The week is ahead is relatively slim on macroeconomic data. The highlights may be the several speeches from Federal Reserve officials, including Ben Bernanke on Wednesday. Three Treasury auctions will test the bond market's appetite for bargain buying following a recent jump in benchmark yields. Also on the radar of rate watchers is an announcement from the Obama Administration that will hope will provide directional guidance on the future of the GSEs.

Treasury will sell a total of $72 billion in coupon and bond debt this week. This will raise $50.2 billion in new cash and refund $21.8 billion in maturing securities. In their borrowing statement the TBAC said they expect Treasury to hit the debt ceiling between April 5th and May 31. Treasury does expect coupon auction sizes to be stable in the coming months and any budget shortfalls will be made up by larger bill auctions (less than 1-year maturity also known as discount or zero coupon bonds.)

The Obama Administration is expected to release some sort of announcement on the future of housing finance this week. MND expects the Administration to present a few potential pathways towards reform, but no concrete guidance. The Adminstration has communcated a clear intention to lessen the mortgage market's reliance on government backed financing. To accomplish that goal the Administration will encourage private investors to re-liquidate the non-agency secondary market. This is another step in the right direction but by no means the end of what will be a long drawn out process Reforming the housing finance mechanism will take much time and even more debate. Getting it right the first time is of the utmost importance.

“Stocks are expected to keep rising next week as strong earnings push the S&P 500 past key resistance levels, despite an increase in oil prices, civil unrest in the Middle East and internal overbought signals,” Analysts at Thomson Reuters predicted.

After the 7-week trading range finally broke down late last week, MND analysts now expect the benchmark 10 year Treasury note to move at least up to 3.70% before a recovery rally is considered by bond traders. This implies mortgage rates will move higher in the day's ahead. READ MORE

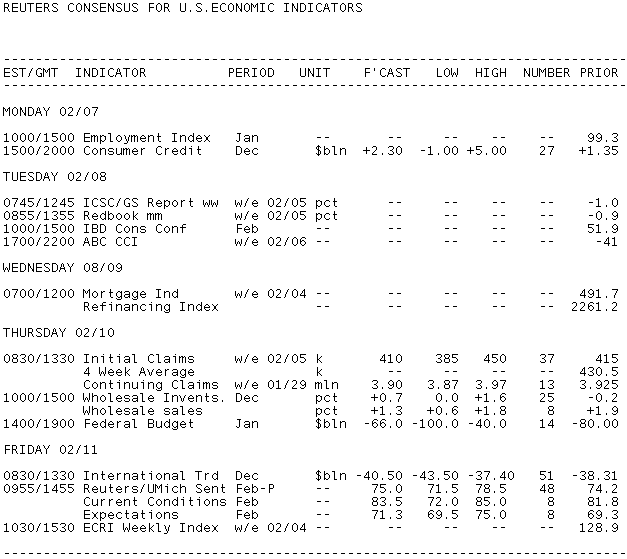

Key Events This Week

Monday:

10:15 ― The Federal Reserve will purchase an estimated $7-9 billion in Treasury coupons maturing between 2/15/2018 and 11/15/2020

11:30 ― President Obama delivers a speech to the US Chamber of Commerce.

“The business community that felt burned during Obama's first two years in office is now divided over several policy and personnel changes, from tax cuts and a major trade agreement to the appointments of business leaders to key posts,” said reporters at USA Today. “Big business is warming to the president; small business, not so much.”

3:00 ― Consumer Credit is anticipated to expand by $2 billion in December, following a $1.4 billion expansion in November and marking the third straight month of growth. Don’t be fooled by the headline though; the deleveraging process continues.

Revolving debt ― which includes credit cards ― has fallen for the past 27 months, including a 6.3% annual fall in the November report. Non-revolving or installment credit ― which includes student and auto loans ― accounted for the recent increase, and that was mostly due to federal government lending.

Economists at Nomura point out expansions of consumer credit in October and November were the first back-to-back gains since July 2008.

“However, the advance was likely related to regulatory changes in federal student loans,” they noted. “Stripping out loans provided by the Federal government, consumer credit outstanding has been declining since August 2008. This is especially true in the case of demand for credit cards, the component which is closely-related with consumption activity.”

Tuesday:

8:45 ― Jeffrey Lacker, president of the Richmond Fed, speaks on the economic outlook at the University of Delaware in Newark.

10:15 ― The Federal Reserve will purchase an estimated $1.5 billion in Treasury coupons maturing between 8/15/2028 and 11/15/2040

12:30 ― Dennis Lockhart, president of the Atlanta Fed, speaks to the Calhoun Chamber of Commerce in Anniston, Alabama.

1:00 ― Treasury auctions $32 billion 3-year notes

1:30 ― Richard Fisher, president of the Dallas Fed, speaks on the economy to the Stemmons Corridor Business Association in Dallas.

ALERT: Tuesday is Class A Notification Day in the TBA MBS Market

Wednesday:

7:00 ― MBA Mortgage Applications jumped 11.3% last week, reversing a 13% decline the week before. The weekly measure is often too volatile to be meaningful, but the annual changes show the trends are decidedly weak: the purchase index was 21.4% lower than the same period one year ago.

10:15 ― The Federal Reserve will purchase an estimated $6-8 billion in Treasury coupons maturing between 2/15/2015 and 7/31/2016

1:00 ― Treasury auctions $24 billion 10-year notes

6:45pm ― Ben Bernanke, chairman of the Federal Reserve, testifies for the first time in front of the Republican-led House Budget Committee.

Economists at IHS Global Insight said the chances of hearing fresh insight from Bernanke are slim, even if Republicans press the chairman on Fed policy.

“The House Committee may well attempt to prod the Chairman in terms of options on dealing with the budget deficit and federal debt situation, but Bernanke has skillfully skated around this topic in the past,” they said. “So it is not clear at this point what the purpose of the out-of-cycle testimony will be, other than a ‘get to know you better’ with the new Republican Budget committee leadership.”

6:45pm ― Dennis Lockhart, president of the Atlanta Fed, speaks to the CFA Society in Atlanta.

Thursday:

8:30 ― Initial Jobless Claims for the week ending Feb 5 are anticipated to fall 3k to 412k, a figure well-below the four-week average of 436k. Claims have been volatile lately due to snowstorms ― ranging from 391k in late December to 457k in mid-January ―

and this report should be no exception.

“We see the four-week moving average, currently about 430k, as indicative of healthy employment growth continuing in 2011,” said economists at Nomura.

10:00 ― Wholesale Inventories are expected to rebound by 0.7% in December following a 0.2% cutback one month before. The growth is part is part of a broader trend of re-building inventories, as businesses are expecting the economic recovery to take firmer shape in 2011.

However, economists at Nomura point out that changes in private inventories were “an enormous drag on real GDP growth in Q4, subtracting 3.7 percentage points. They said a 0.5% increase would be consistent with the GDP report from a few weeks ago, and that any number below that figure would suggest downward revisions to Q4 growth.

12:40 ― Dennis Lockhart, president of the Atlanta Fed, participates in a panel discussion on public debt management and fiscal policy to the U.S.-Swiss Dialogue in Atlanta.

1:00 ― Treasury auctions $16 billion 30-year bond

2:00 ― The Treasury Budget for the first month of 2011 is expected to show a deficit of $60 billion. That may not sound too bad compared with the $80 billion deficit a month before, but January is typically a surplus month. Bloomberg notes the average surplus for the month has been $21.3 billion for the past decade. Last year, however, it was a $42.6 billion deficit. One reason the deficit is expected to grow: the payroll tax cut.

2:00 ― The Federal Reserve releases an updated approximate purchase amount and tentative outright QEII Treasury operation schedule. At that time, the Desk will also publish information on prices paid for securities included in the operations listed above.

Friday:

8:30 ― The monthly gap in December’s Trade Balance report is anticipated to grow to $40.5 billion, from $38.3 billion a month before. The November report narrowed thanks to a 0.8% gain in exports (including a 1.2% increase in nominal goods exports), while imports rose just 0.6% (mainly a result of energy needs; imports excluding petroleum actually fell 0.1%). But imports are anticipated to outpace exports in December as demand for petroleum speeds up after two weak months.

“Even with the wider deficit in December, trade will remain a strong boost to GDP growth in the fourth quarter of 2010, with imports falling across the board and exports showing strong momentum,” said economists at IHS Global Insight.

9:55 ― Consumer Sentiment could be on the upswing this month as the stock market continues to improve and the unemployment rate falls. The benchmark S&P 500 improved 2.26% in January, while the unemployment rate ― viewed with skepticism by many ― has fallen to 9% from 9.8% in the past two months. Also, the mid-January report showed the expectations component inch forward to 68.2, the highest level since June.

“The current and expectations indices are both expected to increase, with the current situation index increasing faster,” said economists at IHS Global Insight. “The Dow Jones Industrial Average has moved through the 12,000 mark, boosting consumer sentiment despite a poor housing market, uncertainty in the Middle East, inclement weather, and high fuel and food prices. We expect the consumer sentiment and spending momentum that built up in the last two quarters of 2010 to spill over into 2011.”

Economists at BBVA also look for an increase, but say modest improvements won’t be enough to change their assessments of private consumer spending.

“Consumers’ confidence has remained virtually flat since mid-2009, reflecting a sort of wait-and-see attitude towards spending,” they wrote. “Indeed, even though private spending has recently gained momentum, consumers are still affected by lack of credit, deleveraging and uncertainty in the labor market.”