- JULY FNCL 4.5: +0-05 at 103-00 (103.00) AUGUST FNCL 4.5: +0-03 at 102-19

- Secondary Market Current Coupon: -2.0 bps at 3.973%

- CC Yield Spreads:+72.6bps/10yTSY. +70.2bps/10yIRS. Much tighter vs. Friday 5pm marks

- UST10YR: +2.2ps at 3.247%. 2s/10s: 3bps STEEPER at 253bps

- S&P CLOSE: -0.39% at 1113.20. HIGH: 1131.08 LOW: 1108.11

- BEST SECTOR: Materials +0.44% (on Yuan appreciation) WORST SECTOR: Consumer Discretionaries -0.89% (on Yuan appreciation. less exports)

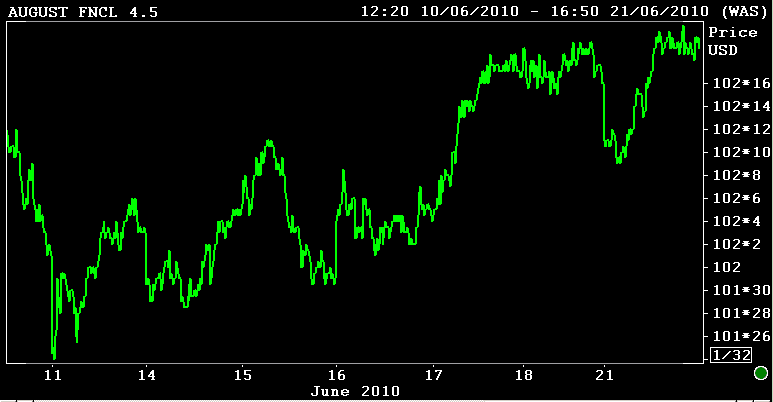

Although we got off to a slow start, "rate sheet influential" MBS traded well today. Prices rallied from early morning lows, yield spreads tightened, and lenders repriced for the better. This left loan pricing close to what was being offered on Friday (aggressive rebate!). From a technical perspective, mortgage valuations continue to benefit from a lack of new loan supply and below average trading volume.

30 day locks are based on the August FNCL 4.5 coupon. At this point in the month, all 15 day loan pricing is based on August indications as well..

Pipeline pull-through is decent and rate float downs haven't been much an option for most folks lately.

Thinking forward, because loan officers are closing their loans (pull-through!) and commitment buckets aren't losing much water (salable loan paper), smaller more aggressive secondary marketing departments are probably underhedged and playing the market as price levels bounce around a rich range (not as much with the majors). This gives loan traders an opportunity to earn extra profit margin on new applications (when MBS prices rise)...but leaves the lock desk much more sensitive to downward fluctuations in MBS prices.

Plain and Simple: This is one of those environments where reprices for the worse will come way faster than reprices for the better. It took 10 ticks for lenders to pull the trigger today! Fells Wargo has been an example of how sensitive lenders are at the moment.

ps. don't read into this as a bearish directional bias. The range trade is in play and markets are still acting non-committal. Plus...even though weak housing data is on the radar of market watchers, the pending FOMC statement will prevent participation from accumulating and keep both stocks and bonds from moving too far in either direction. Anyone think the S&P tests the 200 day moving average again this week? READ MORE