Stocks aren't really budging from their recent range but benchmark yields are lower and "rate sheet influential" MBS coupons are bid 8 to 10 ticks higher....

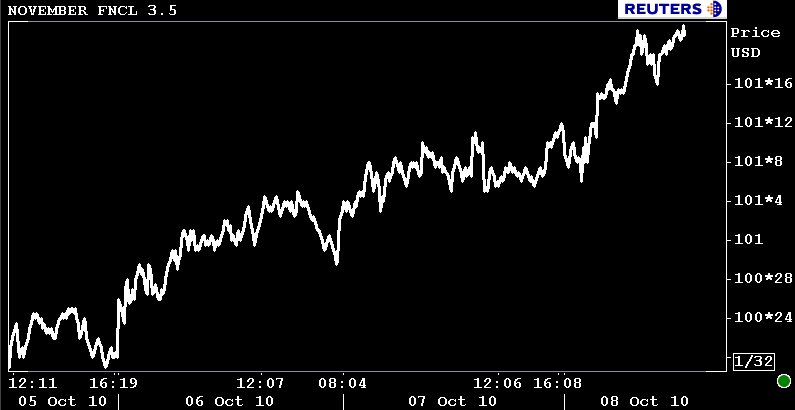

I have waited and waited and waited to do this but I think I can safely award the 3.5 MBS with the official production coupon designation. YAY! 30 year 3.5s have actually been the primary pipeline hedging coupon all week, but like the rest of the bond market I was hesitant to move lower before getting confirmation from the Employment Situation Report today. The funny thing is, with 3.0s bid in the 99 handle (not executable in any size) the current coupon should technically be weighted more with the 3.0 vs. the 3.5. We are not going there yet...but we will continue to keep an eye on the mortgage options market for hints of 3.0 supply to come.

Let's give the 3.5 it's moment of glory before we get back to business....woohoo yay par rates below 4.00%! Ok moving on..

The November delivery FNCL 3.5 is +10/32 at 101-31. The Nov. FNCL 4.0 is +9/32 at 103-31. I've got the current coupon marked at 3.333%. I know the street is lower but I run my current coupon using the MBS coupons that are seeing supply delivery. I am weighted 80% 3.5s and 20% 4.0s. Here are my spreads: +99.2bps/10yrTSY, +88.4bps/10yIRS, +225/5yTSY.

The Nov. FNCL 4.0 continues to follow our internal trend channel higher...

re: THE EMPLOYMENT SITUATION REPORT

This was my Plain and Simple of the data: Overall, headline data was weaker than expected, but I would rather describe it as "BLAH". I think ADP summed it up perfectly when they said there is "NO MOMENTUM IN EMPLOYMENT". The market will focus on continued growth in private payrolls though and while only 64k jobs were added by private industry in Sept (less than forecast), August Private Payrolls were revised for the better, significantly! (from +67k to +93k). Plus, private payrolls have grown in 9 of the last 10 months, so that is a positive. Furthermore, job losses are focused in construction, manufacturing and government (local government = teachers, fireman, and police). When you strip out Census layoffs, the total payroll decline was "only" 18,000. Now for the bad news....14.1 million Americans are considered unemployed by BLS, 6.1 million of those folks have been out of work for longer than 27 weeks and the real unemployment rate when you include discouraged workers and those marginally attached to the labor force rose 0.4% to 17.1%. Private Industry might be adding jobs but a large portion of America is being left behind.....

5s continue to be the richest spot on the curve, currently bid 6/32 higher at 100-25 yielding 1.088% (ugh so low). 10s are +10/32 at 102-13 yielding 2.349%. The 2s/10s curve is 2bps flatter at 200 wide.

Rate sheets are being released and from I've seen so far par notes are paying about 25 extra bps. I haven't updated my model yet but will post a comparison ASAP...