We've been waiting for this moment for almost 9 months. It has finally come. Beware, there's gonna be some "horn tootin" in this commentary...

From: Bond Market Repeating History. False Start Fuels Rally

Here we are again. History seems to be repeating itself as we head into the summer months.

The market got all excited about a speedy economic recovery following a seasonal uptick in consumer spending and positive progress in the labor market only to find that those improvements weren't sustainable in the real world where Main Street wasn't able to accumulate wealth or deleverage at a fast enough pace because only high-skilled labor is being awarded wage hikes and home buyer demand is in the toilet right along with home prices.

The same thing happened last year. Street economists upgraded quarterly growth projections only to be disappointed by unsustainable momentum down the road, which brought on downgrades and a return to "long road ahead" reality. We've described this behavior as a "false start". It can be brought on by homebuyer credits, payroll tax cuts and quantitative easing efforts or any other inorganic effort that distorts perspectives of economic reality. And it can be easily erased by unexpected events like earthquakes and floods.

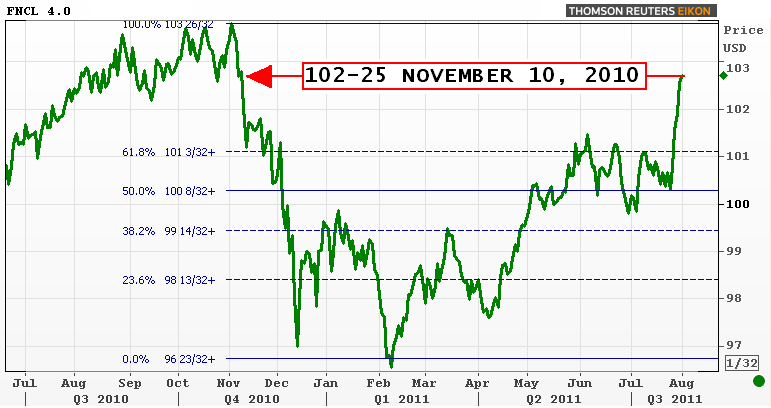

We started to see history repeating itself last December and pointed it out here. Signs of underlying economic weakness were observed early and often, our fundamental view was recapped and confirmed here. Primary dealers and economists even threw cold water on our outlook here, that didn't skew our perception of reality though. And then, using a color coated chart, we showed you why benchmark 10yr yields would touch 2.85% and drift higher before breaking through 2.85% resistance and moving toward our long-standing trend channel. THIS CHART IS AWESOME

And now, after benchmark 10s touched 2.85% and sold off as our technical analysis suggested, we've witnessed rates rally back through 2.85% resistance and reenter the "originator friendly" trend channel (RED) that was originally called out after the bond market went into duration shedding mode in November and December 2010. Now we can proudly proclaim....

HISTORY HAS OFFICIALLY REPEATED ITSELF.

TOOT............TOOT

Unfortunately rate sheets don't exactly reflect the fact that the economy and benchmark interest rates have "repeated history". Primary/secondary spreads are much wider than they were when the Fannie Mae 4.0 MBS coupon last visited its current levels (November 10, 2010). Don't get me wrong, a borrower with no exposure to LLPAs could pay a point and get 4.25 today on C30 product, rebate just isn't as aggressive as it was in early November 2010.

WHY?

Volatility is not a friend to MBS valuations, loan pipelines or rate sheets. Anytime TBAs move sharply, as they have over the past four sessions, lenders are left with extra hedging costs. These additional costs, which include fewer deliverable loans as deals fallout as well as market losses incurred on MBS short positions (that is how lock desks hedge against interest rate risk, by selling MBS), must be recovered. That can happen either by adding new loan production to the pipeline or by an MBS sell-off that allows the desk to buy back their MBS hedges at cheaper prices (or a well-timed roll/coupon swap). The speed and size of the recent rally was simply too big and too quick, secondary didn't have a chance to adjust their hedging strategies before rates plummeted. And now we're all playing catch up and loan pricing is suffering as a result. There is another variable in the mix as well. Some lenders have been adjusting their servicing models and reducing SRP values. That further explains the extra margin in your rate sheets. It's not all a factor of extra juice (MLOs describe it as "greed"), it's a loss of income.

NOW WHAT?

Stability is a friend to MBS valuations, loan pipelines and rate sheets. A range trade would be nice, maybe even a slow uptrend toward higher prices and steady decline in current coupon yields. In the immediate future we'll need the Employment Situation Report, which prints on Friday morning, to play along because if it beats expectations by a large margin you can bet your bps that traders will gladly take the opportunity to cheapen up Treasuries before next week's auction cycle (3s/10s/30s). If that scenario plays out we could see benchmark 10s retest 2.85%. If that scares you. Lock now. On the flip side, even if July jobs data confirms the economy has totally stalled, we're not sure how much lower rates can run without added motivation, not with auction supply just ahead. Fundamental weakness is likely baked in already. That implies rates will move sideways in a potentially wide range (2.52 to 2.85) for the next few weeks as the market awaits new guidance. If that makes you hesitant to float, lock now. Just remember, stability will give lenders a chance to close the gap in loan pricing.

That's a short-term point of view though. Looking a bit further out we're focused on the annual Global Central Bankers Conference in Jackson Hole, Wyoming at the end of August. This is the perfect setting for Ben Bernanke to begin hinting at new measures aimed at stimulating the economy. Either that or Ben is going to bluntly alert us that he has no immediate solution for the housing market or the soon-to-be lost generation of low-skilled laborers (replaced by productivity gains and automation). That would be a major confidence killer though, not something the Fed generally advocates. That's why we look for Ben to use the bully-pulpit as much as possible in the next few months because he recognizes how sensitive the global consumer is to rising commodity prices. That'll likely start with increased dovish rhetoric about cost-push inflation subsiding and growth stagnating which will evolve into a rumor-mill of underground QE whispers as Fed speakers sound off into the Fall.........just like they did last year. That certainly takes repeating history to a whole new level. Are we turning Japanese?

Economic outlook assumptions are still based on assumptions of assumptions. Perceptions of reality are constantly skewed. It's a trader's world, we just live in it...

At least for now the reality of a long road to recovery has been restored.