Treasury just reopened $21 billion 11/15/2020 10 year notes.

The bid to cover ratio, a measure of buyer demand, was 3.30 bids submitted for every 1 accepted by Treasury. This is well above average and the most aggressive bidder behavior (as measured by the BTC) since the April 2010 issue when the BTC printed an astounding 3.72 bids submitted for every 1 accepted.

The high yield was 3.388% which is 1bp below the "When Issued" yield. Another sign that demand was strong...

Indirect bidders took home 53.6% of the competitive bid which is above average but below their 56.6% takedown in the November refunding and the 54.7% award seen at the September auction.

Direct bidders were awarded a below average 7.9% of the issue and only 15.3% of what they bid on.

Dealers added 38.5% of the competitive bid and 19.1% of what they bid on. Both metrics were below average which isn't necessarily a bad thing because indirect bidders more than made up for the difference. (We don't want dealers to be forced to buy because other accounts were unwilling.)

Plain and Simple: Buy side demand was strong even though direct bidder participation was a bit weaker than usual, indirects more than made up for missing demand. Trading desks say overseas buyers were noticeably absent this morning, which we assumed was a factor of Asian investors waiting until the auction to put their money to work. They did just that as illustrated by the indirect bid.

Market Reaction...

After holding below 3.42% support all morning, benchmark 10s rallied through 3.40% and are currently bid -5/32 at 93-29 yielding 3.359%.The 2s/10s curve is 2bps flatter at 275bps wide. 5s are back below 2.00% again. And 10yr swap spreads have firmed slightly from session wides. (NEGATIVE NOTE: 10y TIPS breakevens spiked up to 2.42% at 1pm)

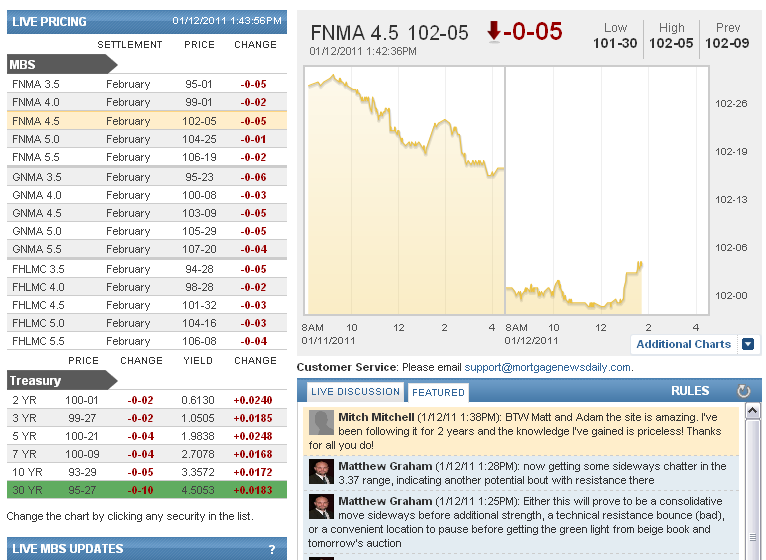

In the TBA MBS market, a bounce in benchmarks has helped lead "rate sheet influential" coupons recover from intraday price lows. The February FNCL 4.5 is currently -4/32 at 102-05. The bid/ask on FNCL 4.5s widened out considerably into the TSY rally though. This is indicative of an illiquid marketplace. Sloppy! In unison...current coupon yield spreads have also gapped wider. This implies we are experiencing focused weakness in the production side of the MBS market (bid wanted).

Here is a snapshot of current indications...

NEXT EVENT: Beige Book at 2pm.

NEXT TARGET: We wanna see 10s break 3.32% and retest 3.30%