Can the past be reliably expected to predict the future? Probably not if one is talking about consumer behavior and structural breaks in the housing cycle.

That, at least, is the opinion of Wells Fargo Economists John E. Silvia, Azhar Iqbal, and Abigail Kinnaman in a two-part series in the company's Consumer and Retail Commentary newsletter. They say that, since private consumption is such an important driver of GDP, it is key for policy and decision makers to understand the behavior of consumers and their household balance sheets as they attempt to forecast consumer trends. Prior trends and historical averages should not be used for this purpose.

Their analysis shows that household assets and liabilities are non-stationary and non-means reverting, that is their averages do not stay the same over time nor can they be expected to return to them. For example, corporate equities are quite volatile and tend to reflect underlying economic fundamentals. They made up close to 30 percent of household assets at the peak of the dot-com bubble, only to plunge to 15 percent when the bubble burst. Their recovery did not carry them close to their previous level before they crashed again with the recession. Household investment in other assets, mutual funds, credit market instruments, demonstrate the same types of fluctuations, although the variances are much shallower.

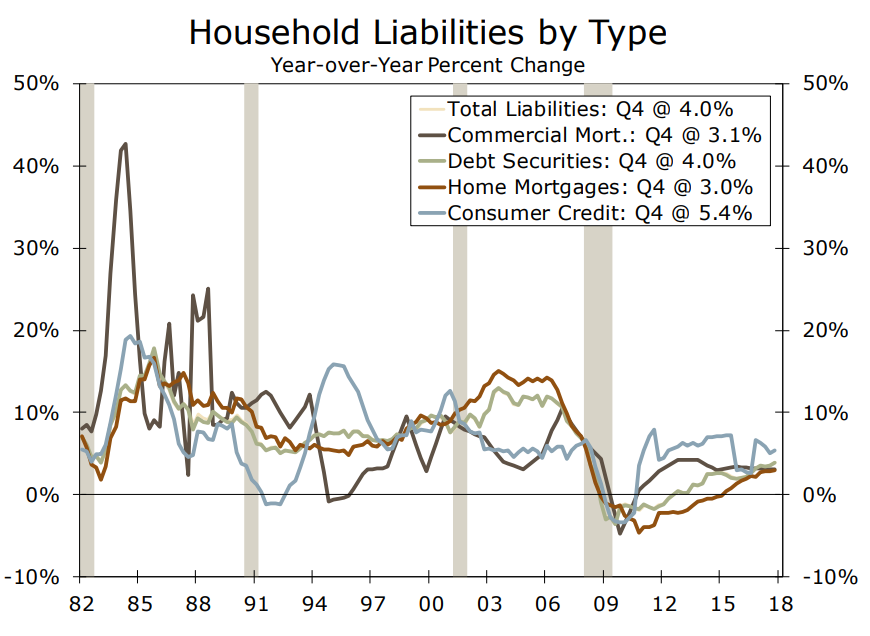

The growth rate of various household liabilities also evolves over time. Household were highly leveraged in terms of housing debt in some cycles, but the economists say that does not mean they will continue to put their money into that sector now or in the future. Home mortgage liabilities increased only 3 percent year over year, far less than the 5.4 percent growth of consumer credit debt, in the fourth quarter of 2017. The authors point to the apparent caution of households in taking on mortgage debt that has led to a relatively subdued housing recovery.

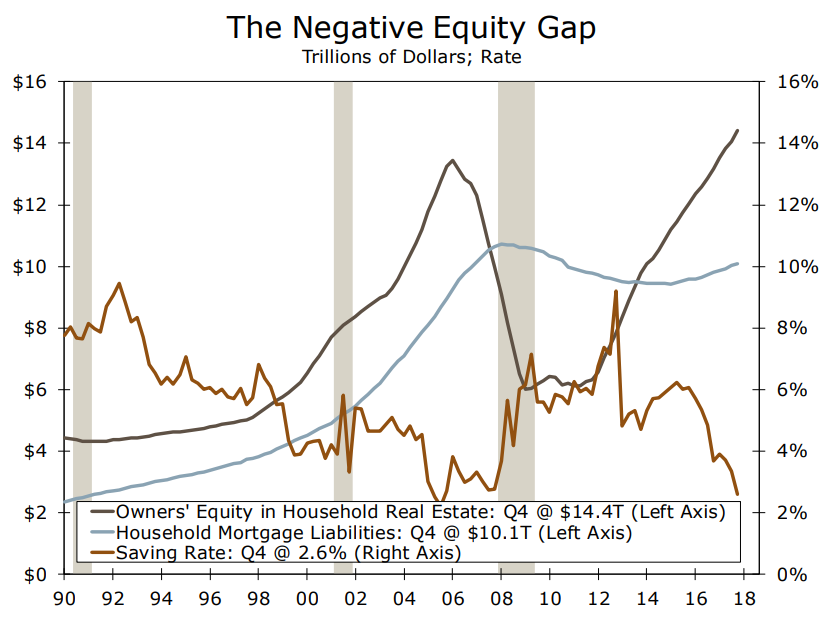

The assets to liability ratio is also non-stationary, indicating that the makeup of assets and liabilities and how households accumulate wealth over time will also change over different time periods, reflecting the ongoing evolution of the economy and of financial market regulations. For example, stricter financial regulations and consumer caution help explain lower mortgage debt in the current cycle while the rising stock market has boosted household wealth. On net, the upswing in the assets-to-liabilities ratio, currently at 7.1, reflects the evolution of economic fundamentals.

In the second part of the analysis the authors point out that to call the housing market cyclical is a cliché but not completely accurate. Both the asset side, that is owner's equity, and the liability side, mortgages, demonstrate both volatility and structural breaks, an abrupt change in a time series either because of a change in the mean or other parameters that produce the series. This leads them to conclude that both sides are non-mean reverting which diminishes the prospect of finding a reliable forecasting method for either one. "Moreover, the structural breaks in both series intimate that changes in housing finances are abrupt and are likely to be unanticipated. While the conditions for housing corrections may exist, the precise timing to reliably forecast such a correction remains elusive."

Decision markets should note that the non-stationary nature of assets and liability means it is difficult to find a cause for their behavior. The authors say, "We do not know which series leads the other in creating a trend, and it would be misleading to attempt to argue one way or the other." For example, the Debt Service Ratio (DSR) (analogous to DTI) declined 34 percent from its peak in the fourth quarter of 2007 until it bottomed out in the same quarter of 2012, but has risen only 4 percent since then. Both the DSR ratio and the related Financial Obligations Ratio are characterized by structural breaks. "This reaffirms our view that prior trends are not necessarily telling of future trends," they say.

This presents a problem for credit, especially longer-term obligations such as auto and mortgage loans. For example, auto loans may extend for five to seven years so credit decisions made during an economic expansion such as 2004 to 2006 can be followed by a rapid rise in the DSR and growing pressure on consumer finances. Household delinquencies are sure to follow.

Emotional mindsets such as blind faith in rising home prices or consumer confidence or lack of it can drive or hamper economic growth, is a characteristic of households as well as investors and entrepreneurs. As the economic cycle improves and employment and income increase, so does household net worth. Households then tend to reduce savings and increase consumption.

But emotional reactions can operate in the other direction; when households become less optimistic they can pull back spending. The net worth and spending time series are also characterized by structural breaks so once again historical trends should not be used to predict the future.