Short and sweet Friday posts are my favorite. I bet they're your favorite too....

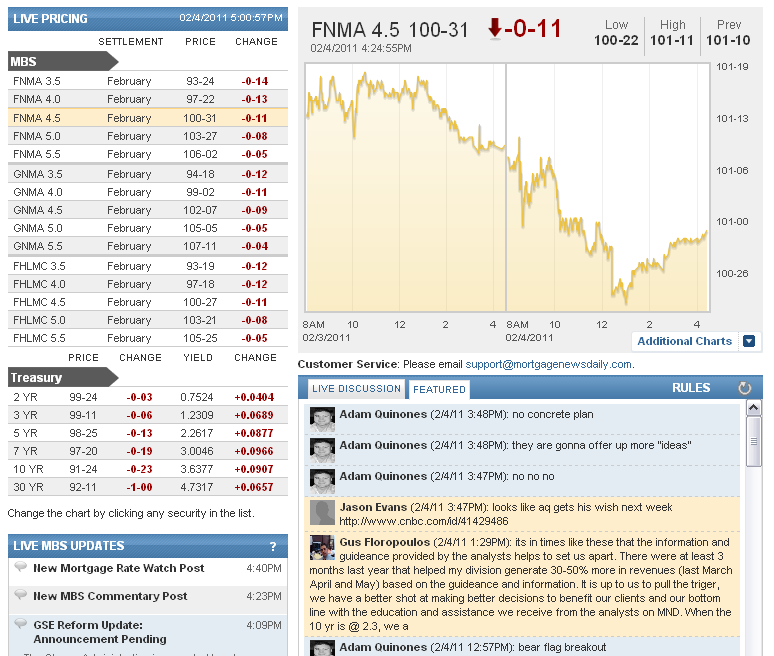

After 7-weeks of consolidation, stored energy was finally released in the bond market today. The range has officially been broken. Ya!!!. I was suffering greatly from range exhaustion. This is much needed relief. I apologize for the celebration. This range break was far from originator friendly. The production MBS coupon has shifted from 4.50 to 5.00 MBS. 4.50 trades still need to be filled so you'll see 5.00% and 4.875% on C30 rate sheets, but all new production is destined for a 5.00 bucket, especially if prices fall further from here. Thie means, if we worsen from current levels, 5.375% could darn well become your new best execution 30 year fixed mortgage rate. You should dust of THIS POST on extension risk for a better explanation of why rates rise faster then they fall.

Below is our long-term 10yr TSY note chart with technical studies. The teal triangle you see is the BEAR FLAG pattern we've talked about so many times over the past month. THIS POST explains the bear flag pattern and what it meant for mortgage rates. I think you know what it meant though. BAD THINGS. Also on this chart you should notice a white circle at the intersection of two dotted gray lines at 3.70%. This is where our long and short term fibonacci retracements run into each other. This is our next target in 10 year notes.

The release of stored energy in benchmark Treasuries was not friendly toward loan pricing. MG discussed the ramifications on rate sheets on the consumer blog channel. I urge you to read it HERE.

As far as the particulars go, production MBS prices fell far enough today to force lock desks into splitting up there pipeline hedging strategies between 4.50 and 5.00 coupons. They'll have to trim margins to offer 4.875% and have it make sense to borrowers though. The secondary market current coupon rose 10.7bps to 4.329%, at least in my model. Yield spreads were tighter then they were wider and then tighter again. Bargain buyers reportedly showed interest at the price lows. This is a good sign as more MBS selling would be a catalyst for broader liquidation in the bond market (shift in duration bias).

With $72 billion in Treasury auctions scheduled for Tuesday, Wednesday, and Thursday....we'd anticipate at least one test of 3.70% before a potential turn around is considered. It is imperative that 10s do turn around before too long though. If they trade much higher and the curve continues to steepen from already record wides, we're sure to see snowballing selling and the potential for a run back to 4.00%. Newly set short positions will need to be covered first. Then real money will need to add momentum with bargain buying. This is all pie in the sky for now though. We're targeting a test of 3.70% in 10s. That means we expect this to get worse before it gets better. We sure do hope we're wrong about that though...because the bond market is teetering on a major shift in duration bias.

HERE is a recap of the headache provided by the Employment Situation Report. Check out the comments in the dashboard discussion above...I provided an update on GSE Reform. HERE is the micropost I wrote on it.

We lost a family dog this week. A much loved family dog. It sucked. Alot. Say a prayer for Lacie please. She will be grealty missed.

I want the yellow team to win the Super Bowl. More importantly I want the Caps to beat the Pens on Sunday.