Jobless Claims data has been released. Before we go any further, this report has no bearing on the September Employment Situation Report, which will be published tomorrow morning, nor will it have much influence over the October report. More on that below...

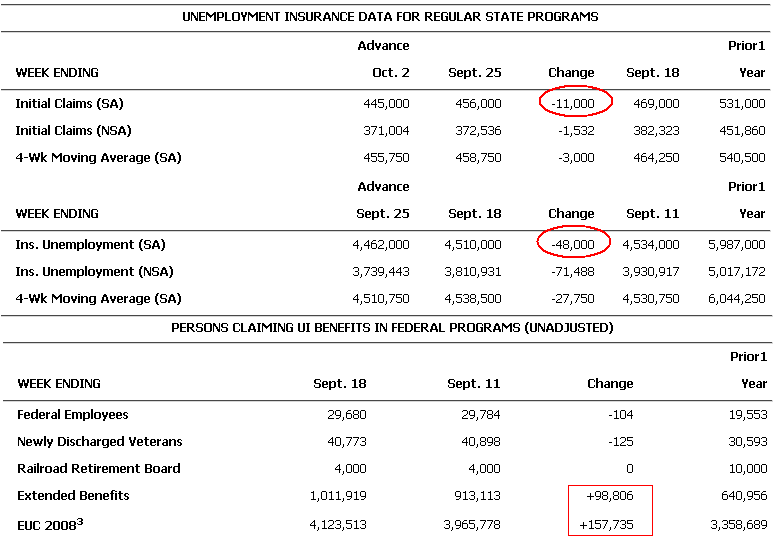

Quick Recap: Jobless Claims. -11,000 to 445,000 (better than expected). Continuing Claims -48,000 to 4,462,000 (worse than expected). Extended Benefits +98, 806. Emergency Benefits +157, 735

08:30 07Oct10 RTRS-US JOBLESS CLAIMS FELL TO 445,000 OCT 2 WEEK (CONSENSUS 455,000) FROM 456,000 PRIOR WEEK (PREVIOUS 453,000)

08:30 07Oct10 RTRS-US JOBLESS CLAIMS 4-WK AVG FELL TO 455,750 OCT 2 WEEK FROM 458,750 PRIOR WEEK (PREVIOUS 458,000)

08:30 07Oct10 RTRS-US CONTINUED CLAIMS FELL TO 4.462 MLN (CON. 4.450 MLN) SEPT 25 WEEK FROM 4.510 MLN PRIOR (PREV 4.457 MLN)

08:30 07Oct10 RTRS-US INSURED UNEMPLOYMENT RATE FELL TO 3.5 PCT SEPT 25 WEEK FROM 3.6 PCT PRIOR WEEK (PREV 3.5 PCT)

08:30 07Oct10 RTRS-US JOBLESS CLAIMS LOWEST SINCE WEEK ENDED JULY 10, 2010 (427,000)

08:30 07Oct10 RTRS-TABLE-U.S. jobless claims fell in latest week

re: Jobless Claims and the September Employment Situation Report

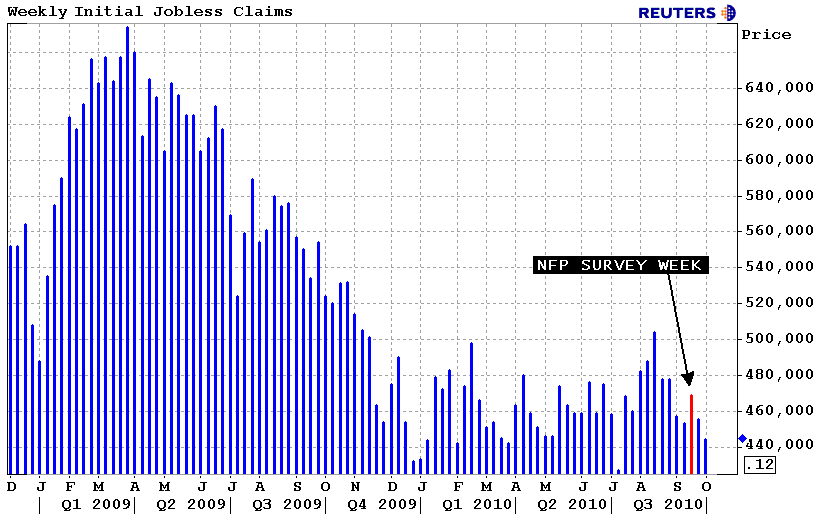

The BLS and Census Bureau generally conduct their surveys for the official Employment Situation Report in the week that contains the 12th day of the month or the pay period including the 12th. The joless claims report that provides a hint into what we might see tomorrow would be data for the week ending Sept.18th. In that week, jobless claims were at 469,000....this would imply forecasts for a 75,000 improvement in private payrolls might be a bit too high....ADP AGREES

Employment Situation Report Preview...

Economists polled by Reuters currently believe the report will show the labor market was flat last month after 54k jobs were lost in August. Private employment is expected to have increased by more than 80k in the month, but that increase was offset by the expiration of temporary Census jobs. The Unemployment Rate, currently at 9.6%, is expected to remain put or rise by one-tenth.

“The labor market evidence continues to point to job creation, but at a slow pace,” said economists at IHS Global Insight. “We expect headline employment to fall 5,000, as more than 70,000 temporary Census workers were released in September. This is the last time that Census layoffs will distort headline employment, because only 6,000 temporary Census workers remained in place as of mid-September.”

Economists at Deutsche Bank point out that the report takes on added significance because it is the last jobs report the Fed will see before its November 2-3 FOMC meeting, when further quantitative easing initiatives are expected.

Also, the BLS will release an estimate for annual benchmark revisions to the prior year of data.

“Last year at this time the BLS announced a tentative 824k downward revision to the level of March 2009 payrolls, the biggest ever,” Deutsche Bank noted. “The fact the economy has been growing over the past four quarters — it grew 3.7% in Q1 2010 — suggests to us the preliminary benchmark revisions announced by the BLS next week will be positive.”

LOCK/FLOAT THOUGHTS: If the data doesn't match expectations, 10s would move into the low 2.30s% and rebate would improve a few more bps while MBS would lag a continued rally in benchmarks. Unless the Employment Situation Report is much much better than expected, I doubt the bond market reacts in a manner that leads to a trend of higher mortgage rates. However, considering the extent to which the bond market has already baked in more quantitative easing, if NFP comes in on target or beats, we would likely see knee jerk selling heading into the long weekend. This would allow traders to set up shorts (concessions) ahead of auction supply in the expensive long-end of the curve next week. In the big picture, it seems like the Fed has already made up their mind re: QEII. From that perspective, any bond market weakness should be met with bargain buying by the time the dust settles (during or after the auctions)

Stock futures traded higher as Jobless Claims flashed...however optimism was quickly reigned in and S&Ps are back to pre-data levels...currently +0.75 at 1156.50.

The 10-year note is back below 2.40% after a brief move back over that pivot. 10s are currently bid 2/32 higher to 102-03 yielding 2.387% (-0.07bps). Volume is once again below average.

The November FNCL 4.0 is +0-06 at 103-08. That is a new record high price.....

Loan pricing should be better this morning.