I told MG last night that this market doesn't have much of a pulse at the moment, but that we would find out today just how numb traders are after we sort through a deluge of data this morning.

ROUND 1 PART 1: RETAIL SALES

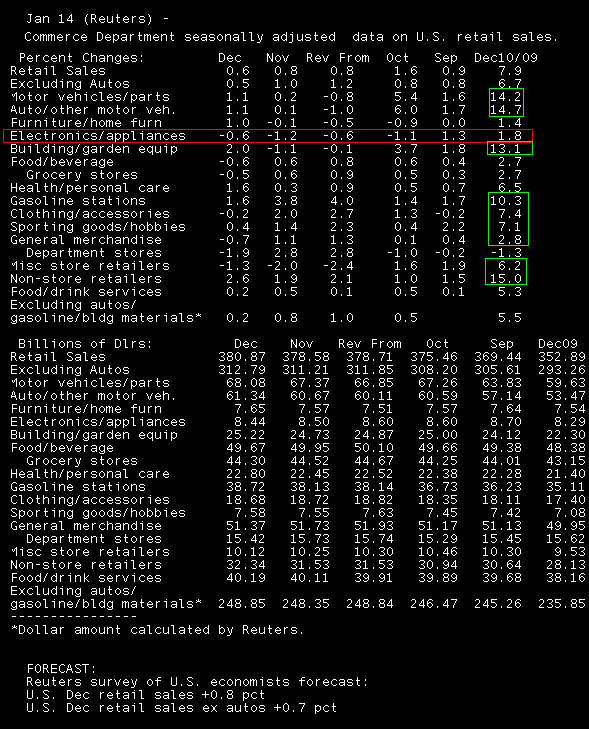

ADVANCE MONTHLY SALES FOR RETAIL AND FOOD SERVICES DECEMBER 2010: The U.S. Census Bureau announced today that advance estimates of U.S. retail and food services sales for December, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $380.9 billion, an increase of 0.6 percent (±0.5%) from the previous month, and 7.9 percent (±0.7%) above December 2009.

Reuters Quick Recap...

RTRS-US DEC RETAIL SALES +0.6 PCT (CONSENSUS +0.8 PCT) VS NOV +0.8 PCT (PREV +0.8 PCT)

RTRS-US DEC RETAIL SALES EX-AUTOS +0.5 PCT (CONS +0.7 PCT) VS NOV +1.0 PCT (PREV +1.2 PCT)

RTRS-US DEC RETAIL SALES EX-GASOLINE +0.5 PCT VS NOV +0.5 PCT

RTRS-US DEC RETAIL SALES EX-AUTOS/GAS/BUILDING MATERIALS +0.2 PCT VS NOV +0.8 PCT

RTRS-US DEC GASOLINE SALES +1.6 PCT VS NOV +3.8 PCT

RTRS-US DEC CARS/PARTS SALES +1.1 PCT VS NOV +0.2 PCT

RTRS-US RETAIL SALES +6.6 PCT IN 2010 VS. -6.5 PCT IN 2009

08:30 14Jan11 RTRS-TABLE-U.S. Dec retail sales rise 0.6 pct

A few observations...

Note the year over year changes. This is the metric that really fuels the bullish fire on Wall Street. A 14% uptick in auto sales, +13% YoY in building equipment, +7.4% in clothing sales, +10% in gasoline receipts, +7.1% in sporting goods, +15% in "non-store retailers". When viewing the data on a shorter timeline, the advance month over month changes failed to match estimates. And when you strip out auto purchases, gas, and building materials, retail sales were up by a meager +0.2% vs. +0.8% in November.

I know I'm taking the pessimistic point of view here, but it's not a factor of our bias toward interest rates, it's a factor of us needing to call attention to overly optimistic attitudes. We're dealing with a long slow, choppy, segmented recovery here people. Upgrading GDP growth from 3.0% to 3.5% just isn't gonna cut it when it comes to putting people back in their jobs (many of which are lost forever).

BTW NON STORE RETAILERS = ONLINE SHOPPING (Here is the NAICS description). Firms don't have to hire as many temporary workers when they are selling more inventory over the web.

ROUND 1 PART 2: Consumer Level Inflation

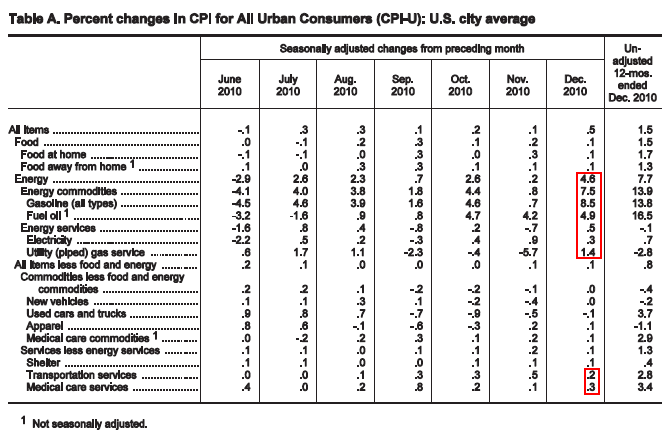

CONSUMER PRICE INDEX – DECEMBER 2010: The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.5 percent in December on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 1.5 percent before seasonal adjustment.

The energy index increased in December. The gasoline index rose sharply and accounted for about 80 percent of the all items seasonally adjusted increase. The household energy index, which declined in November, increased as well. The food index increased slightly in December, with the fruits and vegetables index rising notably.

The index for all items less food and energy also rose in December. An increase in the shelter index accounted for about 60 percent of the rise, and the indexes for airline fares, medical care and apparel rose as well. These increases more than offset declines in the indexes for communication, recreation, and household furnishings and operations.

Reuters Quick Recap...

RTRS-U.S. DEC CPI +0.5 PCT (+0.5047; CONSENSUS +0.4 PCT), EXFOOD/ENERGY +0.1 PCT (+0.0923; CONS +0.1 PCT)

RTRS-U.S. DEC CPI YEAR-OVER-YEAR +1.5 PCT (CONS +1.3 PCT), EXFOOD/ENERGY +0.8 PCT (CONS +0.8 PCT)

RTRS-U.S. DEC UNADJUSTED CPI INDEX 219.179 (CONS 219.022) VS NOV 218.803

RTRS-U.S. DEC CPI ENERGY +4.6 PCT, GASOLINE +8.5 PCT, NEW VEHICLES UNCH

RTRS-U.S. DEC CPI FOOD +0.1 PCT, HOUSING +0.2 PCT, OWNERS' EQUIVALENT RENT OF PRIMARY RESIDENCE +0.1 PCT

RTRS-U.S. DEC CORE CPI SEASONALLY ADJUSTED INDEX 222.187 VS NOV 221.982

RTRS-U.S. DEC REAL EARNINGS ALL PRIVATE WORKERS -0.4 PCT (CONS -0.2 PCT) VS NOV -0.1 PCT (PREV -0.1 PCT)

RTRS-U.S. DEC CPI RISE LARGEST SINCE JUNE 2009 (+0.7 PCT)

RTRS-TABLE-U.S. Dec CPI rose 0.5 pct

HEY CHECK OUT THE COST PUSH INFLATION!!! I'm sure you've noticed rising energy/gasoline prices at home. They are showing up in the data as well. That is sure to sour the mood on Main Street.

Speaking of souring consumer moods...

ROUND 2:CONSUMER SENTIMENT

Reuters Quick Recap...

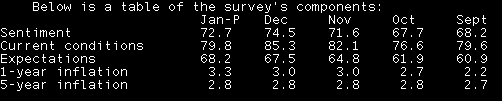

RTRS-THOMSON REUTERS/U. OF MICH US CONSUMER SENTIMENT PRELIMINARY JAN 72.7 (CONSENSUS 75.4) VS FINAL DEC 74.5

RTRS-THOMSON REUTERS/U. OF MICH CURRENT CONDITIONS INDEX PRELIM JAN 79.8 (CONSENSUS 84.6) VS FINAL DEC 85.3

RTRS-THOMSON REUTERS/U. OF MICH CONSUMER EXPECTATIONS INDEX PRELIM JAN 68.2 (CONSENSUS 68.3) VS FINAL DEC 67.5

RTRS-THOMSON REUTERS/U. OF MICH 12-MONTH ECONOMIC OUTLOOK INDEX PRELIMINARY JAN 87 VS FINAL DEC 79

RTRS-THOMSON REUTERS/U. OF MICH 1-YEAR INFLATION OUTLOOK PRELIM JAN 3.3 PCT VS FINAL DEC 3.0 PCT

RTRS-THOMSON REUTERS/U. OF MICH 5-YEAR INFLATION OUTLOOK PRELIM JAN 2.8 PCT VS FINAL DEC 2.8 PCT

RTRS-THOMSON REUTERS/U. OF MICH 12-MONTH ECONOMIC OUTLOOK INDEX HIGHEST SINCE SEPTEMBER 2009

RTRS-THOMSON REUTERS/U. OF MICH 1-YEAR INFLATION OUTLOOK HIGHEST SINCE OCTOBER 2008

RTRS-THOMSON REUTERS/U. OF MICH CURRENT CONDITIONS LOWEST SINCE SEPTEMBER 2010

RTRS-TABLE-Reuters/U Mich Jan. prelim. sentiment index 72.7

Here is the headline from Reuters...

Rising gasoline prices sour U.S. consumer mood: Rising gasoline prices beat down U.S. consumer sentiment in early January, overshadowing an improved job outlook and passage of temporary federal tax breaks, a survey released on Friday showed.

5-year inflation expectations remain well-ground.

ALSO OUT...

Industrial Output moved up 0.8% vs. calls for a read of +0.5%. Reuters cites unusually cold weather as the culprit behind a 4.3% uptick in Utility output.

RTRS-U.S. DEC INDUSTRIAL OUTPUT +0.8 PCT (CONSENSUS +0.5 PCT) VS NOV +0.3 PCT (PREV +0.4 PCT)

RTRS-U.S. DEC CAPACITY USE RATE 76.0 PCT (CONS 75.6 PCT) VS NOV 75.4 PCT (PREV 75.2 PCT)

RTRS-U.S. DEC MANUFACTURING OUTPUT +0.4 PCT VS NOV +0.3 PCT, CAP USE 73.2 PCT VS NOV 72.9 PCT

RTRS-U.S. DEC MINING OUTPUT +0.4 PCT (NOV -0.7 PCT), UTILITIES OUTPUT +4.3 PCT (NOV +1.5 PCT)

RTRS-U.S. DEC INDUSTRIAL OUTPUT EX CARS/PARTS +0.9 VS NOV +0.5 PCT

RTRS-U.S. DEC MOTOR VEHICLE ASSEMBLY RATE FALLS TO 7.41 MLN UNITS/YR FROM NOV 7.53 MLN

RTRS-U.S. Q4 INDUSTRIAL OUTPUT +2.4 PCT (Q3 +6.5 PCT), CAP USE 75.5 PCT (Q3 75.1 PCT)

RTRS-FED SAYS UTILITIES OUTPUT IN DEC BOOSTED BY UNUSUALLY COLD WEATHER; U.S. DEC CAP USE RATE HIGHEST SINCE JULY 2008

(Reuters) - US industrial output rose 0.8 pct in December: U.S. industrial output rose by a stronger-than-expected 0.8 percent in December as unusually cold weather caused utility output to soar, a Federal Reserve report showed on Friday. The increase was the largest since July and was above a median forecast for a 0.5 percent increase in a Reuters poll and followed a downward revision in November's output growth to 0.3 percent from an originally reported 0.4 percent gain. Utility output in December rose 4.3 percent over November, while manufacturing and mining output each rose 0.4 percent.

MARKET REACTION....

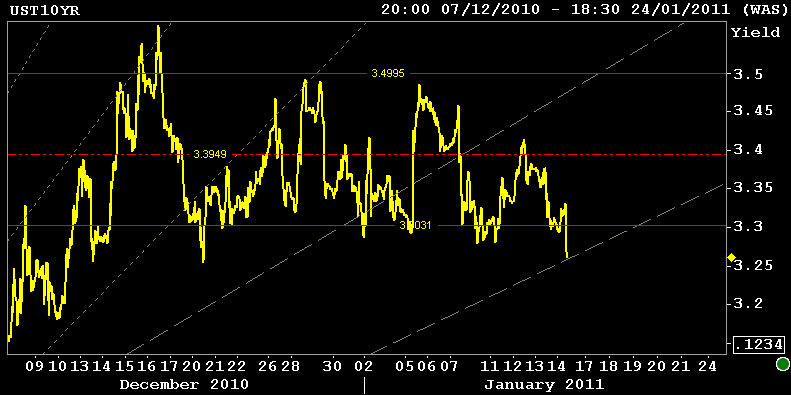

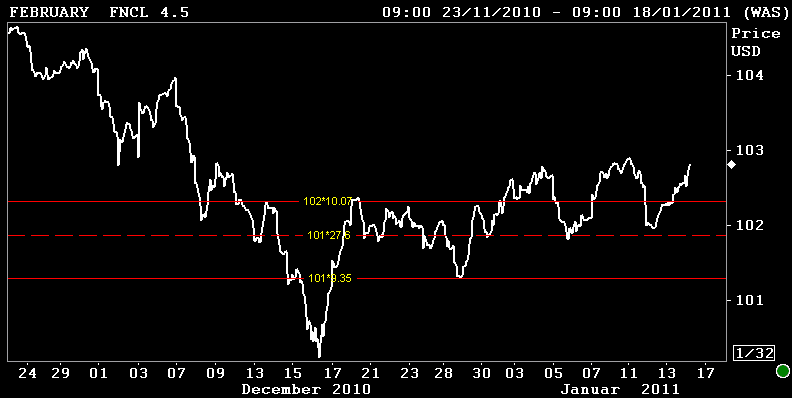

The yield curve is flattening as real$ waves in a few more longs, squeezing out the short base in the process. MBS prices are higher and spreads are tighter into the bull flattener. And loan pricing is the best we've seen since early December.

10s are through a cluster of resistance around 3.28 - 3.30%, currently bid +11/32 at 94-22 yielding 3.261%. Have I mentioned how much I love using fibonacci fans? Check out the touch at my 50% retrace...technically speaking we'd expect to see a little push back at this point aka profit taking. If we break through this level with volume and forced short covering, we will be quite encouraged.

Production MBS coupons are performing well into the rates rally. We're approaching 40 day price highs again. Loan pricing reflects that too...although the buydown is still expensive, C30 4.75% is looking more attractive outright.

I've got the current coupon marked at 3.967%. +69bps/10yTSY. +63bps/10yIRS. +208bps/5yTSY

Rising energy prices certainly played a huge role in all the data we received this morning!

THE AX IM GRINDING: The great margin squeeze of 2011 is coming for both consumers and producers. For consumers, without wage growth (Beige Book just said its MIA), disposable income shrinks as energy and food costs rise. While hopefully just a temporary jump, this will only serve to sour the mood on Main Street. For producers, profit margins are being pressured because they aren't able to pass along higher input prices to consumers who are already cost conscious bargain hunters. That will only delay sustained payrolls growth as firms choose to rely on temporary help services and contracted employees to get them through seasonal spikes in consumer demand.

The bond market has a pulse! We are encouraged by this price action but recognize what's at stake..not just a shift in technical biases...a shift in duration bias that would require a commitment from bond investors. READ MORE ABOUT THE POTENTIAL FOR A SHIFT IN PRODUCTION COUPONS