The April Employment Situation Report will be released tomorrow morning. In advance of this high-profile economic event, a wind of fundamental change appears to have swept through financial markets.

Bonds have rocked the rally cap in 14 of the last 14 trading sessions and now sit at their best levels since early December. This rates rally played out even as equities continued to trend higher in the process, until recently that is. Yields eventually fell far enough that on Wednesday we alerted you that a shift in production MBS coupons was potentially in progress. As a result, it was shared with consumers that "we may be witnessing the early stages of a significant shift lower in home loan borrowing costs".

The broader economic recovery is clearly under an increased amount of scrutiny as Main Street seems much more sensitive to even the "transitory" impact of a spike in energy and food costs. Illustrating that sentiment today was a sharp decline in commodity prices. The NYMEX light crude oil contract plummeted $10 (9.27%) to $99.10, moving below $100 for the first time since mid-March.

Although our "big picture" perspective is one that favors a continued move higher in "rate sheet influential" MBS prices (repeating 2010's history), we must share the other side of the story....

Short covering has played a pivotal role in the recent rates rally. "Short covering" is when a bearish trader closes a position that was opened with the intention of capitalizing on lower prices/higher yields. The term "short" describes the trader's directional bias. "Covering" simply means closing the position. The resulting effect of short covering is a contraction in "open interest", which represents the number of open contracts in the marketplace. If a trader has set a short position and prices continue to rise, then their position is considered to be under water or "in the red". Leaving a short position open as rates continue to rally can be dangerous because the position gets more expensive with every uptick in price. So it should make sense that as rates have continued to rally this week it has forced more short covering which has led to snowballing in the bond market. Forced short covering is a sign of investors waving the white flag on their bearish positions but it doesn't mean there is more rally to come. This behavior is encouraging, especially when done so in mass, but it must be intensified by real money investors (as opposed to fast$) who need to move their funds "down in coupon". It must also be backed by a CONFIRMATION of weaker economic fundamentals and shorter hedge ratios....

We'll have the opportunity to see just how receptive the bond market is to a sustained shift "down in coupon" when the Employment Situation Report is released tomorrow. If the market is resistant to confirming the recent rates rally, we could be witnessing a big ole "buy the rumor, sell the news" rally right now. From that perspective, until a breakout is confirmed we will remain defensive of gains.

Here is a sneak peek of the monthly jobs report from Reuters....

PREVIEW- High gasoline prices seen slowing US April hiring

WHAT: U.S. employment report for April

WHEN: Friday, May 6, at 8:30 a.m. EDT (1230 GMT)

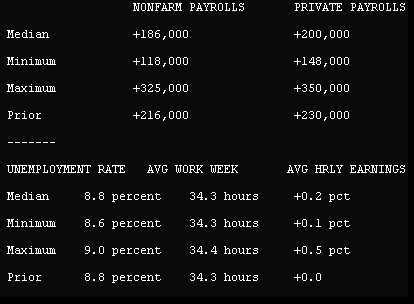

REUTERS FORECASTS:

FACTORS TO WATCH:

U.S. payroll growth likely eased in April as employers responded to rising gasoline prices by scaling back on hiring.

Slower economic growth in the first quarter will also be felt in April's employment report, expected to show employers added 186,000 jobs after expanding payrolls by 216,000 in March -- which was the most in 10 months. Still, payrolls will have grown for seven straight months.

High energy costs held back the economy to an annual growth rate of 1.8 percent, braking sharply from a 3.1 percent clip in the fourth quarter. The price of gasoline for all grades rose 6.6 percent or 24 cents per gallon in April from March.

The anticipated slowdown in job creation was telegraphed by rises in applications for state unemployment benefits, as well as the four-week average of claims.The rise in claims between the March and April survey period was a combination of technical factors and supply-chain disruptions related to the devastating earthquake and tsunami in Japan. Though some auto makers briefly closed plants and reduced hours because of part shortages, they would not necessarily have laid off workers. The Institute for Supply Management survey showed a dip in the employment gauge.

The moderation in employment is expected to be temporary, with energy prices seen leveling off in the summer. Economists expect the economy to regain speed in the second quarter, with the labor market taking up some of the burden for growth.

Although there were five weeks between the March and April survey period, rather than the normal four weeks, that should not have an impact on the payrolls figure as the Bureau for Labor Statistics' seasonal adjustment factor should take this into account.

The unemployment rate is seen steady at a two-year low of 8.8 percent in April, but could rise as those workers who have dropped out of the labor force return. The jobless rate has declined a full percentage point since November, the largest four-month decline since February 1984.

The private sector will likely account for all of the jobs created in April, with employers expected to have hired 200,000 new workers -- building on March's 230,000 gain. Though private payrolls have grown for 13 straight months, they are still roughly 7 million below their pre-recession levels.

The economy has recovered only a fraction of the more than 8 million jobs lost in the 2007-2009 recession. Job growth of between 250,000 and 300,000 a month is needed to have a sizable impact on the pool of 13.5 million jobless Americans.

The unemployment rate is being closely watched by the Federal Reserve, which last month signaled it was in no hurry to start withdrawing the massive stimulus it has lent the economy, The U.S. central bank lowered its projection for unemployment for this year and 2012.

Government employment is expected to have shrunk for a sixth straight month in April.

Employment gains last month were most likely in the private services sector, which accounts for more than 80 percent of U.S. economic activity. Goods-producing industries payrolls likely slowed again in April, with construction employment probably declining and manufacturing hiring moderating somewhat.

The employment report is also expected to show the average work week unchanged at 34.3 hours for a third straight month and no sign of wage inflation, with average hourly earnings rising 0.2 percent after being flat in March. (Polling by Bangalore unit; Reporting by Lucia Mutikani; Editing by James Dalgleish)

---------------------------------

Plain and Simple: Rates are at a tipping point ahead of the Employment Situation Report tomorrow. The recent rates rally is on the line as short covering has led bonds into overbought territory and fast$ traders are looking for any excuse to book a profit before next week's Treasury debt issuance. The positive progress we've enjoyed since early April is only the beginning of what might evolve into a sustained rally in the bond market. Nothing has been confirmed. Preliminary signs are encouraging, but could very well be another "false start".

READ MORE: MBS Ledge: Shift in Production Coupon Potentially in Progress