Freddie Mac will again draw on its Treasury line of credit following its third quarter results. The government sponsored enterprise (GSE) released those financial statements on Thursday. To balance its books, the company will request an infusion of $6 billion under its Senior Preferred Stock Agreement. This will bring the total received since Freddie Mac was put into conservatorship in August 2008 to $72.2 billion.

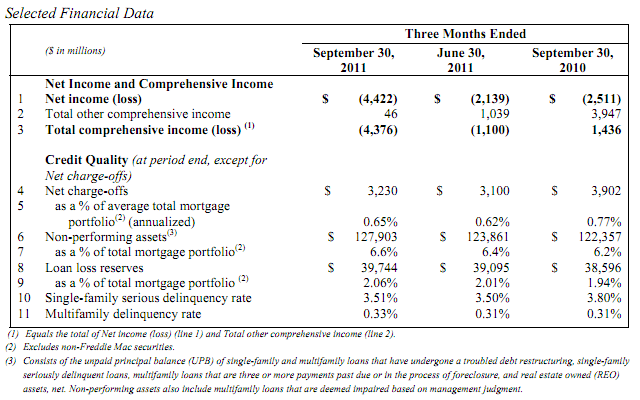

During the quarter that ended September 30, Freddie Mac posted a loss of $4.4 billion reflecting interest income of $4.6 billion offset by derivative losses of $4.8 billion and provision for credit losses of $3.6 billion. In the second quarter the loss was $2.1 billion. The difference between the loss and the draw that will be requested from Treasury is a $1.6 billion dividend that the GSE is required to pay Treasury under the terms of its stock agreement. Of the $72.2 billion that will have been drawn from Treasury following the latest request, Freddie Mac will have returned $14.9 billion in dividends.

The company said that the increased net loss for the third quarter of 2011 as compared to the second quarter reflects the impact of further declines in long-term interest rates on the fair value of derivatives. Long-term rates declined by about 125 basis points during the quarter compared to a decline of 30 basis points during the second quarter. The higher net loss also reflects an increase in the provision for credit losses for single family loans due to higher loss severity rates.

The company also reported a total comprehensive loss of $4.4 billion compared to a total comprehensive loss of $1.1 billion in the second quarter. Total comprehensive income or loss is equal to the net income or loss plus total other comprehensive income or loss which represents the change in accumulated other comprehensive income net of taxes. The higher comprehensive loss in the third quarter reflects both the higher net loss and the adverse impact of widening spreads on the value of the company's AFS securities, partially offset by the impact of declining interest rates. In the third quarter global economic uncertainty contributed to widening mortgage spreads, particularly on non-agency securities.

Net interest income of $4.6 billion was unchanged from the second quarter. Net interest yield, which represents net interest income as an annualized percentage of average interest-earning assets was 83 basis points compared to 81 basis points in the second quarter. This increase reflects lower funding costs driven by the replacement of long-term debt at lower rates.

The increase in derivative losses from $3.8 billion in the second quarter to $4.8 billion in the third reflected higher fair value losses on the net pay-fixed swap portfolio partially offset by fair value gains on the net call swaption portfolio as long-term interest rates decreased more in Q3 than in Q2.

REO operations expense was $221 million during the quarter compared to $27 million in Q2. This item primarily consists of expenses related to maintaining foreclosed property, valuation adjustment on those properties, disposition gains or losses, and recoveries from credit enhancements such as mortgage insurance. The large increase was primarily driven by higher REO holding period write-downs as REO fair values declined as well as a reduction in the projected recoveries related to primary mortgage insurance.

During the quarter Freddie Mac provided about $81 billion in liquidity to the mortgage market. The company helped to finance 312,000 conforming single-family houses, 67 percent of which were refinances, and 80,000 apartment units.

In the area of foreclosure prevention, Freddie Mac assisted approximately 48,000 borrowers compared to 54,000 in Q. 2. There were 24,000 loan modifications, 8,300 repayment plans, 4,200 forbearance agreements, and 11,750 short sales or deeds-in-lieu transactions.

The financial statement says that the company continues to experience significant credit losses and has, since 2008, recorded $70.5 in provisions for credit losses associated with single-family homes and recorded an additional $4.4 billion in losses on loans purchased from the company's PC trusts, net of recoveries. These losses are primarily associated with loans written from 2005 to 2008.

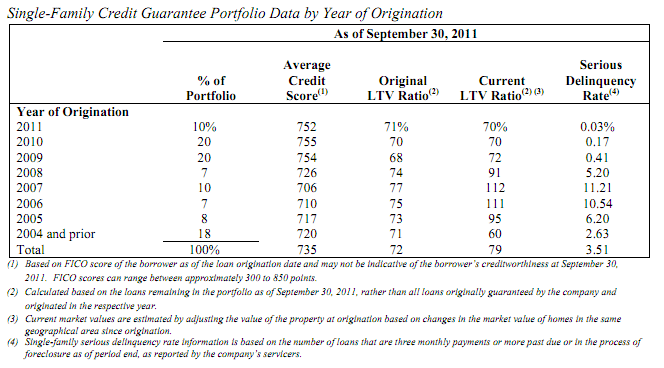

Going forward, the company believes that the credit quality of newer loans is strong, with higher credit scores and lower loan to value ratios. These loans now make up about 50 percent of the company's portfolio.

The serious delinquency rate for single family mortgages was 3.51 percent at the end of the third quarter, virtually unchanged from the end of the second quarter. By comparison, the Mortgage Bankers Association's National Delinquency Survey reports that the national rate was 7.85 percent at the end of Q2. The multi-family delinquency rate on September 30 was 0.33 percent compared to 0.31 percent on June 30.

Non-performing assets were $127.9 billion or 6.6 percent of the total mortgage portfolio on September 30 compared to $123.9 billion or 6.4 percent on June 30. These amounts included $43.2 billion and $37.2 billion of modified loans that are performing or are less than three months past due on the respective dates. The increase in non-performing assets is largely due to a change in accounting guidance.

Freddie Mac Chief Executive Officer Charles E. Haldeman, Jr. said of the results, "Our financial performance in the third quarter was impacted by the weak housing market as well as challenging financial market conditions. Freddie Mac was a stabilizing force in the mortgage market, ensuring the continuous flow of funds to lenders and borrowers and helping families avoid foreclosure. We also made further progress this year on becoming a stronger and more efficient company - adding high quality loans to our book and streamlining operations. Taken together, these efforts are maximizing the value of our assets for America's taxpayers, and reinforcing the housing finance system.

The company said it expect to request additional draws from Treasury but that the size and timing of such draws will be determined by a variety of factors such as changes in home prices, interest rates, and mortgage securities prices. For a discussion of the GSEs' possible future requirements see http://www.mortgagenewsdaily.com/10272011_gse_conservatorship.asp.