The bond market must've had too many marshmallow peeps yesterday cause trading flows are comatose in the "rate sheet influential" portion of the yield curve.

With Germany, France, Australia, the UK, Hong Kong and several other markets all closed today and the high-risk FOMC event ahead, this isn't surprising as market participants have moved into "wait and see" mode before the Fed Statement on Wednesday afternoon. Check out what we wrote last week regarding position squaring ahead of the FOMC meeting.

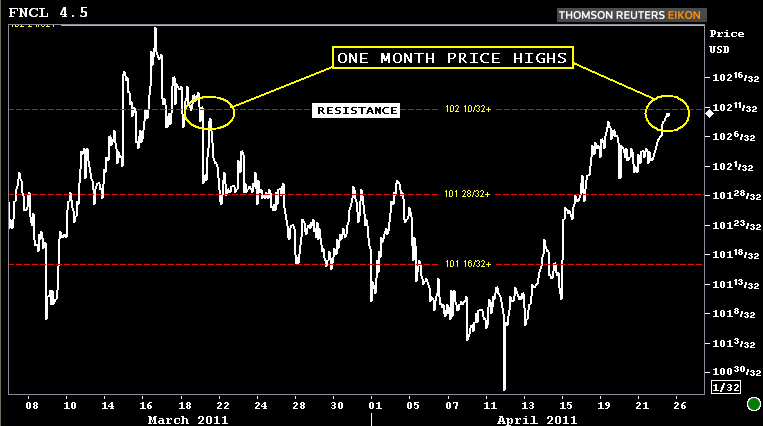

Nonetheless, amidst a backdrop of limited pipeline hedging, thin liquidity, and declining implied volatility, "rate sheet influential" MBS indications have drifted up to their highest levels of the day....and month! Current Coupon MBS are outperforming benchmarks as well. On the spot I've got the CC marked 3.3bps lower at 4.107%. 73.7bps/10yr TSY vs. +74.5bps on Thursday afternoon. +67.9bps/10yr IRS after going out +68.7bps on Thursday. So higher and tighter we go! The FNCL 4.5/4 swap is pretty much UNCH at 3-14. WHY ARE CC MBS OUTPERFORMING?

The FNCL 4.5 is +8/32 at 102-10. This is a key resistance level aka it will be tough to break!

C30 loan pricing is 7.8bps better on average vs. rebate on Thursday afternoon. With production MBS coupon prices now +8/32 (4ticks above morning indications), reprices for the better are possible. Lenders will likely be hesitant to recall and reprice for the better though. Liquidity is lacking in the TBA MBS market. Hedging a pipeline won't be easy because of that...plus we're only 0.125 better in price.