Mortgage lenders reflected a lot of optimism about their business prospects in the third quarter Mortgage Lender Sentiment Survey conducted by Fannie Mae. This is in sync with a report late last month from the Mortgage Bankers Association which reported greatly increased profitability on the part of mortgage banks in the second quarter. Now lenders have told Fannie Mae they expect this trend to continue.

The net profit margin outlook found by the survey was at an all-time high, surpassing the previous high in the first quarter of 2015, primarily due to strong mortgage demand expectations, especially for refinancing.

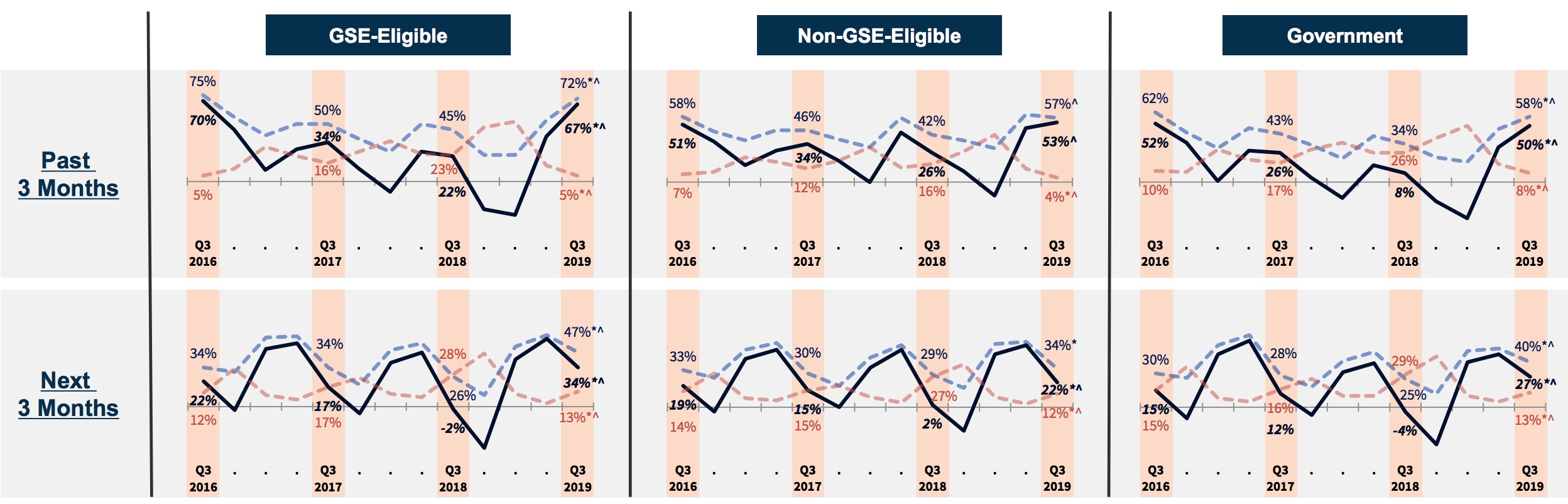

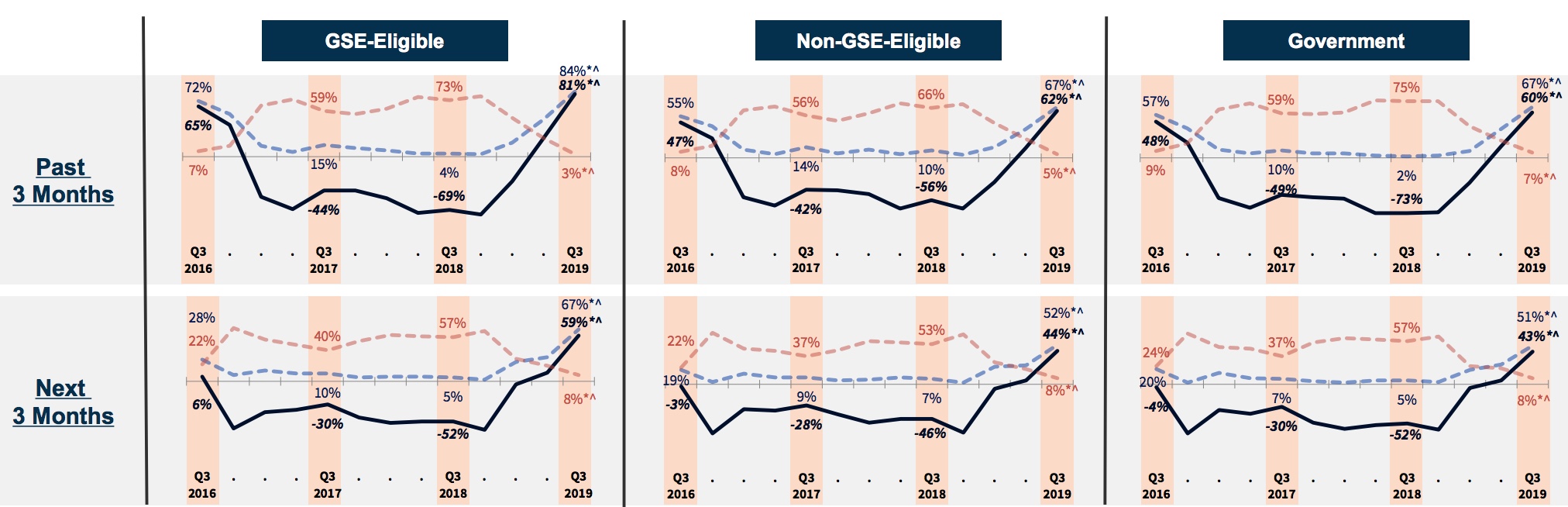

The net share of lenders reporting an increase in demand over the previous three months reached the highest level for any third quarter since 2016 across all loan types, GSE-Eligible, Non-GSE-Eligible, and Government. The net share of those expecting that demand will continue to rise over the next three months was the highest for any third quarter since Fannie's survey was initiated in 2014. Virtually the same pattern was in play for refinancing demand reports and expectations.

Purchase Demand

Refinance Demand

Fannie Mae provides support for the refinancing demand assumptions. The company estimates that approximately 40 percent of outstanding mortgages, or about $4.1 trillion of unpaid principal balance, would likely benefit from refinancing.

With the perception of greater demand comes expectations for higher profit margins. Fifty-three percent of respondents expect those margins to increase over the next three months, up from 41 percent in the second quarter survey. Thirteen percent expect margins to decline, about the same as the previous quarter but down from 41 percent a year earlier.

The report says the recent widening of the primary/secondary mortgage spread appears to confirm mortgage lenders' reported profitability. Mortgage rates typically do not fully absorb a contemporaneous decline in Treasury rates, due in part to temporary capacity constraints and increased hedging costs for lenders. A wider spread contributes to lender revenues and profits.

Consumer demand (at 61 percent) and operational efficiency (43 percent) were the reasons cited most often for the profit margin optimism. Among those anticipating a decline in profits, most (66 percent) blamed competition from other lenders, the 11th consecutive quarter that has led responses. However, GSE pricing and policies jumped into second place at 28 percent, its highest level of response since the second quarter of 2014.

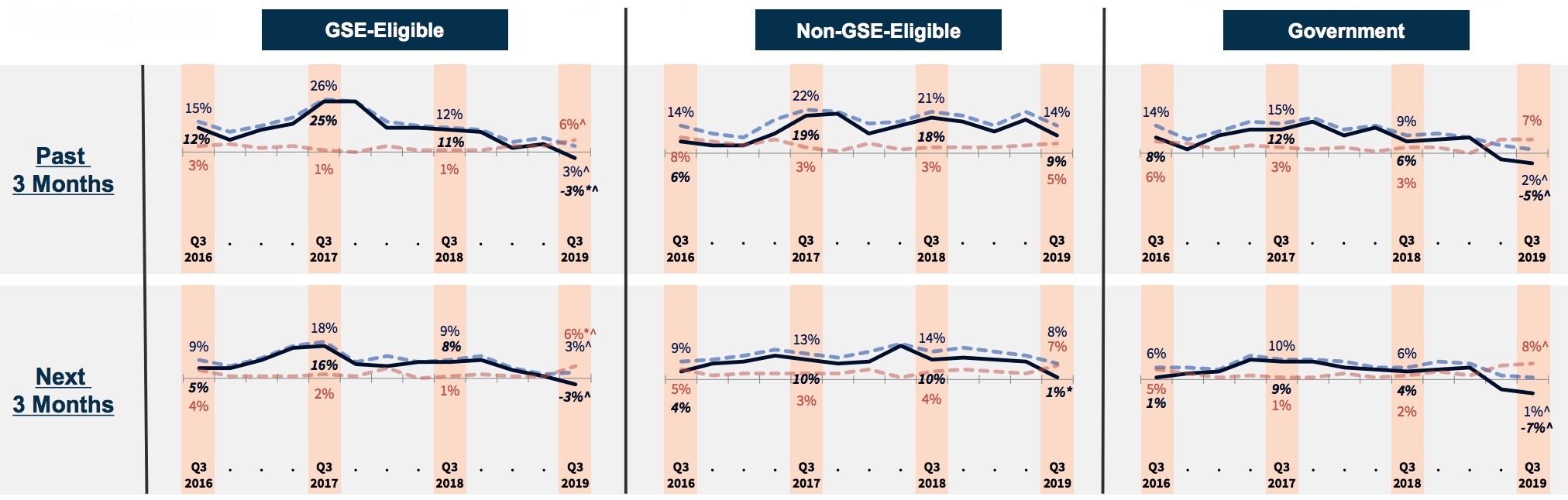

The net share of lenders reporting that credit standards for GSE-Eligible loans had eased over the prior three months was negative for the first time since the fourth quarter of 2014 and lenders generally reported less easing previously and less expected over the next quarter.

Credit Standards

"Lender profitability sentiment hit a survey high this quarter, despite the movement of credit standards from net easing to net tightening," said Fannie Mae Senior Vice President and Chief Economist Doug Duncan. "Lenders attributed their upbeat profitability outlook to consumer demand and operational efficiency. Many lenders pointed to declining interest rates as the engine behind consumer demand, particularly for refinance mortgages. Together, the results suggest that lenders' positive profitability outlook is being driven primarily by business fundamentals, not by lowered credit standards."

The Lender Sentiment Survey features responses from 199 senior lending executives from 179 institutions. There were 72 mortgage banks, 70 depository institutions and 33 credit unions represented in the report. Sixty were among the top 15 percent of institutions in loan volume, 45 were considered mid-sized, and 74 percent were in the bottom 65 percent for mortgage volume.