Both benchmark rates and production MBS coupon prices have bounced around a large yet well-defined range so far in 2011. There have been moments when it seemed like rates were doomed to breakout in the wrong direction, there have been times when it felt like a sustained rally was in the works.

At one end of the spectrum we find the potential for snowball buying as a flattening yield curve forces real money investors to add longer dated debt to better match asset cash flows vs. liability cash flows. At the other end of the extreme lies a legit threat of snowball selling, which leads to a rapid spike in rates as real money investors dump longer duration debt and move "up in coupon". (WHAT IS DURATION? WHAT IS EXTENSION RISK?).

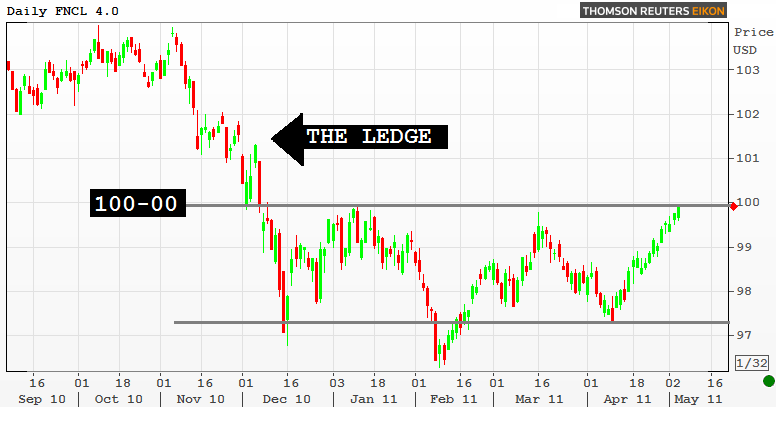

Right now we find ourselves at the aggressive side of the 2011 range, at the base of a steep a ledge.... teetering on a potential shift lower in production MBS coupons. One that would allow originators to hedge their pipelines with 4.0 coupons and break the loan pricing barrier at 4.875%.

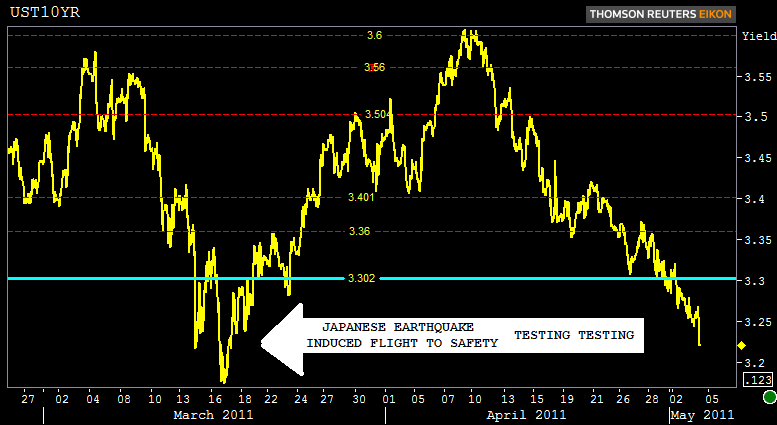

The benchmark 10yr note is testing the yield lows of the year which were hit in the aftermath of the Japanese earthquake induced flight to safety. Breaking these loans and confirming the breakout with snowballish volume is the next phase in the process.

The FNCL 4.5 is revisiting the 103 handle for the first time since December...when snowball selling (duration shedding) last pushed loan pricing off a ledge. Additional gains in this coupon do nothing but add rebate to already juicy 4.875% quotes.

The FNCL 4.0 coupon is being pulled higher by the forces of "parnertia" (convexity buying). A sustained move into premo territory (over par) would give lenders a chance to set hedges using the 4.0 coupon aka lead to a shift lower in production coupons and break the C30 barrier at 4.875%. 4.0s trading at par is a sign that a shift is already in the works. We still gotta climb that ledge though...treading water over 100-00 is a good start.

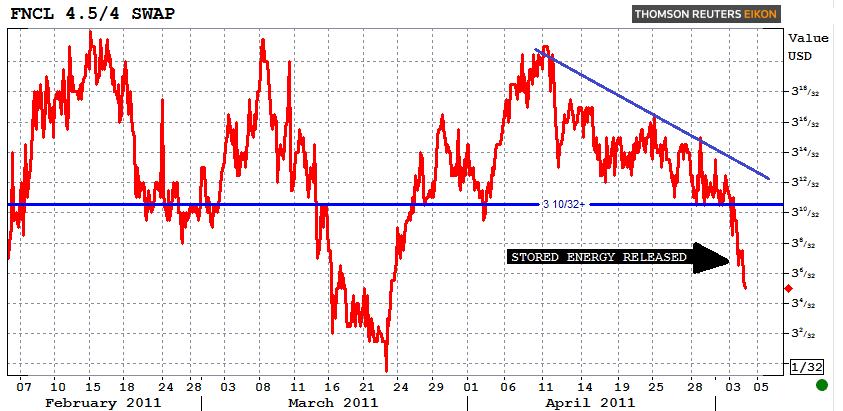

Besides looking at MBS coupon prices outright we can also peer into the potential for a shift "down in coupon" by pacing intercoupon swaps. The price spread between FNCL 4.5s and FNCL 4.0s has narrowed to 3.125 (3-04) after consolidating (storing energy) around 3-10 resistance for almost all of April. Stack compression (bull flattening MBS curve) is another sign of the coupon shift already being in progress.

Plain and Simple: Breaking out of the 1st quarter range would not only imply a shift in economic outlooks and technical trading tactics ...but a shift in duration bias...a shift in the MBS production coupon...a shift in hedge ratios. This requires a great deal of commitment from the bond market. It requires portfolio rearranging. It requires rebooted hedging strategies. It requires position squaring and an accumulation of longer dated debt. We've been here a few times already this year, the prospects for one last run lower in rates is back on the table, but remain defensive. We're seeing the preliminary signs of this process already being in progress...but no sustained commitment as been confirmed. Remember this guidance, it has been a consistent inclusion in our commentary this year.

"Lenders have moved the Best Execution 30-year fixed note rate as low as they possibly can without drastically altering their pipeline hedging strategies. This is a factor of what production mortgage-backed security coupon is most liquid in the secondary mortgage market. On conventional loans, the 4.50 percent MBS coupon is the hedging vehicle of choice for lock desks. Home loans with note rates between 4.875 and 5.25% are generally used to fill 4.50 percent MBS coupon trades. Until MBS investors demonstrate sustainable demand for 4.00 percent 30-year fixed MBS coupons, lenders will not find it economically efficient to quote 4.75 percent note rates without expensive permanent buydown costs. From that perspective, if you are floating a conventional home loan interest rate, you should not be expecting further improvements to your actual rate in the short term. If the bond market recovery rally continues, closing costs will improve, but on the whole, it will take a sustained move higher in 4.00 percent MBS coupon prices for Best Execution to dip below 4.875 percent."