They aren't suggesting you shop 'til you drop, but Freddie Mac says neither should borrowers buy the first mortgage they see.

Doug McManus and Elias Yannopoulos, members of the company's Economic and Housing Research Group, write in its Insights Blog that shopping for a better mortgage rate could save a borrower hundreds or thousands of dollars. Yet, a 2015 survey by the Consumer Financial Protection Bureau found that almost half of consumers "seriously considered" only one lender before making a choice. More than three-quarters (77 percent) made application with only one lender and very few considered more than three. The Freddie Mac analysts say many borrowers don't even realize that rates offered by lending institutions can vary widely.

Their research indicates that just getting one additional quote saves borrowers an average of $1,500 over the life of the loan and five quotes saves an average of $3,000. So why do consumers leave this money on the table? McManus and Yannopoulos say the answer to that question is so complex it just won Richard Thaler the Nobel Prize in economics.

Thaler's research into seemingly irrational economic behaviors didn't focus on mortgages of course, but he found that consumers in general shop too little, get confused while evaluating alternatives, and are slow to switch from past choices even if failing to do so is costly. Such behaviors don't necessarily complicate getting a good deal on a pair of shoes but do apply to complex tasks like getting a mortgage and can lead to consumers relying solely on an existing banking relationship or a referral from someone they trust.

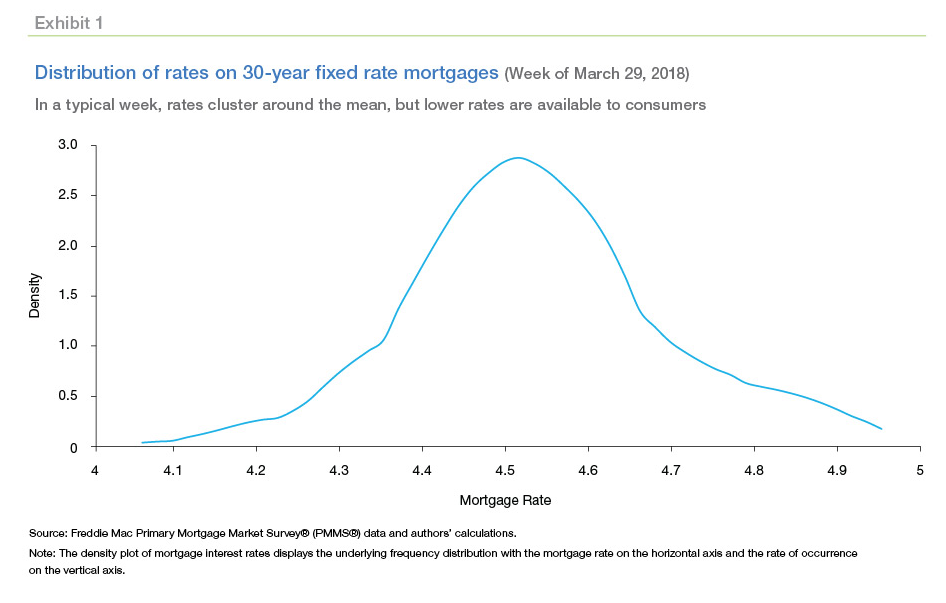

And getting a good rate can be complex. Freddie Mac tracks variations in rates and points each week from about 125 lenders across the county in its Primary Mortgage Market Survey (PMMS). These lenders include a mix, thrifts, credit unions, commercial banks, mortgage banks, that roughly match the level of the mortgage business that each type commands nationwide. The survey's results for the week of March 29 show how wide the dispersion of rates might be. While the majority of lenders were quoting around 4.5 percent, the range was 4.2 to 4.8 percent.

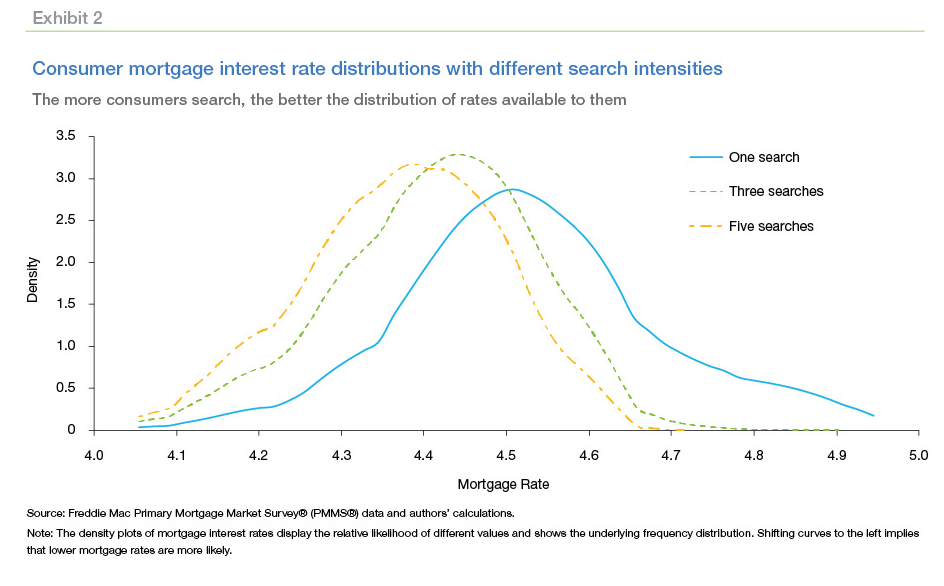

The authors mimicked rate shopping by randomly drawing mortgage rates from the March 29 distribution. One draw provides the borrower with a rate that could be high, low, or most likely near 4.5 percent. It's called "luck of the draw." But what if borrowers draw more than once? A second draw might pull in a lower or higher rate to choose from. With five draws they have three more chances to better the situation. In practice, this shopping can be as simple as doing an internet search, visiting a local bank, or picking up the phone.

The distribution of rates on March 29 was not atypical. Freddie Mac extended this experiment over the past two decades (1995 to 2017) and found consumers getting five rate offers saved an average of 16.6 basis points (bps) or 0.166 percent. Savings ranged from 12 bps to 22.3 bps. While these might sound like modest reductions in the mortgage rate, the present value of the change in mortgage payments add up to a substantial sum.

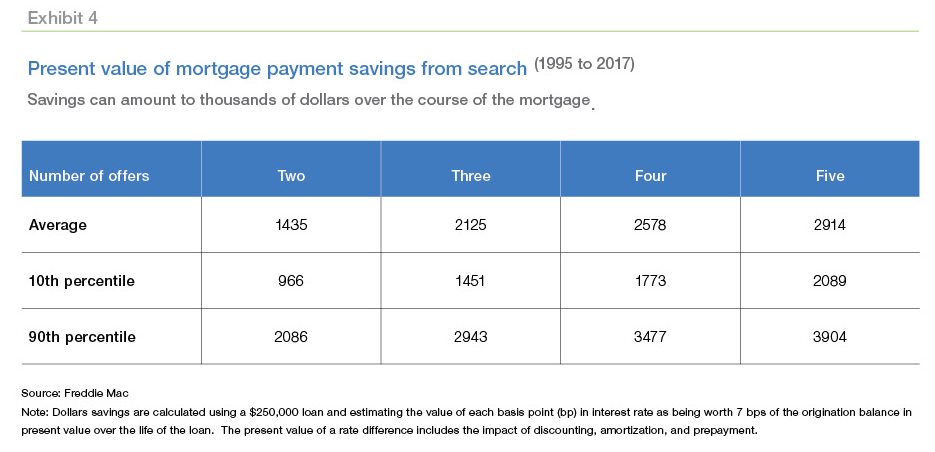

For example, the average expected savings from only one additional quote on a $250,000 loan is $1,435. But that's just the average. Borrowers who were quoted a higher rate in their first search will save more. Exhibit 4 displays the present value of the rate reductions from additional searching. Savings are computed based on each week's survey for the average savings, and both the bottom ten percent and the top ten percent of savings for each week and then averaged across all weeks. Eighty percent of borrowers who obtain one additional rate offer will save between $966 and $2,086. The average expected benefit increases to $2,914 if the borrower receives five rate quotes. Eighty percent of borrowers who obtain five offers will save between $2,089 and $3,904.

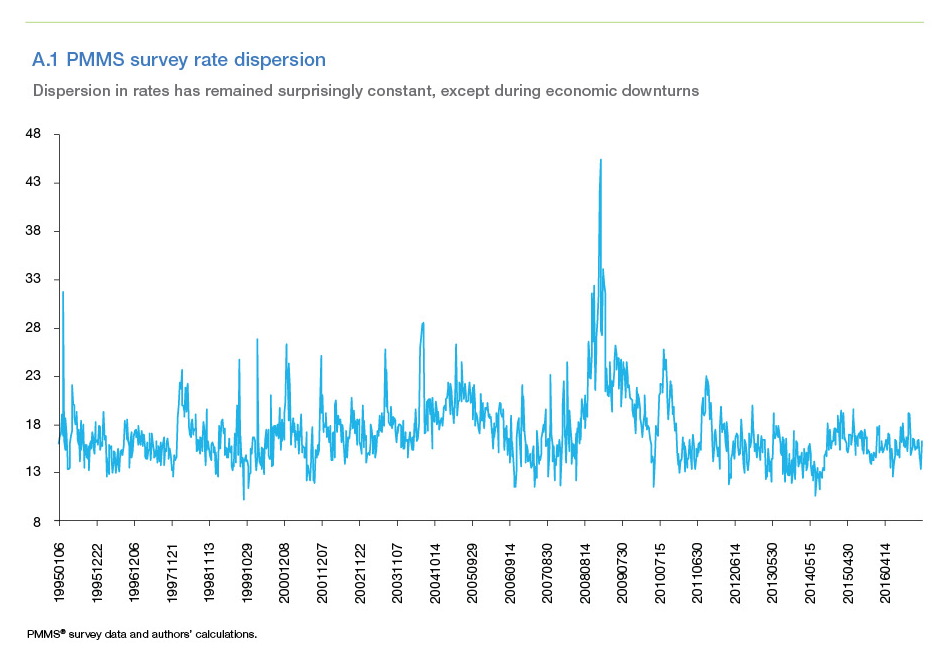

Of course, a household's actual savings depend on other factors too; the loan size, the length of time the borrower has the loan, and the dispersion of rate quotes. Freddie Mac says this dispersion has remained surprisingly constant but tends to be higher in periods of economic stress. Looking at the PMMS survey data from 1995 through 2017, the standard deviation of offers ranged from 15 to 25 bps. However, during the global financial crisis, the rate dispersion peaked at about 45 bps. Borrowers getting a $250,000 mortgage during the week of December 11, 2008, in the depths of that crisis could have saved an average of $5,020 by getting five rate offers.

The price of a mortgage doesn't consist of the rate alone and consumers also need to shop for fees. The authors quote a 2012 paper by Susan Woodward and Robert Hall published in The American Economic Review which said that, by not shopping effectively, a typical borrower paid an extra $1,000 in broker fees to originate their mortgage.

Of course, there are no guarantees of savings. A borrower could get lucky with his or her first rate offer, and the Freddie Mac analysis assumes a wide range of possible rates, something that might not exist in some markets.

Still, McManus and Yannopoulos say the research is clear: Borrowers should compare offers from several lenders. Those comparison should include interest rates, terms, and fees (including lender application, processing fees, and other loan origination fees). And it also pays to ask questions if you don't understand the loan program features.

"By shopping more than one mortgage lender-ideally, three or more-the consumer is much more likely to get a better interest rate and save money in both the short and long term," the authors say. "With lower monthly payments and lower fixed fees, the loan will be more affordable, and thus safer, and consumers will have hundreds or thousands of dollars more in their pockets. Not a bad return for a few phone calls or clicks on the internet."