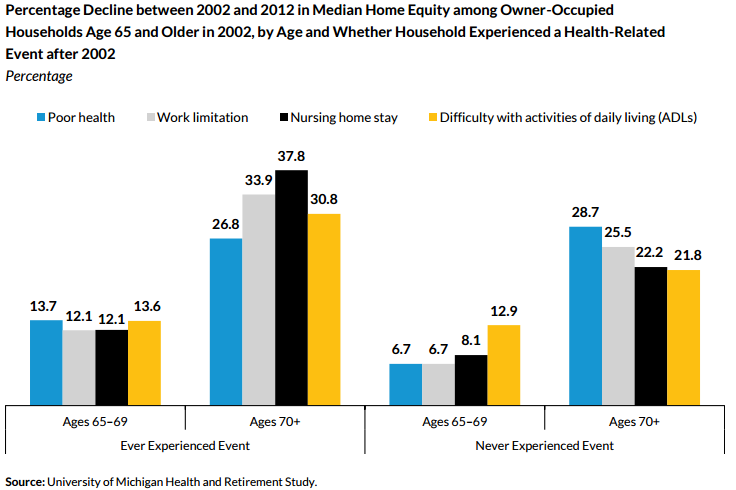

The data does not provide the reasons homeowners tapped into their equity but study authors, Barbara A. Butrica a UI senior fellow and economist, and Stipica Mudrazija a research associate, established some correlations by observing households from 2002 to 2012 to see how their home equity changed with and without occurrence of a health-related event. They identified households where a HRS survey respondent or spouse reported a nursing home, the onset of poor health, a work-limiting condition, or an activity of daily living (ADL) impairment. They limited their sample to households that owned homes in 2002 and were without any of these events in that year. They also analyzed households aged 65 to 69 in 2002 and those 70 and older as separate groups.

While median equity values diminished over the 10-year period for all owner-occupied households, there were greater losses among the oldest households and those with a health-related event. In the younger group, median equity was down 12.1 percent for those with a work-limiting condition but only 6.7 percent for those without. In the older group equity fell by one-third with such an event, and by only 25.5 percent without.

While there may be other reasons for equity to shrink, falling home prices during the recession for example, the authors say the differences between those experiencing or not experiencing health events suggest that these events may have triggered home equity withdrawals.

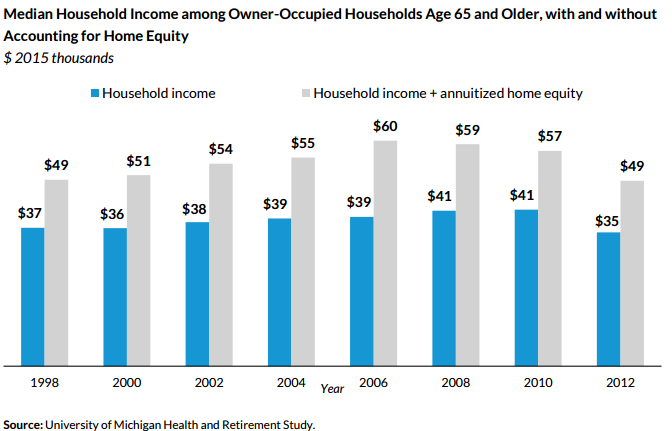

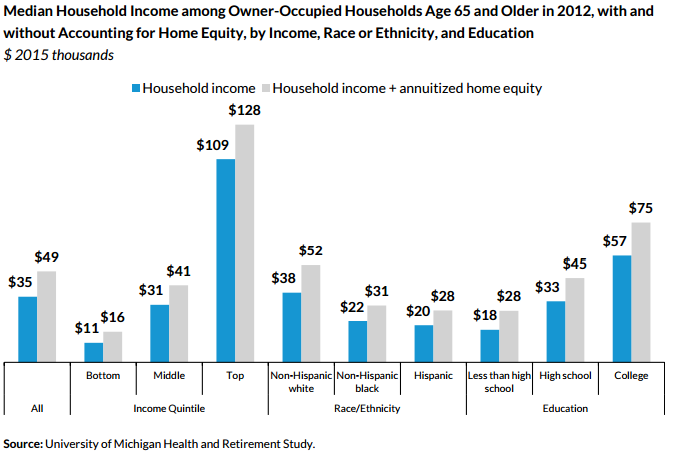

The level of equity most older homeowners, even those with housing debt, have amassed provides a last resort option which homeowners could liquidate rather than tap to improve retirement incomes. U.I looked at the potential value home equity could provide to retirement security if a home were sold and the equity annuitized net the cost to rent. The estimates assume a home sale at market value with all equity annuitized and without any fees.

At the 2006 housing peak homeowners could have increased their incomes from $39,000 to $60,000, 54 percent. Even in 2012, the market bottom, such a procedure would have increased incomes 40 percent, from $35,000 to $49,000.

Patterns of home equity and the potential security it might provide vary widely by income, race, ethnicity, and education. In general minority and low-socioeconomic-status homeowners amassed the least equity in their homes, but it represented nearly all their wealth. For example, non-Hispanic white (white) households had median home equity values ($134,000) that were nearly twice those of non-Hispanic blacks (blacks) ($72,000) and Hispanics ($77,000). Yet home equity was only 46.7 percent of total net wealth for whites. In contrast, home equity represented 86.8 percent of total net wealth for blacks and 88.6 percent for Hispanics.

Only about one-quarter of the lowest income households had housing debt in 2012, compared with almost half of those with the highest incomes. Among those with debt, the median lowest-income household owed $49,000; while the highest owed $120,000. There were similar patterns for education levels but differences by race and ethnicity are less pronounced, with white, black, and Hispanic owner-occupied households all having housing debt in the mid-30 percent range. The typical amount owed was $82,000, $65,000, and $82,000 respectively.

Minorities and those with lower socioeconomic status are also more likely to be overextended. Among owner-occupied households with housing debt, nearly one-quarter with lower income, one-third of black households, one-quarter of Hispanic households, and one-quarter of those without high school diplomas had LTV ratios of at least 80 percent in 2012.

Non-minority and college educated older households were more likely to potentially tap into their home equity than the other households. High-income households more than twice as likely as low-income households to utilize any of the methods to draw on equity, 23.4 versus 9.2 percent even though, in general, minority and low-socioeconomic-status homeowners would gain more by doing so. Owner-occupied households age 65 and older could increase their incomes 45 percent among those in the lowest income group and 56 percent among those without high school diplomas. Those with the highest income would see a 17 percent gain and those with college degrees 32 percent. Nonetheless, older homeowners with low incomes, who are black or Hispanic, or who lack high school diplomas would have median incomes dramatically lower than their counterparts, even accounting for their homes.

In their concluding analysis the authors say that many retirement experts argue that the conventional three-legged stool of retirement resources-Social Security, pensions, and savings-is incomplete because it ignores a home which the majority of older adults, regardless of income, race and ethnicity, and education, are more likely to have.

But the prospects for many of being able to access home equity diminished substantially after the Great Recession and the 54 percent increase in income homeowners might have realized pre-recession had slid to 40 percent by 2012 because of lower home values and mounting home debt. That however has improved over the last two years as the median price of a home has increased by 3 percent.

Financial prospects depend on housing debt as well, and although the share of all Americans with underwater mortgages declined from 31.4 percent in 2012 to 13.1 percent in 2015, the report noted earlier that older adults have been increasingly indebted and increasingly leveraged, especially low-income and black households.

If these trends continue retirement security will increasingly depend on retirees having enough income and assets to pay for basic living expenses and to service their debt. In fact, a 2013 study found evidence that older adults deal with indebtedness by delaying retirement and claiming their Social Security benefit. They also found that mortgage debt consistently has a stronger effect on labor supply and Social Security receipt than credit card or other debt.

Ideally, the authors say, older adults would pay off their debts well before retirement age. Accordingly, it is important to identify those who are financially fragile, to better understand their circumstances, and to look for ways to help dig them out of debt before retirement. Financial education and stricter regulations for lending institutions are among the ways that policymakers might help achieve this goal.