"Rate sheet influential" benchmark Treasury yields and MBS prices made modest improvements yesterday in a sluggish trading session.

The day began on a sour note as 10s touched 3.695% in the early hours of the N.Y. session. This led current coupon MBS bids lower at the open. That didn't last long though---soon thereafter the stock lever engaged and risk-averse interest rate markets benefited from flight to safety attention and a bargain buying "duration adding" bid.

This led the 10 year note on a 3 basis point barnburner rally from its weakest levels of the day (note sarcasm), helping new production mortgages recover AM price losses. Lenders who published pricing before the NYSE opening bell were able to reprice for the better by late lunch hours. Reprices for the better were not broad based though.

Benchmark Treasury yields and “rate sheet influential” MBS valuations moved in a tight sideways range for most of the day...storing up energy for a more influential event yet to print.

The 3.625% coupon bearing 10 year Treasury note ended the day +0-08 at 99-22 yielding 3.664 while the FN 4.5 went out +0-07 at 101-02 yielding 4.38%. The secondary market current coupon was 4.332%. At 5pm my yield spread scorecard read: +67.1bps over the 10 year Treasury yield and +64.2 basis points over the 10 year swap rate. Yield spreads were slightly wider but basically unchanged on the day. Activity in the TSY futures market was uncommonly low while MBS trading volume was well below recent averages as new loan supply from originators looks to have peaked late last week.

Stocks fought off pre-market pessimism surrounding a lack of Greece bailout unity (Merkel said it would be last resort. Not happening at EU Summit this week) and rallied on the passage of historic health care reform. Treasuries managed to maintain marginal gains as traders added did some duration adding ahead of $118 billion in auction supply...which appears to have been adequately priced into the market last week (more like over kill flattening) READ MORE.

Consumer Discretionaries were at the head of their class while the Utilities sector sucked strength from the S&P 500.

In overseas activity the SHANGHAI fell 0.7%, the HANG SENG gained 0.26%, the NIKKEI lost 0.47%, the DAX is up 0.18%, the CAC is +0.46%, and the FTSE is +0.44%

There isn't much news to discuss from overnight trading. 'Ol faithful did rear its hideous head again though. In yet another dramatic twist in the Greek epic, it is said that EU officials are attempting to draft some form of compromise to bring aid to Greece before the commencement of the EU Summit on Thursday. Greek says they will handle their business on their own. Just so you get an idea of what I mean, here is a statement from Greek Finance Minister George Papaconstantinou: "Let me be clear, Greece has not asked for financial aid from anyone. We are not asking someone to save us....But for those countries that do what they are supposed to do, there must be some sort of [European] mechanism to ensure stability."

So...you don't want help but there must be some sort of mechanism to support stability??? READ MORE. I don't know why I am even talking about this...I bet more than half of you saw the word Greece and said "just let me know when its over"

OK. Perhaps this next bit of news might be noteworthy: JAPAN TO FACE FUNDING SHORTAGE IN 2011/2012. Japan is having fiscal problems? You dont say...(please note extreme sarcasm). READ MORE

US stock futures were super sideways overnight....YAWN!

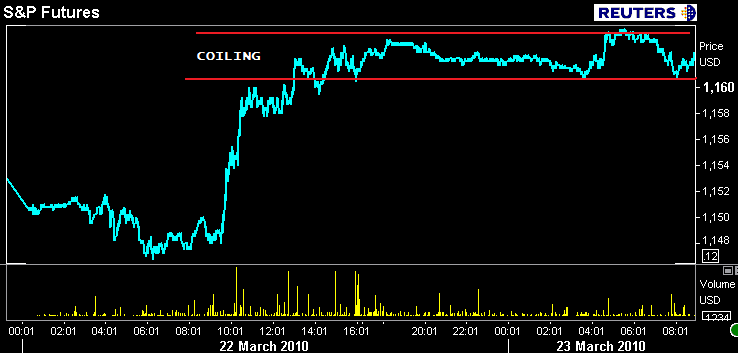

Treasuries did the same...more coiling/energy storage. Volume was pathetic....

OK. Given the overnight developments I just shared...take a guess at where the FN 4.5 is bid at the moment.

DID YOU SAY PROBABLY FLAT????

YAAH!!! YOURE RIGHT!!! FLAT. The FN 4.5 is +0-00 at 101-02 yielding 4.38%. The secondary market current coupon is 4.332%.3m/10yr and 5yr/10yr vols are higher. Nominal yield spreads are wider vs. 5pm marks.

No need to go too deep into this outlook. Markets have been "coiling" energy, waiting for an influential event that provided direction and justified broader participation. Existing Home Sales will print at 10AM followed by $44 billion 2 year notes at 1pm with a House Financial Services Hearing on Housing Finance at 10AM. The short end of the yield curve looks cheap.....steepener anyone?