The monthly Employment Situation Report was expected to be the market's main focus last week, instead plunging commodities prices stole the show and put the sensitive state of the domestic economic recovery back in the spotlight.

The NYMEX light crude oil contract last week fell from a high of $114.83 all the way down to $94.63 amidst growing concerns that rising food and energy prices would slow the overall economic recovery and force the Fed to leave overnight interest rates near zero for longer than originally anticipated. Benchmark interest rates illustrated that sentiment as a forced bond rally (short covering) flattened the yield curve and pushed mortgage rates to their lowest levels since early December. SEE CHART. READ MORE: MBS Ledge: Shift in Production Coupon Potentially in Progress

The 10yr note went out under 3.15% and the FNCL 4.5 MBS coupon finished Friday's session +1/32 at 103-16. Benchmarks 10s begin the week slightly higher but most of last week's gains remain in tact. 10s are currently -4/32 at 103-27 yielding 3.164% and the FNCL 4.5 is -1/32 at 103-15.

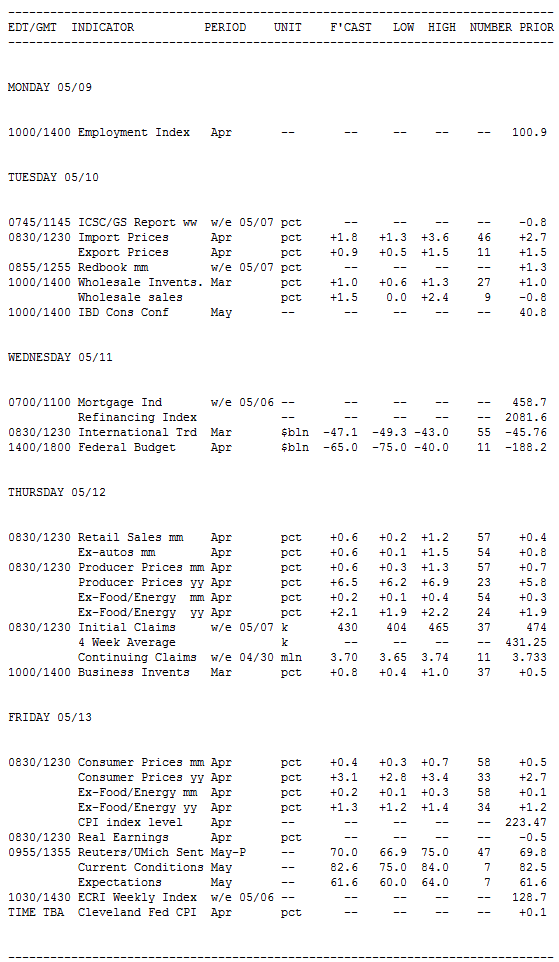

Key events this week include retail sales, $72 billion in Treasury coupon auctions, two inflation reports, and the first look at May consumer sentiment. Economists at Citigroup believe the run-up in fuel prices will dominate each of those reports, but say "the recent collapse in crude oil prices will dramatically alter interpretations of the results."

Key Events This Week:

Monday:

No economic data.

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

Tuesday:

10:00 - The Wholesale Trade report

is anticipated to post continued growth in March. In February,

inventories jumped 1% on a monthly basis and were up 12.7% from the

prior year. Consensus forecasts weren't available for this report, but

in its Q1 GDP report, the BEA assumed a growth rate of 0.9% in March.

"Wholesale

inventories have increased since the start of 2010 and we expect them

to follow their current positive trend," said economists at BBVA,

predicting a monthly pickup of 1.1%.

Economists at Nomura Global

Economics added: "Wholesalers' inventories likely increased at a solid

pace in March, led by stock building as well as higher gasoline prices.

10:00 - Tim Geithner, Treasury Secretary, holds a press conference following US-China Strategic and Economic Dialogue in Washington.

12:45 - Jeffrey Lacker, Richmond Fed President. speaks on the economic outlook in Virginia.

Treasury Auctions:

11:30 - 4-Week Bills

1:00 - 3-Year Notes

It's Class A MBS roll day! Fannie Mae and Freddie Mac 30-year coupons move to June delivery as the monthly settlement process begins for May trades.

Wednesday:

8:30 - Rising petroleum prices are expected to widen the monthly Trade Deficit in

March. Economists look for a $47.7 billion trade gap, up from $45.8

billion a month before. Both imports and exports are anticipated to pick

up, but the pace of imports should rise faster due to oil costs. The

expected widening follows a 1.7% narrowing in February.

"Petroleum

imports probably increased sharply on both higher price and increased

volume," said analysts at Citigroup. "Given the further price rise in

April, we expect that this is not the last big increase in the oil

bill."

Economists at IHS Global Insight said trade "was close to

neutral for growth in the first quarter," but they see exports carrying a

little more momentum in the second quarter, while import growth slows.

2:00 - The gap in April's Budget Statement from

the Treasury is anticipated to be roughly one-third of the previous

month, but April is usually a time of surplus so it's not much to get

excited about. Economists look for a $65 billion deficit, with estimates

ranging from $16 to $75 billion. That looks relatively good next to

March's $188 billion gap, or April 2010's $82.7 billion deficit. But in

the first six months this fiscal year, the deficit already adds to

$829.4 billion - about 15% worse than last year.

"A strong

increase in April tax receipts likely improved the budget balance," said

economists at Nomura Global Economics. "We expect the budget deficit to

be $42.0 billion in April, compared with a deficit of $82.7 billion for

April of last year."

12:00 - Narayana Kocherlakota, Minneapolis Fed President, speaks on contingent planning for monetary policy in New York.

12:20 -Dennis Lockhart, Atlanta Fed President, speaks on the economic outlook in Atlanta.

1:00 - Sandra Pianalto, Cleveland Fed President, speaks on the economic outlook and monetary policy in Cincinnati.

Treasury Auctions:

1:00 - 10-Year Notes

Thursday:

8:30

- Headline inflation is expected to remain worrisome due to soaring

energy prices but core costs should be contained in the Producer Price Index. April's

report is expected to produce a 0.6% headline climb in the month,

following a 0.7% advance in March and a 1.6% gain in February. Nine

consecutive advances have brought the annual rate to 5.8% (as gas prices

have jumped nearly one-third).

The more closely-watched core

index - which strips out volatile energy and food prices - is expected

to inch forward just 0.2% in April, following a more-than-forecast 0.3%

uptick. Core prices are currently up 1.9% for the year - the fastest

pace since August 2009.

"Producer prices probably jumped again in

April, on sharply higher energy prices, especially gasoline," said

economists at Citigroup, who noted that gas prices surged 25% in the

past two months but that rise has been muted by seasonal adjustments.

"Rising seasonal factors have held the two-month increase in gasoline

prices to just 11%. Seasonal adjustment will dampen May gasoline prices

as well. Those factors, combined with the sudden drop in oil prices this

week, could produce a sharp turn in PPI next month."

Energy costs make up one-fifth of the headline index, according to economists at Janney Montgomery Scott.

8:30 - Retail Sales have

posted average monthly gains of 0.8% in the last three quarters, so the

Street's +0.6% forecast for April is a bit below trend even if it's

higher than March's 0.4% gain. Some of the gain also reflects high gas

prices, so gains may not be widespread. But economists are impressed

with how the consumer has held up despite rising energy costs.

Analysts

at Citigroup, for instance, note that motor vehicle sales were roughly

unchanged and large retail chains reported healthy gains.

"The

extra household income from an improving labor market and the temporary

payroll tax cut has been helping consumers cope with higher gasoline and

food prices," said economists at IHS Global Insight, who note that in

April there was a strong increase in private payrolls and an uptick in

average hourly earnings.

8:30 - Economists at Deutsche Bank said the weekly Initial Jobless Claims report

would be "the most important labor market indicator between now and the

next employment report." The reasoning is simple: the nonfarm payrolls

survey suggested 268k private jobs were created last month - the

strongest month since February 2006. But reaction to the report was

appropriately mixed, as unemployment rose to 9% and the previous day's

jobless claims report jumped 43k to 474k, its highest weekly reading

since August.

Economists believe the first week of May could provide

some much-needed correction. The last report also suggested temporary

distortions that could have driven the claims figure higher. Still, the

median forecast of 430k is far from inspiring; nor is the range of

forecasts: from 415k to 465k.

"We expect that the surge in New York

and Oregon filings, which added nearly 28,000 to unadjusted claims in

the previous week, will reverse," said economists at Citibank, who

anticipate a weekly decline of 60k. "However, shutdowns among certain

auto manufactures may place some upward pressure on the figure. We also

note that storm- related filings may be more apparent during the

reference period, introducing the risk that claims could exceed our

estimate."

8:30 - Charles Plosser, Philadelphia Fed President, speaks on the economic outlook in Florida.

10:00 - Few comments were available for March's Business Inventories.

The consensus expects a 0.8% increase following a 0.5% uptick a month

before, but economists said little beyond that inventories would post

increases in line with previous reports.

"The March business

inventory report will reveal how much retailers added to stocks in

March," said analysts at Nomura. "If the pace of stockpiling topped the

BEA's assumptions (+0.6% for March), the report would add a few tenths

to our Q1 GDP tracking estimate."

Treasury Auctions:

1:00 - 30-Year Bonds

Friday:

8:30 - The Consumer Price Index should

report similar trends to the Producer Price Index, but more people

watch this one because it reflects how rising costs are being passed

onto the average spender. Total inflation is set to jump 0.4% in April

following a 0.5% uptick in March, but if energy and food costs are

stripped out than the gain should be a less-than-alarming 0.1%,

economists predict. Even if the monthly headline figure comes in higher

than expected, the market will likely be comforted by last week's

collapse in energy costs.

"On the core side, we continue to see

very low risk of passthrough, particularly now that energy prices have

rapidly reversed course," said economists at Janney Capital Markets.

"Shelter costs remain the biggest single anchor to the CPI, comprising

nearly a third of the total index, and with home prices still on an

evident down trend and rental vacancies elevated in many markets, we see

limited risk of reversal. For the intermediate term, the normalization

of consumer demand in a post-recessionary environment should allow

inflation rates to stabilize in the 1.5% - 2.0% range, even accounting

for $100 oil."

9:55 - A strong payrolls report and the death of

Osama bin Laden aren't enough to change the spirits of the American

consumer, economists say. The U of Michigan Consumer Sentiment report is expected to move forth just 0.2 points to 70 in May, as climbing fuel prices continue to hurt discretionary spending.

"If

the recent large decline in crude oil prices persists, it should remove

a major roadblock to consumer confidence in the months ahead," said

economists at Citigroup.

"Recent news has been a mixed bag,"

added analysts at IHS Global Insight. "April's payrolls and average

hourly earnings improved, but there was an uptick in the unemployment

rate to 9.0%. The first week in May was eventful with a volatile stock

market and falling world oil prices on the economic front, and the

killing of Osama Bin Laden. Stock market volatility is not a good thing

for consumer mood and household net worth - especially with falling real

estate prices. However, falling world oil prices can have a positive

impact on consumer sentiment as long as it translates into cheaper

prices at the pump."