After ticking sideways in a generally slow overnight trading environment, benchmark TSY yields are beginning to creep higher and "rate sheet influential" MBS prices are moving lower.

10s are at their session price lows/yield highs, currently -0-07 at 101-05 yielding 2.492%. The 2s/10s curve is 2bps steeper at 206bps wide. The 5-year note is the weakest spot on the curve (+4.1bps to 1.273%). 7s are +1.9bps at 1.863%.

I would expect to see the 10yr note pause at the target illustrated below before continuing higher. If support level is broken...be on the watch for reprices for the worse.

Rate sheet influential MBS prices are moving lower in a sluggish TBA marketplace. The November FNCL 4.0 has broken support at 102-20 and is currently -0-05 at 102-16. This is the intraday low print. Yield spreads are wider as in quiet flows. MBS are well offered by the street (FOR SALE!LOWER ASKING PRICE) after a selling spree over the past two days left dealers a little too long. Lock desks were buying back 4.0 hedges yesterday and will likely continue to reduce coverage if prices fall further. Anyone waiting to pair off?

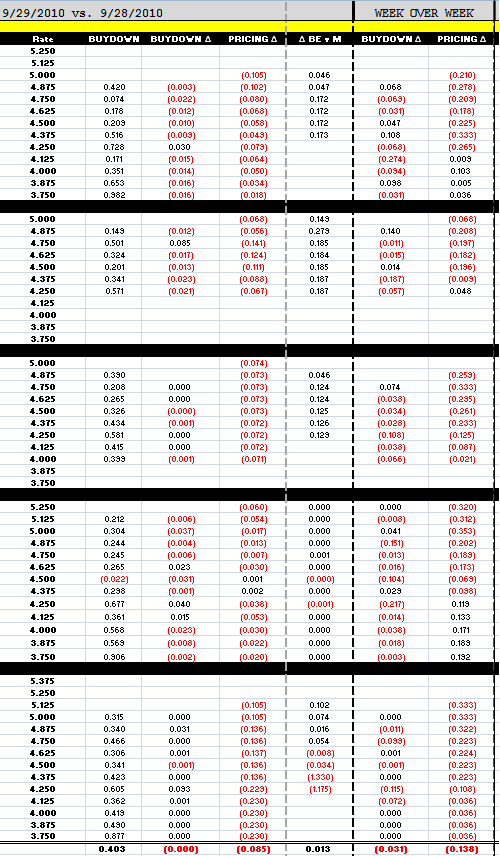

Loan pricing is 8.5bps worse today with one lender responsible the majority of rebate reductions. Buydowns are UNCH. Pricing is 13.8bps worse than it was last Wednesday, which was the best day to lock last week.

With rebate already a few bps weaker on the open, reprices for the worse don't appear to be an issue at the moment. However if 2.50% support is broken in 10s and FNCL 4.0s test the next layer of support at 102-10, then reprices for the worse would become a legit threat. Also, if you're not lucky enough to have a delegated UW in your shop and turn times have grown longer, beware of the unexpected "MY PIPELINE IF FULL AND I JUST PAIRED OFF" reprice for the worse. Capacity constraints are clearly an issue at some of the mainstream wholesalers.

FED QE UPDATE: Fed's Kochelakota sees limited price impact from QE

(Reuters) - Minneapolis Federal Reserve President Narayana Kocherlakota on Wednesday said he did not see much impact on inflationary expectations from any possible, additional monetary easing measures. Speaking in London, he also said that quantitative easing was not a tool the U.S. central bank would be contemplating if it could lower interest rates."The effects of any QE are likely to be quite muted on inflation expectations," Kocherlakota said in response to a question at a forum. Kocherlakota, who will rotate into a voting seat on the Fed's policy-setting Federal Open Market Committee next year, added that quantitative easing was not a tool that is as effective as lowering interest rates.

----------------------

Besides reaffirming that disinflation is the Fed's biggest concern, these comments add momentum to the Hilsenrath story in the WSJ yesterday: FED MULLS NEW BOND APPROACH. In the short run, the market's knee jerk reaction to this rhetoric was to sell bonds on lower odds for another round of Fed QE.

NEXT EVENT: $29 billion 7s at 1pm.