THE EMPLOYMENT SITUATION REPORT- September 2010

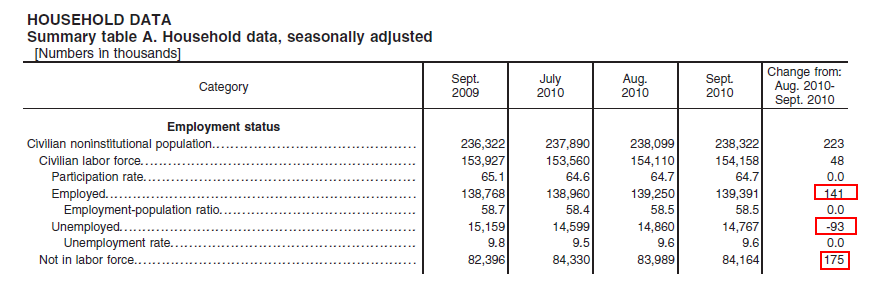

QUICK RECAP: NFP: -95K vs. call for UNCH vs. Aug -57K. Private Sector +64K jobs vs. call for +75. vs. +93K in August. Government job cuts total 159K vs. 150K in August. Unemployment Rate: UNCH at 9.6%. Average Hourly Earning UNCH vs. call for +0.2% vs. +0.3% in Aug. Average Hourly Work Week at 34.2 hours, on the screws and UNCH vs. Aug.

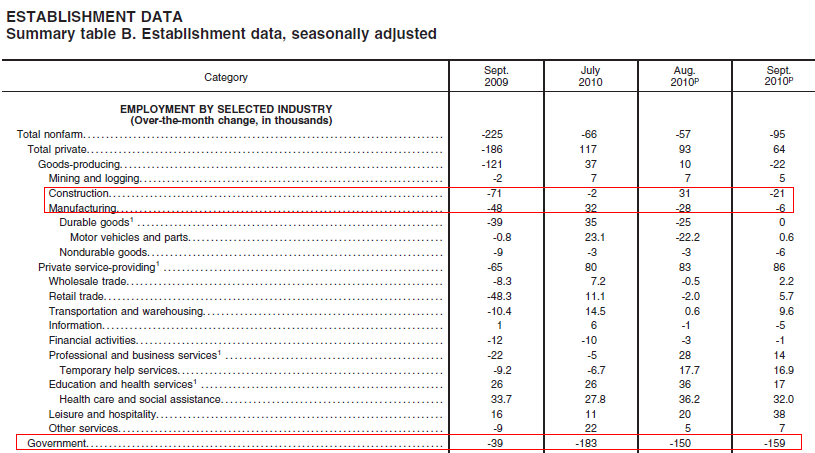

Total nonfarm payroll employment edged down by 95,000 in September. Government employment fell by 159,000, reflecting both the departure of 77,000 temporary Census 2010 workers from federal government payrolls and a decline of 76,000 in local government employment. Private-sector payroll employment continued to trend up (+64,000) over the month.

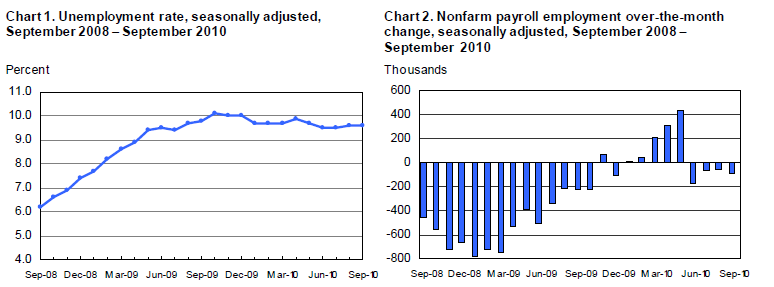

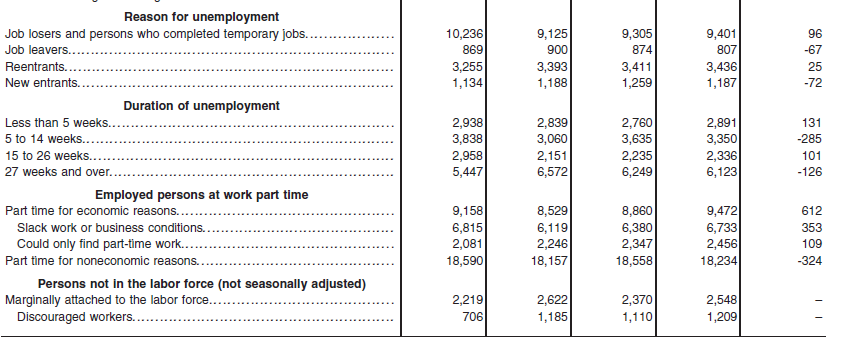

The number of unemployed persons, at 14.8 million, was essentially unchanged in September, and the unemployment rate held at 9.6 percent. (175,000 people exited the labor force which helped keep the unemployment rate from rising.)

The number of long-term unemployed (those jobless for 27 weeks and over), at 6.1 million, was little changed over the month but was down by 640,000 since a series high of 6.8 million in May. In September, 41.7 percent of unemployed persons had been jobless for 27 weeks or more.

Government employment fell by 159,000 in September. A decline in federal government employment was due to the loss of 77,000 temporary Census 2010 jobs. As of September, about 6,000 temporary decennial census workers remained on the federal government payroll, down from a peak of 564,000 in May. Employment in local government decreased by 76,000 in September with job losses in both education and noneducation.

JOB LOSSES WERE HIGHLY CONCENTRATED IN TWO SECTORS: CONSTRUCTION, our world, AND GOVERNMENT JOBS

Plain and Simple: Overall, headline data was weaker than expected, but I would rather describe it as "BLAH". I think ADP summed it up perfectly when they said there is "NO MOMENTUM IN EMPLOYMENT". The market will focus on continued growth in private payrolls though and while only 64k jobs were added by private industry in Sept (less than forecast), August Private Payrolls were revised for the better, significantly! (from +67k to +93k). Plus, private payrolls have grown in 9 of the last 10 months, so that is a positive. Furthermore, job losses are focused in construction, manufacturing and government (local government = teachers, fireman, and police). When you strip out Census layoffs, the total payroll decline was "only" 18,000. Now for the bad news....14.1 million Americans are considered unemployed by BLS, 6.1 million of those folks have been out of work for longer than 27 weeks and the real unemployment rate when you include discouraged workers and those marginally attached to the labor force rose 0.4% to 17.1%. Private Industry might be adding jobs but a large portion of America is being left behind.....

Market Reaction....

Initially there was no reaction but once everyone got a chance to absorb the headlines and dig a little deeper, directional activity began to pick up.

Bond yields are now lower with 5s and 10s leading the curve, although improvements are tiny. The 10yr note is currently +0-04 at 102-07 yielding 2.371% (-1.6bps). 5s touched a new record low again and are currently +0-02 at 100-21 yielding 1.112% (wow that is a terrible 5yr return).

The Nov. FNCL 3.5 is +0-05 at 101-16 and the Nov. FNCL 4.0 is +0-05 at 103-17. Call Guinness because these are new record price highs. Vol is getting smashed.

Stocks ticked lower then stocks ticked higher because stocks see reason to rally no matter what the data says....data = bad, then the Fed implements QE, stocks likey. Data = strong, no QE but doesn't matter because stocks are cheap and the economy is slowly recovering, which basically means "time to do some bargain buying", just don't buy the banks. It's a win/win for equities.

More to come...for now we should be expecting loan pricing to at least be UNCH vs. yesterday, most desks should pass on marginally better rebate though.