The BEA has released Q3 Preliminary GDP data. The GDP estimates released today are based on more complete source data than were available for the advance estimate issued last month. In the advance estimate, the increase in real GDP was 2.0 percent. Q3 Advance GDP data was released on October 29th. The final estimate for the third quarter, based on more complete data, will be released on December 22, 2010.

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 2.5 percent in the third quarter of 2010, (that is, from the second quarter to the third quarter), according to the "second" estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP increased 1.7 percent.

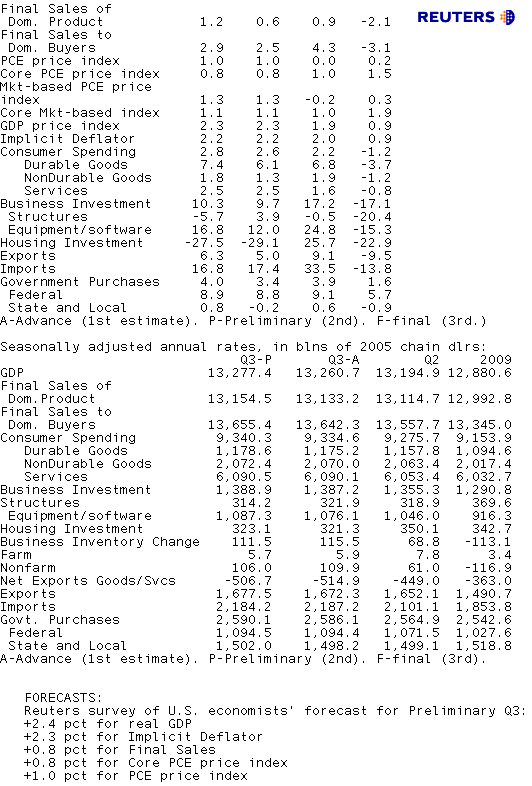

The increase in real GDP in the third quarter primarily reflected positive contributions from personal consumption expenditures (PCE), private inventory investment, nonresidential fixed investment, exports, and federal government spending that were partly offset by a negative contribution from residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The acceleration in real GDP in the third quarter primarily reflected a sharp deceleration in imports and accelerations in private inventory investment and in PCE that were partly offset by a downturn in residential fixed investment and decelerations in nonresidential fixed investment and in exports.

Reuters Quick Recap...

RTRS-US PRELIM Q3 GDP +2.5 PCT (CONSENSUS +2.4 PCT), PREV +2.0 PCT;

RTRS-US PRELIM Q3 FINAL SALES +1.2 PCT (CONS +0.8 PCT), PREV +0.6 PCT

RTRS-US PRELIM Q3 GDP DEFLATOR +2.2 PCT (CONS +2.3 PCT), PREV +2.2 PCT

RTRS-US Q3 PCE PRICE INDEX +1.0 PCT (CONS +1.0 PCT), PREV +1.0 PCT;

RTRS-US Q3 CORE PCE +0.8 PCT (CONS +0.8 PCT), PREV +0.8 PCT

RTRS-US Q3 CONSUMER SPENDING +2.8 PCT (PREV +2.6 PCT), DURABLES +7.4 PCT (PREV +6.1 PCT)

RTRS-US Q3 MARKET-BASED PCE PRICE INDEX +1.3 PCT (PREV +1.3 PCT), CORE +1.1 PCT (PREV +1.1 PCT)

RTRS-US Q3 BUSINESS INVESTMENT +10.3 PCT (PREV +9.7 PCT), EQUIPMENT/SOFTWARE +16.8 PCT (PREV +12.0 PCT)

RTRS-US Q3 HOME INVESTMENT -27.5 PCT (PREV -29.1 PCT), BUS. INVESTMENT IN STRUCTURES -5.7 PCT (PREV +3.9 PCT)

RTRS-US Q3 EXPORTS +6.3 PCT (PREV +5.0 PCT), IMPORTS +16.8 PCT (PREV +17.4 PCT)

RTRS-US Q3 GDP EX MOTOR VEHICLES +2.0 PCT (PREV +1.6 PCT)

RTRS-US Q3 YEAR-ON-YEAR PCE PRICE INDEX +1.4 PCT (PREV +1.4 PCT), CORE PCE +1.3 PCT (PREV +1.3 PCT)

RTRS-US Q3 BUSINESS INVENTORY CHANGE +$111.5 BLN (PREV +$115.5 BLN)

RTRS-US Q3 BUSINESS INVENTORY CHANGE ADDS 1.30 PERCENTAGE POINT TO GDP CHANGE

RTRS-TABLE - U.S. Q3 GDP revised to +2.5 percent

Plain and Simple: Final Sales were revised higher from +0.6% to +1.2% led by domestic purchases (+2.9% vs. previous +2.5%), specifically a 2.8% jump in consumer spending and a 10.3% rise in business investment. Core inflation was unchanged at an anemic +0.8%.

Market Reaction...

2s/10s curve off flattest levels of session. 2s/10s at 230bps wide. 10s tick below 2.75%, currently +16/32 at 98-29+ yielding 2.749%. Janaury FNCL 4.0s are +8/32 at 101-19. Production coupons are wider vs. the curve. S&P futures are holding near session lows regardless of positive domestic data. READ MORE ABOUT OVERNIGHT EVENTS

I will be out of office until 11am.