The Federal Reserve Board and the Federal Open Market Committee today released the minutes of the Committee meeting held on November 2-3, 2010 and of the conference call held on October 15, 2010. The minutes for each regularly scheduled meeting of the Committee ordinarily are made available three weeks after the day of the policy decision and subsequently are published in the Board's Annual Report.

Reuters Quick Recap...

- Fed officials sharply revised down their forecasts for economic growth next year, and saw unemployment at significantly higher levels than they had the last time they issued official forecasts in June.

- Most participants in the Federal Open Market Committee, the Fed's policy-setting arm, backed the plan to ramp up asset purchases in an effort to bring down long-term interest rates and try to nudge economic activity up a notch.

- In a rare, unscheduled meeting held via videoconference on Oct. 15, policymakers debated a range of new avenues for policy, including the possibility of targeting a specific level of bond yields and enhancing communications by instituting news briefings by Chairman Ben Bernanke.

Here are a few excerpts from the release relating to the economic outlooks of FOMC board members....

ON WHAT'S HOLDING US DOWN...

Participants variously noted a number of factors that were restraining growth, including low levels of household and business confidence, concerns about the durability of the economic recovery, continuing uncertainty about the future tax and regulatory environment, still-weak financial conditions of some households and small businesses, the depressed housing market, and waning fiscal stimulus

ON HOUSING...

"Participants noted that the housing sector, including residential construction and home sales, remained depressed.Foreclosures were adding to the elevated supply of available homes and putting downward pressure

on home prices and housing construction. Some participants saw disputes over mortgage and foreclosure documents as likely to delay the eventual recovery in housing markets."

ON THE LABOR MARKET...

"Participants agreed that progress in reducing unemployment was disappointing; indeed, several noted that the recent rate of output growth, if continued, would more likely be associated with an increase than a decrease

in the unemployment rate. Participants again discussed the extent to which employment was being held down, and the unemployment rate boosted, by structural factors such as mismatches between the skills of the workers who had lost their jobs and the skills needed in the sectors of the economy with vacancies, the inability of the unemployed to relocate because their homes were worth less than the principal they owed on their mortgages, and the effects of extended unemployment benefits on the duration of unemployed workers’ search for a new job."

"A number of participants noted that continued high unemployment, particularly with large numbers of workers suffering very long spells of unemployment, would lead to an erosion of workers’ skills that would have adverse consequences for those workers and for the economy’s potential level of output in the longer term"

ON INFLATION...

"Measures of price inflation had generally trended lower since the start of the recession; the same was true of nominal wage growth. Most participants indicated that underlying inflation was somewhat low relative to levels

that they judged to be consistent with the Committee’s statutory mandate to foster maximum employment and price stability. While underlying inflation remained subdued, meeting participants generally saw only small

odds of deflation, given the stability of longer-term inflation expectations and the anticipated recovery in economic activity. They generally did not expect appreciably higher inflation, either"

While prices of some commodities and imported goods had risen recently, business contacts reported that they currently had little pricing power and that they would continue to seek productivity gains to offset higher input costs. Small wage increases, coupled with productivity gains, meant that unit labor costs were lower than a year earlier. Many participants pointed to substantial slack in resource utilization, along with well-anchored inflation expectations, as likely to contribute to subdued inflation for some time."

ON OPEN MARKET ASSET PURCHASES...

"Participants also differed in their assessments of the likely benefits and costs associated with a program of purchasing additional longer-term securities in an effort to provide additional monetary stimulus, though most saw the benefits as exceeding the costs in current circumstances. Most participants judged that a program of purchasing additional longer-term securities would put downward pressure on longer-term interest rates and boost asset prices; some observed that it could also lead to a reduction in the foreign exchange value of the dollar."

"Most expected these changes in financial conditions to help promote a somewhat stronger recovery in output and employment while also helping return inflation, over time, to levels consistent with the Committee’s mandate. In addition, several participants argued that the stimulus provided by additional securities purchases would help protect against further disinflation and the small probability that the U.S. economy could fall into persistent deflation—an outcome that they thought would be very costly. Some participants, however, anticipated that additional purchases of longer-term securities would have only a limited effect on the pace of the recovery."

"Some participants, however, anticipated that additional purchases of longer-term securities would have only a limited effect on the pace of the recovery; they judged that the economy’s slow growth largely reflected the effects of factors that were not likely to respond to additional monetary policy stimulus and thought that additional action would be warranted only if the outlook worsened and the odds of deflation increased materially.

"Some participants noted concerns that additional expansion of the Federal Reserve’s balance sheet could put unwanted downward pressure on the dollar’s value in foreign exchange markets. Several participants saw a risk that a further increase in the size of the Federal Reserve’s asset portfolio, with an accompanying increase in the supply of excess reserves and in the monetary base, could cause an undesirably large increase in inflation. However, it was noted that the Committee had in place tools that would enable it to remove policy accommodation quickly if necessary to avoid an undesirable increase in inflation."

A summary of economic projections made by Federal Reserve Board members and Reserve Bank presidents for the November 2-3, 2010 meeting was also included as an addendum to the minutes. Summaries of economic projections are released on an approximately quarterly schedule. The descriptions of economic and financial conditions contained in the minutes and in the Summary of Economic Projections are based solely on the information that was available to the Committee at the time of the meeting.

Here is a quick recap. Notice the sizable reductions in growth and expected uptick in the unemployment rate. Productivity and investments in technology are crowding out the middle class blue collar workers!

DJN-DJ FED DOWNGRADES US ECONOMIC PROJECTIONS - FOMC NOV MINUTES

DJN-DJ FED SEES 2010 GDP AROUND +2.5% VS JUNE +3.3% FORECAST

DJN-DJ FED SEES 2011 GDP AROUND +3.3% VS JUNE +3.9% FORECAST

DJN-DJ FED SEES GDP RISING AROUND 4.0% IN 2012, 2013

DJN-DJ FED SEES INFLATION BELOW INFORMAL TARGET UNTIL 2013

DJN-DJ FED SEES 2011 CORE PCE INFLATION BETWEEN 0.9%-1.6%

DJN-DJ FED SEES 2012 CORE PCE INFLATION BETWEEN 1.0%-1.6%

DJN-DJ FED SEES 2013 CORE PCE INFLATION BETWEEN 1.1%-2.0%

DJN-DJ FED SEES 2011 JOBLESS RATE AROUND 9.0% VS JUNE'S 8.5%

DJN-DJ FED SEES 2012 JOBLESS RATE AROUND 8.0% VS JUNE'S 7.3%

DJN-DJ FED UPS LONGER-RUN JOBLESS RATE TO BETWEEN 5.0%-6.0%

The question I was looking to have answered by the FOMC Minutes is...

WILL THE FED CUT THEIR ASSET PURCHASE PROGRAM SHORT? IS THE FED REGRETTING THIS DECISION?

While the FOMC Minutes and an updated economic outlook are more than enough support for the Fed's QEII "strategery", I think we can find the answer to that question in the rush of Fed rhetoric that hit newswires in following an influx of critical comments which were directed at the FOMC in the week's following the QEII announcement...

MINNEAPOLIS FED PRESIDENT NARAYANA KOCHERLAKOTA, Nov. 22

QEII BULLISH: "Inflation and employment are both too low, and the pace of recovery is too slow. Economic growth is low and softening further... I believe that QE is a move in the right direction."

FED CHAIRMAN BEN BERNANKE, Nov. 19

QEII BULLISH: "The best way to continue to deliver the strong economic fundamentals that underpin the value of the dollar, as well as to support the global recovery, is through policies that lead to a resumption of robust growth in a context of price stability in the United States."

PHILADELPHIA FED PRESIDENT CHARLES PLOSSER, Nov. 18

QEII NERVOUS: Some even worry that the economy might fall into a deflationary trap. I am not one of them. Indeed, I am more optimistic than many about the future path of the economy. The committee specifically said we will reevaluate and assess the progress of QEII on a regular basis and I take that assessment in a serious way."

CLEVELAND FED PRESIDENT SANDRA PIANALTO, Nov. 18

QEII BULLISH: "Responding to inflationary and disinflationary pressures gets to the heart of what a central bank can and must do...My belief is that by promoting price stability, the Federal Reserve is following the best course for supporting the economic recovery."

FED BOARD GOVERNOR KEVIN WARSH, Nov. 18

QEII DEFENSE: "Monetary policy has an important role to play...but it is not a predominant role."

ST. LOUIS FED PRESIDENT JAMES BULLARD, Nov. 17

QEII BULLISH: "That disinflation trend is something that I'm worried about and I think we should take action to turn around; that's part of the reason I supported the second round of quantitative easing. As the forecast looks right now it looks like we'll be purchasing at this pace through the end of the second quarter to add up to $600 billion."

BOSTON FED PRESIDENT ERIC ROSENGREN, Nov. 17

QEII DEFENSE: "If the economy were to weaken and we were to get further disinflation and a higher unemployment rate, then we would have to reflect on whether we should take additional action."

ATLANTA FED PRESIDENT DENNIS LOCKHART, Nov. 16

QEII DEFENSE: "There is no monetary policy intent to engineer specific values -- or even a direction-- for the dollar."

CHICAGO FED PRESIDENT CHARLES EVANS, Nov. 16

QEII DEFENSE: "I would continue to want to apply accommodative monetary policy until I had some confidence that that situation was changing," he said, referring to high unemployment and low inflation.

NEW YORK FED PRESIDENT WILLIAM DUDLEY, Nov. 16

QEII DEFENSE: "We have no goal in terms of pushing the dollar up or down. Our goal is to ease financial conditions and to stimulate a stronger economic expansion and more rapid employment growth. It's going to make the economy grow a little bit faster. It's going to generate a little bit more employment growth. But you know, we have a long bumpy road to travel."

FED BOARD VICE CHAIR JANET YELLEN, Nov. 15

QEII BULLISH: "This should not be regarded as some sort of chapter in a currency war. The question is: Do we have an effective policy that we can adopt?...If we do, and it actually produces expected benefits and addresses risks that we face, then there is a clear case for doing it, even if it is not going to be a panacea."

RICHMOND FED PRESIDENT JEFFREY LACKER, Nov. 13

QEII BEARISH: "The decision has been made. I was one who thought the risks exceeded the benefits."

It seems like the Fed's defensive bully-pulpitting has been an effective means of quieting QEII opposition doesn' it? I haven't heard much from the inflation hawks or rouge republicans lately. Have you? Barring a major spike in economic activity and corresponding labor market recovery, it looks like QEII is here to stay...just like the MBS purchase program was here to stay.

Plain and Simple Recap: Although there were mixed opinions on the cost/benefit relationship of QEII, 10 of 11 voters felt it was a necessary evil and overall, the Committee believes it has tested enough exit strategies to avoid excessive expansion of the monetary base. Based on the Fed's economic downgrades and the generally vulnerable recovery sentiments shared, it doesn't appear likely that we'll see QEII cut short either.

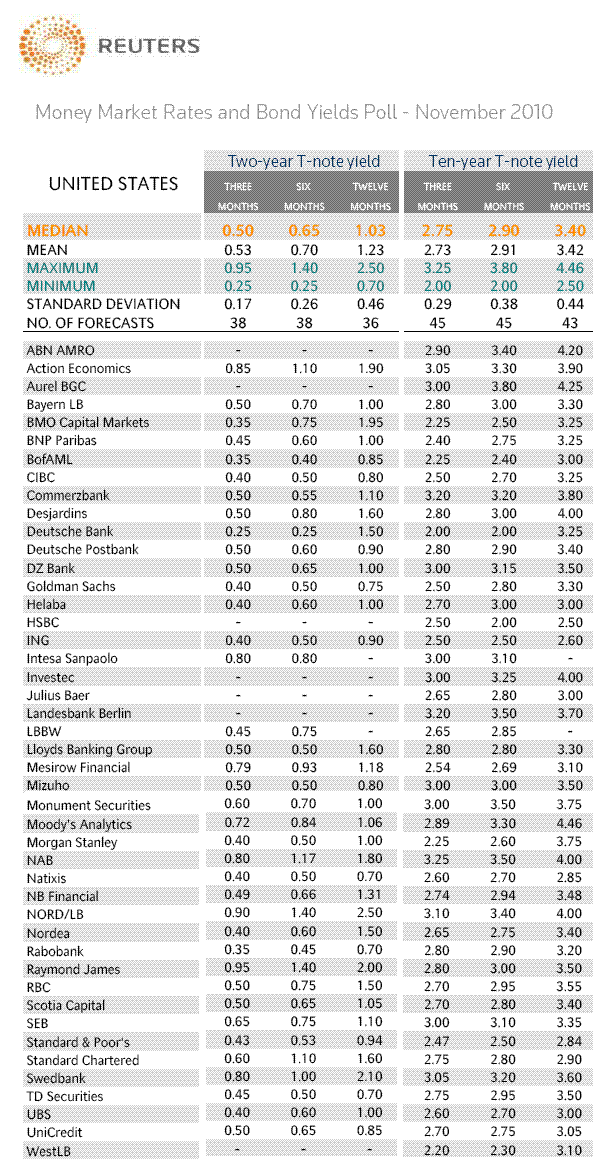

Here are the results of a Reuters poll on where the market thinks bond yields will venture in the months ahead. Uncertainty is obvious via a 125bp range in 10yr notes.