While calling the recent report on real gross domestic product (GDP) the strongest first quarter in four years, Fannie Mae's Economic and Strategic Research (ESR) group agreed with Freddie Mac's economist that the 3.2 percent reported growth is unsustainable. Report details showed deceleration in both household and business spending growth compared to the fourth quarter. Half of the headline growth was due to increases in net exports and business inventories they said, and the growth in upcoming quarters should be closer to the previous trend of 1.8 percent as fiscal policy impacts fade, with government spending no longer boosting growth in the second half of the year. Despite the first quarter results they expect growth for the year to be only one-tenth point higher than earlier projections at 2.3 percent.

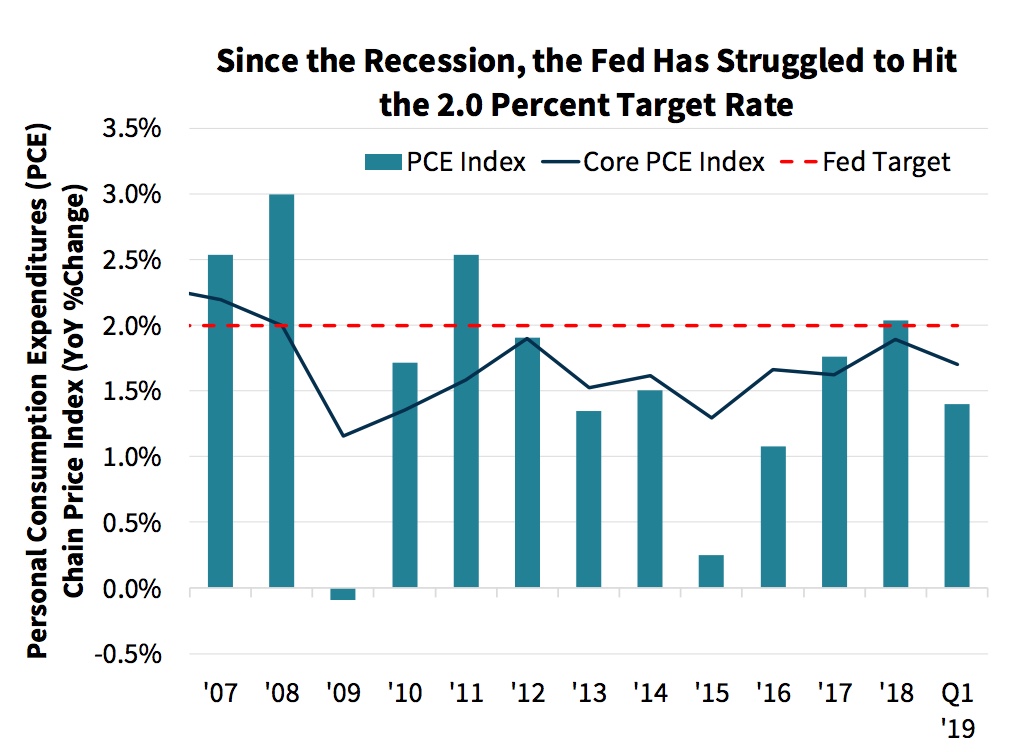

Inflation pressures are still below where the Federal Reserve has set its target. The PCE deflator, its preferred measure of inflation, accelerated in March for the first time in eight months but it still down a half-point from the 2.0 percent goal. During the first quarter the headline inflation rate averaged 1.4 percent, the slowest pace in more than two years.

In its statement following the May Federal Open Market Committee (FOMC) meeting the Fed acknowledged that both measures have declined and attributed it to "transitory factors." However, the ESR group says inflation below 2.0 percent has been less of an exception than normally in the current expansion and this will make it difficult for the Fed to raise its fed funds rate any further this year. Coupled with the fading hope for a U.S.-China trade deal, Fannie Mae has dropped its prediction of a December rate change and sees no more increases within its forecast horizon.

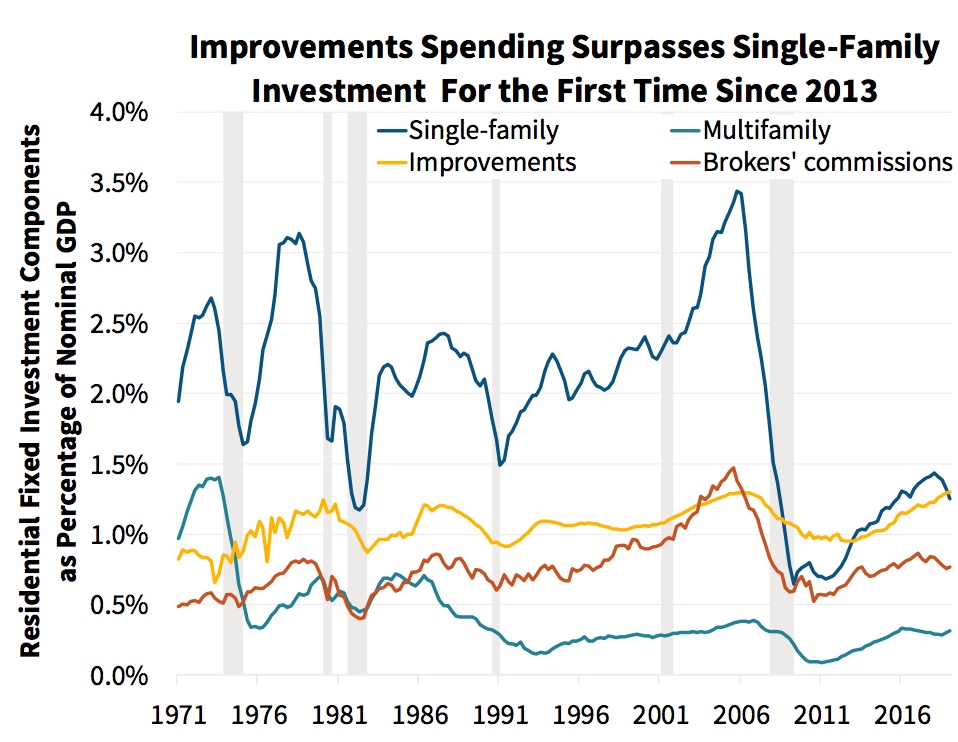

Residential investment was a drag on growth for the fifth straight quarter, driven by a decline in spending on new single-family structures. Single-family starts did increase, but a decline in the average home size pulled spending down. Spending on improvements rose and exceeded investment in single-family structures for the first time since 2013.

Brokers' commissions, a part of residential investment, rose in the first quarter, thanks to a jump in new home sales and the first rise in existing home sales in five quarters. New single-family sales rose almost 15 percent over the quarter and were up slightly on an annual basis supported by drawing down inventories that had built up as interest rates mounted and sales slowed in 2018. Rates have now pulled back from their November average of 4.87 percent, falling about 70 basis points to 4.14 percent in April. The full effect of declining mortgage rates is likely still working its way through the market, adding further support for buyers. Builders likely still have a few months to go before inventories are back to their pre-slowdown trend, which should support new home sales in the second quarter, even if starts continue to be lackluster.

Builders seem to be focusing increasingly on more modest-sized homes which is good for entry-level buyers. After peaking at more than 2,500 square feet in the first quarter of 2015, the median size has trended down by about 200 square feet and the median price of a new home sold fell 7.1 percent. Price gains are also moderating for existing homes with the CoreLogic National House Price Index rising only 3.7 percent in March, the smallest gain since May 2012.

The ESR group says leading indicators are pointing to a solid spring homebuying season. Pending sales jumped 3.8 percent in March which would suggest continued strength in April home sale closing. Purchase mortgage applications also rose strongly in March and April. Fannie Mae has raised its home sales forecast for the second quarter accordingly to indicate a solid rebound from the first quarter. "When combined with our more optimistic view of new home sales for the year, total sales for 2019 were also revised upward seven-tenths from our prior forecast (0.0 percent) to a modest gain of 1.0 percent from 2018."

Incoming applications data also drove a revision to both purchase and refinance mortgage origination forecasts for 2019, pushing expected total volume from $1.62 trillion to $1.66 trillion. Purchase originations are expected to rise given the modest increases in home sales and continued but slowing, home price growth. With mortgage rates beginning to stabilize at much lower levels than in 2018, there should be less of a decline in refinance volumes so that forecast for the year has been revised from a 2.2 percent annual decline to a 1.2 percent decline.