The risk trade is off this morning, the yield curve is bull flattening and "rate sheet influential" benchmarks have broken a key resistance level.

Two main sources can be cited for further positive progress in the QEII cleansing process....

- Reuters: North Korea fired dozens of artillery shells at the island in one of the heaviest bombardments on the South since the Korean War ended in 1953. The attack comes just as a U.S. envoy is traveling to the region after revelations that the North is moving ahead with uranium enrichment, a possible second path to manufacture material for atomic weapons. "The United States is firmly committed to the defense of our ally, the Republic of Korea, and to the maintenance of regional peace and stability," the White House said, adding that it was in close and continuing contact with South Korea over the situation. A U.S. official, speaking on anonymity, told Reuters that U.S. forces in Korea were closely monitoring the situation. But no U.S. troops were involved in the response to the North's artillery fire, the official said. There are around 28,000 U.S. forces stationed in South Korea.

- Independent.ie: The Government was thrown into crisis today after Fianna Fail's coalition partners, the Green Party, called for a general election to be held. John Gormley, Green Party leader and Environment Minister, said he wanted a date for the vote to be set some time in the second half of January. The dramatic call comes less than 24 hours after Cabinet ministers agreed to ask the International Monetary Fund and Europe for a multibillion euro bail-out. Mr Gormley said: "The past week has been a traumatic one for the Irish electorate. People feel misled and betrayed. "But we have now reached a point where the Irish people need political certainty to take them beyond the coming two months. So we believe it is time to fix a date for a general election in the second half of January 2011."

Plain and Simple: Ireland won't be able to obtain a bailout package without the support of the opposition party until anger subsides and cooler heads prevail. That means the fate of Ireland's government/financial stability is still up in the air. North Korea fired on South Korea. Two people were killed. South Korea fired back. Shares in China fell 1.94% on the news and stocks in Hong Kong declined 2.67%. North Korea hates America but we don't need to be spending more money on another war right now, we need to win the war at home against our economy first. Civil unrest is scary and so is a country who ignores the requests of global super powers. Flight to safety seems like a very appropriate description of the market's behavior this morning.

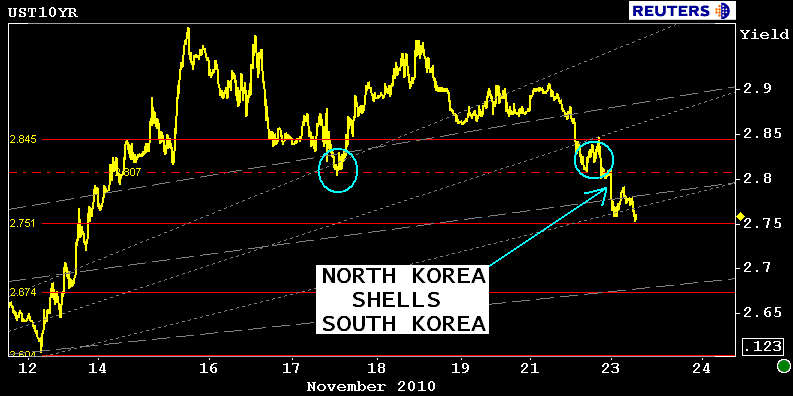

Flows were scattered but bond trading volume was healthy in the overnight session despite Japan being out for their Labour Thanksgiving Day. 216,000 10yr contracts had traded hands of 730am. That is above average. The rally in the long end of the curve took flight following an oversubscribed 2-year note auction yesterday but didn't break resistance until North Korea starting shelling South Korea (they've been at war for the last 57 years btw). This is all happening with the Fed's QEII purchases basically done for the week. At 10:15am today the desk will lift $2-3 billion TIPS coupons maturing between 2012 and 2040, but that's it until next Monday.

Most of the trendlines, pivots, and inflection points on the chart below you have seen...except the dotted red line at 2.80%. I added this resistance line because 10s haven't been below 2.80% since November 14. We broke 2.80% overnight.

Just last Monday this selloff felt unstoppable. Now at least we're seeing a little more of battle between the bargain buyer bulls and the short selling robots/ inflation hawks/reds. The pain trade is just about washed out and we're setting up for some directional movement (in either direction), with our rally base seen between 2.75% and 2.85% in 10s. Curve longs at 236bps wide. Momentum is shifting more neutral after much liquidation of Treasury longs in COT .Technicals are still bearish but there was tactical position squaring seen via short covering yesterday. Open interest has yet to really shift in favor of the longs but volatility did cheapen up nicely. An indication that real money investors may have taken the CHEAPEST TO DELIVER hedge in an instrument with its own embedded call...the 10yr futures contract.

10s are testing a more important inflection point now....2.75%. A breakdown of this resistance accompanied by some follow through position adding (longs) would be a big step toward 3.5s trading in size again.

Equity futures are at their session lows. S&Ps are -14 at 1184. Dow futures are -108 at 11,057. The dollar index is up sharply in the last 24 hours and is adding to those gains this morning, currently +0.49% at 79.066. Commodities are down across the board led by a 2.79% decline in Natural Gas and a 2.44% dip in Silver prices. Light crude is down 1.70%. Gold is off 0.55%.

The day ahead is busy with Q3 GDP Revisions at 830am, Existing Home Sales at 10am, $35bn 5s at 1pm, and the headline event, the FOMC Minutes at 2pm.

Key Events Today...

8:30 ― Revisions to third-quarter GDP are

expected to boost the measure to an annualized rate of 2.4%, up from

the original projection of 2%. Estimates from the 64 economists polled

by Thomson Reuters range from 2% to 2.8%.

“Recent economic

indicators such as business and wholesale inventories, new residential

construction and net external demand point to a stronger economic

activity in 3Q10 than previously estimated,” said economists at BBVA.

Forecasters

at IHS Global Insight say inventory accumulation should provide a

bigger boost than original estimates, while foreign trade should be less

of a drag. However, private nonresidential construction should see

large downward revision.

Projecting into the current quarter, IHS says to expect 2.5% growth. Embedded in this report is the Core PCE Price Index. This is the Fed's preferred gauge of inflation. The preliminary read on Core Inflation was +0.6% QoQ. That is VERY weak core inflation.

10:00 ― Existing Home Sales are

expected to take a slight hit in October. Forecasters expect to see an

annualized pace of 4.50 million sales, down from 4.53 million in

September. Estimates from 60 economists range from 4.20 to 4.80 million.

The pessimism largely stems from the 1.8% drop in September’s pending

home sales index, versus the consensus call for a 3% gain. The PHSI

tracks contract signings, thereby anticipating secondary market sales by

a month or two.

Against the consensus, economists at Nomura Global Economics look for a 1.5% increase to 4.60 million sales.

“Despite

rapid growth over the past two months, the level of existing home sales

remains a bit low compared to pre-federal tax credit levels,” they

wrote. “We therefore think sales could rise further this month, despite

the weakness in the pending home sales index (a leading indicator of

existing home sales).”

On the lower end of the spectrum, economists at IHS Global Insight expect a 6% tumble.

“The

Pending Home Sales Index slipped 1.8% in September, and mortgage

applications to buy homes fell during October, according to the Mortgage

Bankers Association,” they wrote. “The foreclosures mess which led to

halts in foreclosures from some mortgage lenders contributed to the

expected decline in sales.

2:00 ― Given the unprecedented attacks on the Federal Reserve in recent weeks, there should be lost of appetite to read the FOMC Minutes of

the Nov. 2-3 policy meeting. The resulting communique detailed the

central bank’s plan to renew quantitative easing efforts with $600

billion of new asset purchases. The minutes should detail how much

support chairman Ben Bernanke had in launching the program.

“The

QE2 decision is under attack from many quarters ― including from some

members of the committee ― and markets have reacted violently since the

meeting,” said economists at Nomura. “There is a clear need for formal

communication on the latest policy action from the Fed. Indeed, the

minutes of the last FOMC meeting specifically noted that the committee

itself regards this document as ‘an important channel for communicating

participants' views about monetary policy.’”

The minutes will also provide the Fed’s first updates on GDP, unemployment and inflation since the late June meeting.

“We

expect major downward revisions to the Fed's forecasts for growth and

core inflation, and an upward revision to forecasts for unemployment,”

said Nomura.

Treasury Auctions:

- 11:30 ― 4-Week Bills

- 1:00 ― 5-Year Notes