The economy has hit an "air pocket" according to Fannie Mae's latest economic projections. If your plane has ever hit one you're familiar with the feeling; weightlessness, stomach not quite where you left it. You know or at least hope the plane will stop dropping, you are just not sure when...

Fannie Mae's April Economics and Mortgage Market Analysis attributes the current state of temporary weightlessness to a pair of major shocks - the political turmoil which continues in the Middle East and North Africa and the earthquake and resulting nuclear catastrophe in Japan coupled with what it calls multiple cross-currents in both the U.S and Europe. These include budget problems on all levels of government and related cut-backs in spending, concern over federal monetary policy and "rising headline inflation" driven by increasing food and energy prices.

Meanwhile, there appears to be a slowdown in economic activity in the first quarter of the year with consumer spending growth poised to come in well short of the high-water mark set in the fourth quarter of 2010. Business investment and nonresidential investment in structures also slowed and housing is showing renewed softness. Just as the picture begins to seem bleak, Fannie Mae's economists post some good news - more new jobs created in March, an unemployment rate that dropped to its lowest level in two years, and the best quarter for the Dow Jones Industrial Average in 12 years. Despite the overall gloom in the report, Fannie Mae says the contraction in growth is expected to be temporary with a modest acceleration projected for the second half of the year. The group predicts economic growth to average 3.1 percent for 2011, a downgrade from 3.5 percent projected in the March forecast. The key to this outlook is continued improvement in the labor market and moderating oil prices in the second half of the year. Fannie does however exhibit nervous sentiments on the potential for further downgrades, saying "significant challenges lie ahead, which could potentially lower growth this year by much more than we project."

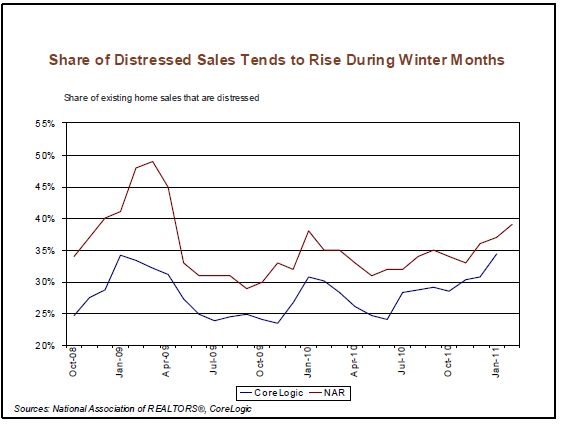

The report calls housing the "Achilles Heel of the Expansion." Activity weakened across the board in February. Existing home sales fell 10 percent, perhaps partially due to earlier weather conditions and distressed sales continue to account for more than a third of total housing sales. The distressed sales are a particular hurdle for the new home market which set a new record low in February and is now 9 percent below the old record set last August. The lack of sales activity has resulted in sharp drops in housing starts which are now only about four percent above the record lows in January 2009 and the second consecutive monthly drop in the issuance of single-family permits suggest continued sluggish homebuilding activity near term.

Distressed sales and a winding down of programs to support the housing market have affected home prices which have shown persistent declines. The FHFA purchase-only price index fell in January for the seventh time in eight months while the CoreLogic and Case-Shiller indices show year-over-year home price appreciation during the first half of 2010 and then renewed declines following expiration of the homebuyer tax credits. Market expectations for home prices have deteriorated over the past several months according to multiple surveys of consumers.

Some of the shifts in housing projections since the March report are disquieting. Median prices of existing homes which were projected to float in the $211,000 to $223,000 range through the end of 2012 have been downgraded to a range of $160,300 to $167,500 in the first three quarters of 2011, falling again at the end of this year and beginning of next before recovering to around $167,000 by Q4 2012. Housing starts have been downgraded to 478,000 for the year compared to 508,000 in the March report and total housing sales projections were modified slightly from 5.56 million 5.53 million. Mortgage originations are still projected to total $1.038 billion with 40 percent coming from refinances and the estimate for the 30-year interest rate remains at 5.4 percent at year-end.

Some other details from the forecast....

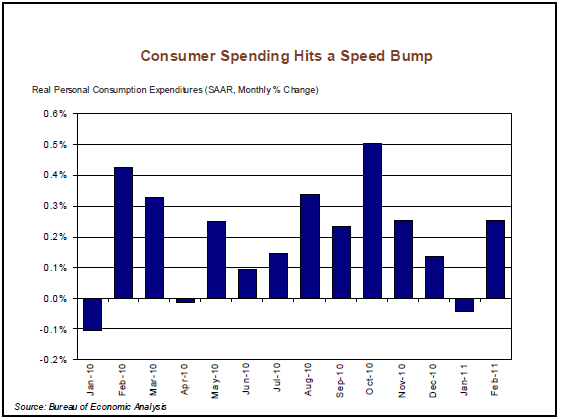

In January real (inflation adjusted) consumer spending declined for the first time in nine months, January growth was approximately -.03 percent compared to over 1 percent in December. It rebounded to December levels in February but the near-term outlook appears, the report says, subdued "as confidence has recently turned sour."

The rapid rise in gasoline prices - up by 80 percent on an annualized basis in the three months ending in February (and substantially higher since) has taken a toll on consumer confidence. The March Conference Board consumer confidence index fell to 63.4 percent from the recovery high point of 72.0 it reached in February and the consumer sentiment index from Reuters/University of Michigan fell ten points during the month. Fannie Mae economists expect that the growth in consumer spending during the first quarter will be below 2 percent compared to over 4 percent in Q4 2010.

Unemployment was down to 8.8 percent in March, the fourth consecutive monthly drop and the rate for the quarter decreased 0.7 percent to 8.9 percent, the steepest quarterly drop since 1984. The vast improvement in the unemployment rate in December and January was due to a huge drop in the labor force (nearly 800,000 during the two month period). The forecast projects an unemployment rate of 8.4 percent by year-end. Initial unemployment claims have also declined with the four-week moving average remaining below 400,000 for six straight weeks. In a survey by Business Roundtable 52 percent of CEOs said they intend to add to payrolls, up from 45 percent in the fourth quarter.

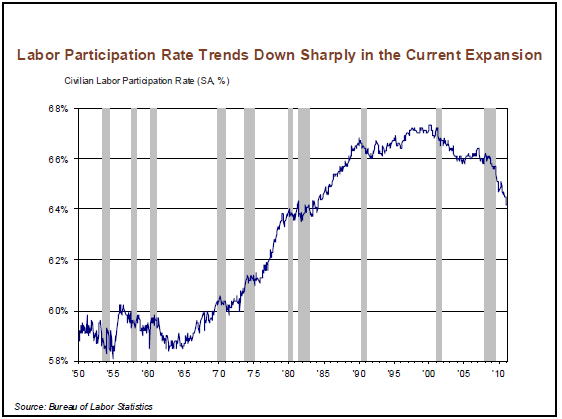

The labor participation rate, which had been falling almost continuously since April of last year, has shown signs of stabilization though. The rate remained unchanged in March for the second consecutive month at an historically low level of 64.2 percent, half a percentage point below that of six months ago. A declining participation rate is historically quite unusual during economic expansions with the notable exception of the jobless recovery following the 2001 recession.However, the dip in the rate in February and March indicated a genuine improvement as gains in household employment substantially outweighed the increase in the labor force.

The average workweek for all employees on private payrolls was unchanged at 34.3 hours in March. In addition, the average hourly earnings of all employees also were unchanged for the fourth time during the last five months. During the past year, wages have risen just 1.7 percent, which will provide little help for consumers to combat higher gasoline prices. However, soft wage trends appear to give the Fed some comfort, in that underlying inflation will likely be benign in the face of rising energy and commodity prices.

READ MORE...

Inflation Update: Cost of Living Rising as Wage Growth Lags

Inflation Expectations Distorted by Bullish Perspectives of Reality