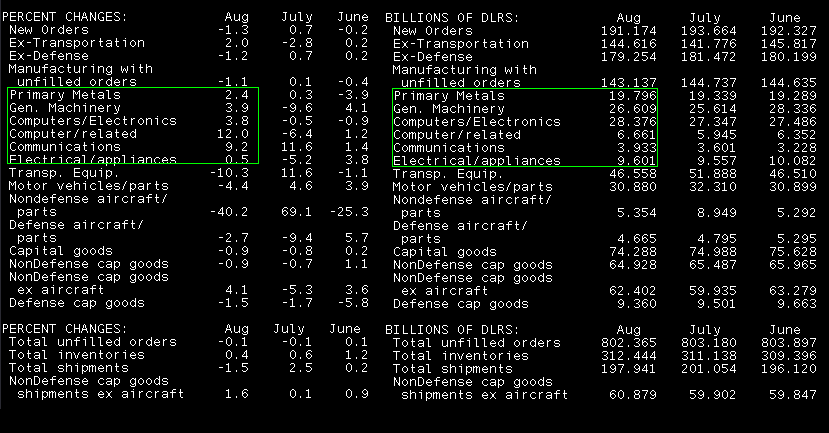

Everyone seems to be in in a tizzy because stocks are rallying on news that Durable Goods Orders fell 1.3% in August AND failed to match forecasts, which called for a 1.0% contraction. But then you strip out transportation and orders grew 2.0% in August, beating estimates for a print of +1.0%. Then you account for the 0.9% upward revision to the ex-trans number and the +0.3% revision to the overall orders index. Furthermore, when you look a little deeper into WHY the ex-transportation number beat consensus in Aug, you'll notice a few categories related to business spending improved noticeably. Computers, Communications, General Machinery....all up.

Why would bonds react so negatively to this news?

Because the Fed just had a meeting. A meeting that resulted in an FOMC statement hinting at further QE, which sparked a big 'ol bond rally.

Here is the text: the Fed is "prepared to provide additional accommodation if needed to support the economic recovery and to return inflation, over time, to levels consistent with its mandate."

KEY OBSERVATION: "IF NEEDED"

So what might the market be watching to determine when "IF NEEDED" would apply?

This verbiage was also embedded in the latest FOMC statement: "Business spending on equipment and software is rising, though less rapidly than earlier in the year".

That rhetoric sends market watchers a signal to pay attention to business spending metrics. So when business spending was reported to have improved in August, the bond market slightly lowered the odds of another round of QE being announced. Hence the sell off, led by the long end of the yield curve.

What's funny is stocks are supposed to be rallying on more QE too, but now they 're rallying on the potential for less QE? Perhaps the story behind stocks is a little more simple, they've rallied all month, it's a Friday, why not rally again. It's the path of least resistance, especially when bonds aren't catching a bid.

In the BIG PICTURE, disinflation turning into deflation is a more significant reason to believe the Fed would initiate another QE program. This rise is business spending will taken with a grain of salt until a trend develops. That means two more months of increases. Keep this on your radar. Also keep an eye on falling price levels, in both consumer level inflation data and producer level price data. The bond market will be extra sensitive to these releases. We get more manufacturing data next week, plus more than one on price levels.