The Bureau of Labor Statistics dumped a bucket of ice water on the market this morning when it released the June Employment Situation Report

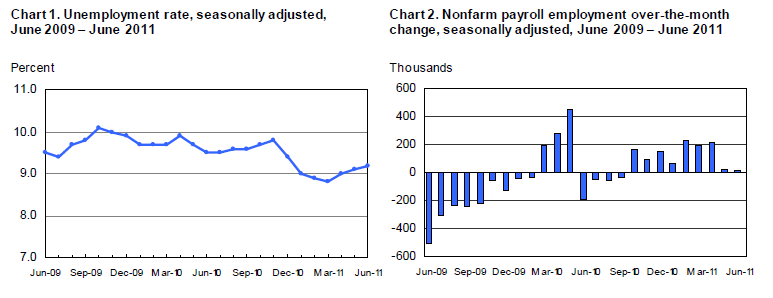

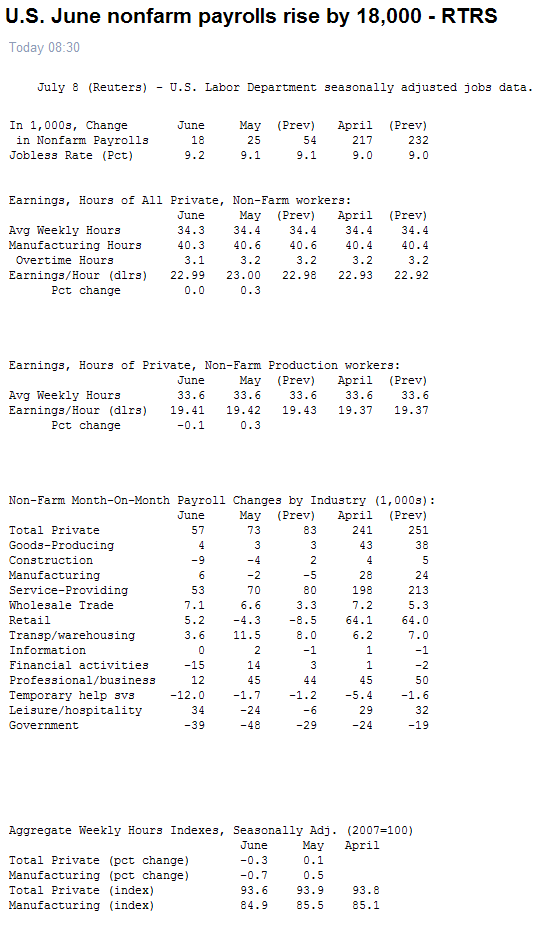

From the Release: "Nonfarm payroll employment was essentially unchanged in June (+18,000), and the unemployment rate was little changed at 9.2 percent, the U.S. Bureau of Labor Statistics reported today. Employment in most major private-sector industries changed little over the month. Government employment continued to trend down."

Plain and Simple: The market was not expecting "essentially unchanged", it was expecting nonfarm payroll employment to grow by 90,000 jobs. Instead it got +18,000 jobs and 34,000 in negative revisions to previous months' data, which totally erases June's lackluster improvement gains more. Private industry, the main driver of job creation, put up 57,000 new positions in June vs. forecasts for 110,000 while government trimmed payrolls by 39,000 heads (57,000 - 39,000 = 18,000 total). Employment in both state government and local government has been falling since the second half of 2008. For the working folk in private industry, hourly earnings barely budged (22.99 vs. 23.00 in May) but the work-week shortened up by 0.1 hours, which ultimately eats away at paychecks when the cost of living isn't improving quite fast enough to motivate splurge spending (thanks to food prices). Now for the really uninspiring statistics, the household survey. The unemployment rate rose slightly from 9.1% to 9.2% but would have risen much more if 272,000 had said they were "unemployed" instead of leaving the labor force (MORE EXPLANATION). Interesting observation here, the labor force shrinking by 272,000 is the exact of opposite of the 272,000 expansion seen in May. So anyone who thought now was a good time to get a job quickly found out that is not the case! HERE IS THE UGLIEST STAT OF 'EM ALL: The number of people who've been jobless for longer than 27 weeks increased by 89,000 to 6.29 million, which equates to 44.4% of the unemployed. Don't focus on the month over month changes though, what's important is the number of Americans, over 6 million, who have lost their job and haven't found another one. These workers are being left behind and are weighing on the broader recovery, something we fully expect the Republican party to focus on in their 2012 election campaign. It's tough to find positive news in this jobs report. Following gains averaging 215,000 per month from February through April, employment has been essentially flat for the past 2 months. At least we're still adding jobs...not losing them, albeit at a frustratingly slow pace. This is an indication that our economic recovery is facing stronger headwinds than anticipated as we cross into the 2nd half of the year.

Market Reaction...

As one might expect. Stocks sharply lower. Bonds rally. A lot.

S&P futures have fallen more than 1.50% and look ready to trade even lower. The benchmark 10-yr note yield dove from 3.184% all the way down to 3.027%. The 2s/10s curve flattened 4bps to 263bps wide. Fannie Mae 4.0s rallied 20/32 higher to 100-20. And although mortgages are lagging, a noticeable shift "down in coupon" is in progress within the MBS coupon stack, a positive as "rate sheet influential" MBS do their best to keep up with the flight to safety/short squeeze in benchmarks (duration needs, speculative relative value traders who await a convexity vortex).

On Wednesday we explained why Fibonacci Retracements play such a big role in our predictive process and provided a real-time example of those powers in progress. This is what we wrote, "Check out the chart below. It's the Fannie Mae 30yr 4.0 MBS coupon. Notice how prices seem to gravitate towards and change direction near Fibonacci support and resistance levels. Holding above 100-00 is a short-term goal. Breaking and holding 100-18 (23.6% retracement) is post-jobs data objective (10-20 days)"

Well, jobs data is out and we're on our way toward meeting a major short-term objective. Fannie 4.0s are currently bid above 100-18. Holding this level would be an encouraging development...

This report goes a long way in supporting our "lower rates by the end of the summer" outlook, but we're not looking for 10s to rally through 3.00% resistance today, not with $66 billion in 3/10/30yr auctions next week. Short sellers are gonna push back....

Regarding rate sheets, secondary will be slow to pass along loan pricing improvements. August FNCL 4.0 prices aren't high enough to warrant wide-spread pipeline hedging yet. Desks just want to get their loans in progress closed and shipped. We'll need FNCL 4.0s to venture into the 101 price handle before rebate really improves....

PS. The unofficial real unemployment rate (U-6), which includes discouraged and marginally attached workers, rose from 15.8% to 16.2% (add 2.7 million people to the "unemployed" category).