Last week RadarLogic, a real estate data and analytics company, submitted a proposal, which we covered here, to the Federal Housing Finance Agency (FHFA) in response to a Request for Information regarding the proposed bulk sale of government owned real estate (REO). Wednesday, in their RPX Monthly Housing Market Report, they provided the latest information on their RPX Composite Price, and used updated data to restate and demonstrate the need for and urgency of their plan.

In brief, the company suggested that a bulk sale would involve huge discounts that would benefit investors but exacerbate losses to the government sponsored enterprises (GSEs) and FHA and ultimately taxpayers and put negative pressure on home prices and demand that would have a domino effect on appraisals and future home prices. Instead it suggested a two prong approach; aggressively modifying distressed mortgages in the foreclosure pipeline and packaging the resulting excess debt into securities to be sold to investors willing to bet on future increases in property values. Second, it advocates the government retain existing and future REO and turn day to day management of the properties over to professional management companies as rental properties. Both approaches, the company said, would return stability to the market and thus to the economy and dramatically reduce the cost of the recovery to both government and taxpayers.

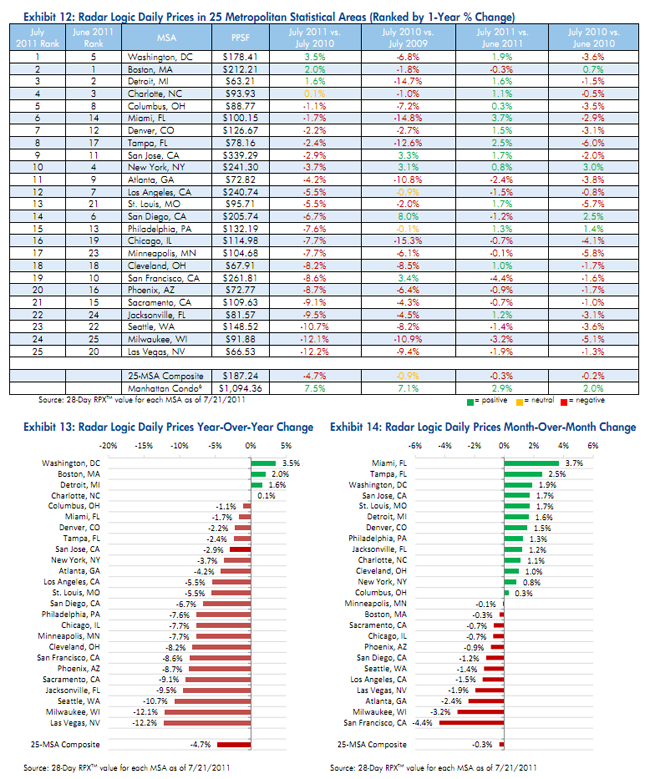

The RPX report compiles statistics from the company's composite price index for residential properties in 25 metropolitan statistical areas (25-MSA RPX). The July 25-MSA RPX price was $187.24 per square foot (psf), a drop of 0.9 percent from the June value and 4.7 percent from the value in July 2010. The company said that, with five months left in the year and the peak selling season behind us, it appears that the high price for 2011 was reached in June at 188.11, only slightly above $183.99, the lowest value observed in 2010, on December 31. In late 2007 the composite price reached $270 psf.

There is a great deal of variability in the prices across the 25 metropolitan areas. Cleveland and Detroit are both in the $65 range while San Jose, California has a psf price of $240.74. The company tracks Manhattan condos as a separate category and found that price, at $1,094.36 psf, had increased 7.5 percent since July 2010.

Only 20 percent of the MSAs in the index had year-over-year RPX price increases and the largest of these increases, in Washington, DC, was 3.5 percent. Three had decreases in double digits, Seattle (-10.7 percent), Milwaukee (-12.1 percent), and Las Vegas (-12.2 percent.) Thirteen MSA's logged month-over-month increases, the largest being 3.7 percent in Miami and 2.5 percent in Tampa. The highest monthly losses were recorded in San Francisco (-4.4 percent) and Milwaukee (-3.2 percent).

The 25-MSA RPX transaction count increased 8.1 percent year over year, but "this growth reflects subdued sales closings in July 2010 due to the expiration of the homebuyer tax credit." The transaction count increased 0.4 percent in July compared to the previous month.

While RadarLogic discounts the importance of the year-over-year transaction activity because of the anomaly of the tax credit expiration, Cleveland, Ohio did see a 98 percent increase and Jacksonville, Florida a 78.2 percent jump. Detroit's activity level fell 19.1 percent. Eleven MSAs had increases in transaction activity from June to July with St. Louis, Missouri being notable with a 27.9 percent jump. San Diego (-7.5 percent), Tampa (-7.4 percent) and San Francisco (-6.5 percent) had the largest decreases.

The report shows little optimism for the future of housing. The RPX Forward Price Fixings are established each day by dealer poll and represent the midmarket expectation of the reference value to be published on the contract expiration date. RPX is projecting little growth in this index over the next four years. From the current level in the high $180s, the fixings remain virtually level through the end of 2015, finishing the chart at just under $200. The cumulative Home Price Appreciation implied by these composite forward fixings at each years' end are:

2011 - 1.5 percent

2012 - 2.0 percent

2013 - 2.5 percent

2014 - 3.1 percent

2015 - 3.6 percent

Radar Logic said it was predicting that the next 10- and 20-City S&P/Case-Shiller composite indices will increase about one percent month-over-month but will remain about 3 percent below the July 2010 level. The 10-City index, it says, will come in at about 156 and the 20-City at roughly 143.

Returning to promoting its proposal to FHFA, the Company restates its concern that foreclosures, bank inventories, and taxpayer losses are going to continue to grow while prices suffer further declines. The total of REO properties held by all parties - GSEs, FHA, private lenders - at the end of Q2 2011 was 548,000, a number that has declined over the past few quarters as lenders slowed or stopped foreclosures in the wake of the robo-signing controversy. On September 20, a witness at a Senate Banking Committee hearing estimated that 10.4 million additional borrowers - or one in five mortgagors in the country - are likely to default on their mortgages. "This is a tidal wave headed straight toward REO inventories and ultimately the nation's housing markets," the Report says.