- RTRS-ADP NATIONAL EMPLOYMENT REPORT SHOWS U.S. EMPLOYMENT DECREASED BY 39,000 PRIVATE SECTOR JOBS IN SEPTEMBER (CONSENSUS WAS +24,000

- RTRS-REUTERS CONSENSUS FORECAST FOR ADP PAYROLL CHANGE FOR SEPT WAS FOR INCREASE OF 24,000 JOBS

- RTRS-US ADP AUGUST PAYROLL CHANGE REVISED TO +10,000 FROM -10,000

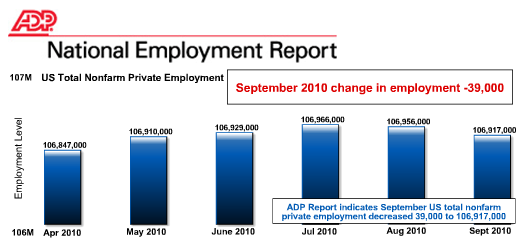

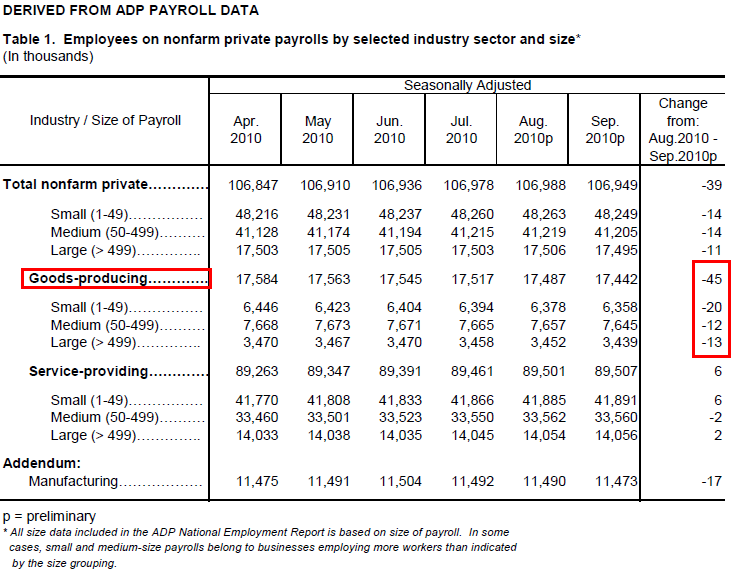

Private-sector employment decreased by 39,000 from August to September on a seasonally adjusted basis, according to the latest ADP National Employment Report® released today. The estimated change of employment from July to August was revised up from the previously reported decline of 10,000 to an increase of 10,000.

September’s ADP Report estimates employment in the service-providing sector rose by 6,000 in September, the eighth consecutive monthly gain. This increase was not enough to offset an employment decline in the goods-producing sector of 45,000. Construction employment dropped by 28,000 during September and manufacturing employment declined 17,000, the third consecutive monthly decline.

Large businesses, defined as those with 500 or more workers, saw employment decline 11,000 while employment among medium-size businesses, defined as those with between 50 and 499 workers, decreased by 14,000. Employment among small-size businesses, defined as those with fewer than 50 workers, decreased by 14,000.*

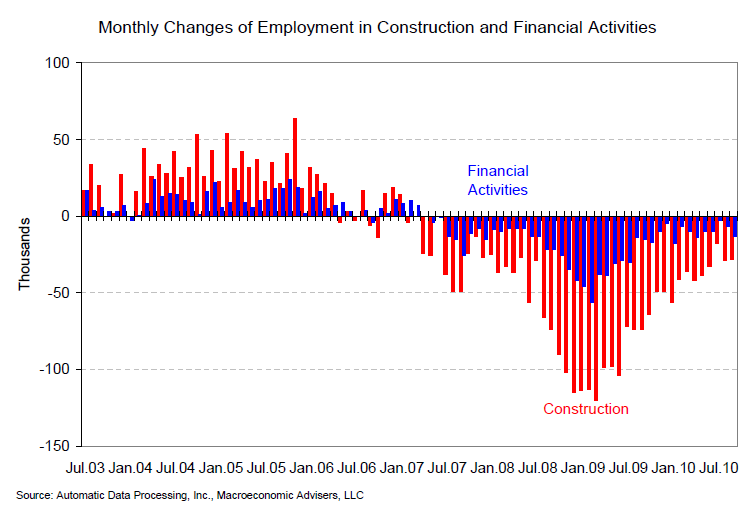

In September, construction employment dropped 28,000. Construction employment has declined for over three years and the total decline in construction jobs since the peak in January 2007 is 2,297,000. Employment in the financial services sector dropped 13,000. Financial Services employment has declined for over 3 years

Unlike the estimate of total establishment employment to be released on Friday by the Bureau of Labor Statistics (BLS), today’s ADP National Employment Report does not include the effects of federal hiring — and now firing — for the 2010 Census. Hiring for the census peaked in May and is still tapering down slightly.

ADP says: "The decline in private employment in September confirms a pause in the economic recovery already evident in other data. A deceleration of employment occurred in all the major sectors shown in The ADP Report and for all sizes of payroll. The September decline in employment followed seven monthly increases from February through August. However, over those seven months, the average monthly gain in employment was 34,000. There simply is no momentum in employment."

Plain and Simple: all the bond market heard after ADP flashed was "QEII is COMING!!!"

Market Reaction....

LIKE I SAID ...ALL THE BOND MARKET HEARD WAS "QEII IS COMING"

10s just touched 2.40%. This is our max resistance level. Now we find out just how much QEII has been baked in. The yield curve is getting crushed. 2s/10s are 5bps flatter at 202bps. The 2.625% coupon bearing 10 year TSY note is currently +17/32 at 101-27+ yielding 2.412%. Volume was weak overnight but has picked up into this rally. Just over 400k 10yr Dec. contracts traded as of 8:45am, most of those tickets were waved in after ADP. I bet flows turn toward the sellers at 2.40%, ADP is not the official employment report.

S&Ps fell 6 handles from 1160 down to 1154 and are still looking for support. Volume is EXTREMELY low. Stocks have rallied on the potential for more QE, stocks have rallied on technicals. Stocks seem like they want to rally either way. Longs have yet to be washed out and aren't being washed out after ADP. As long as 1150 support holds, we should be watching for a bounce....

Current coupon mortgages are obviously getting smashed as TSYs rally. This is on a nominal basis. I'd assume dealers are going to be lowering their asking prices after 2.5bn in origination inventory was added yesterday. This should've more than covered their short. Dealers don't need to be getting long at these levels, not withouth confirmed QEII on the table. Then 3.5s become THE production coupon instead of 4.0s. If you're floating, that is why.

The November FNCL 4.0 is currently +0-05 at 102-29. I've got the cash delivery FNCL 4.0 yielding 3.577% (6CPR). Yield spreads are as follows: +116bps/10yTSY, +106bps/10yIRS, +243bps/5yTSY.

REBATE SHOULD BE BETTER...

It's all about QEII.