It was nice while it lasted, but the long run of historically low mortgage rates is clearly coming to an end. This month Freddie Mac's Outlook looks back at where rates have been, where they are going, and what the effect might be on home buyers, homeowners, lenders, builders, and real estate agents. The authors, Doug McManus, Freddie Mac Quantitative Analytics Director and Elias Yannopoulos, Quantitative Analytics Senior, also look at what may drive rates going forward and present some scenarios for the future.

Rock bottom interest rates weren't always the norm. Older Baby Boomers were buying their first homes in a very different environment. In 1981 rates topped 18 percent, having soared there from 8 percent over a four-year period. Freddie Mac says that was the most dramatic increase in the near 50 years Freddie Mac has tracked rates.

Those rates hit real estate markets hard.

- New mortgage originations fell nearly 40 percent, from $162 billion in 1977 to $98 billion in 1981.

- Annual single-family home sales dropped 36 percent, from 4.5 million to 2.9 million.

- The biggest decline was in construction, with housing starts for single-family homes plummeting over 51 percent, from almost 1.5 million to 705,000 by 1981.

"In frustration, thousands of home builders mailed wooden 2x4s to the Chairman of the Federal Reserve at the time, Paul Volcker, pleading with him to lower rates," Freddie Mac recounts.

Since the highs of 1981, mortgage rates have mostly trended downward, however according to Freddie Mac's own records, they remained in double digits until October 1986. They could soar again, but the company says, "more recent experiences suggest that the current expected increases in mortgage rates should be more modest and have relatively benign effects on housing and mortgage markets."

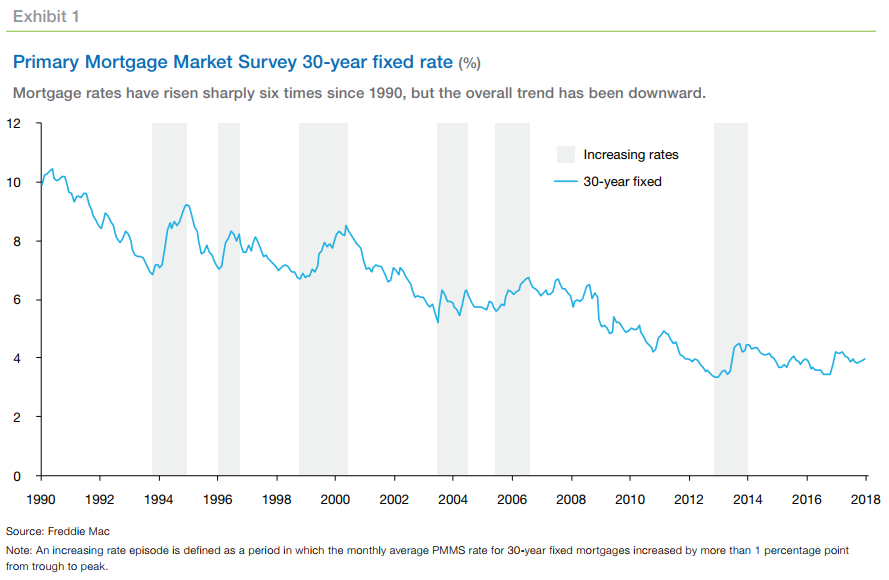

Looking back, however, can inform expectations about how rising rates will impact various populations. Freddie Mac defines a rising rate environment as a period in which the monthly average of its own Primary Mortgage Market Survey (PMMS) rate for 30-year fixed mortgages (FRM) move more than 1 percentage point from trough to peak. There have been six such periods (the shaded areas in the following exhibits) since 1990, none of which came close to matching the rate increase of the late 1970s. The closest competition was the period from October 1993 to January 1995 when the rate jumped 2.4 percentage points.

The six periods identified by the authors were almost always accompanied by reductions in mortgage originations, home sales, and housing starts. For example, in the 14 month period in 1993-1995 referenced above, mortgage originations fell by 49 percent, home sales 11 percent, and housing starts 13 percent. The second biggest increase, 1.81 percentage point over a 19 month period in 1998-2000, saw originations fall 46 percent, sales 2 percent, and starts 12 percent. Over the six periods the average rate increase was 1.46 percent, origination declines averaged 30 percents, sales fell 5 percent, and housing starts 11 percent.

Interestingly, home prices did not fall in any of the six periods, increases in fact averaged 8 percent. There were also two periods when only one or two of the three other measures declined. In 1996 originations continued to grow, in 2003 only originations were down while sales and starts posted slight gains.

Borrowers are the group most directly affected by rising rates. Their buying decisions - whether to buy, when to do it, which home to purchase, how much to borrow - are all heavily influenced by mortgage rates. As rates increase (assuming the same downpayment) so do monthly payments and the higher they go, the greater the chance that potential first-time buyers will be priced out of the market, either because they cannot stretch their budget far enough or because their debt to income ratio gets out of control. Some households can compensate by purchasing a lower priced home, others may choose to rent instead.

The mix is even worse for existing homeowners. Those looking to refinance are especially sensitive. They usually seek to reduce the monthly payment, and, in a rising rate environment, few will find that possible. When purchasing, the link with rates is also strong because equity in the existing home is typically the source of a downpayment for the next one. Once the costs for a new mortgage rise above what the borrower is paying on the existing home, the tendency is to delay the sale and new purchase. However, families who must move, perhaps to relocate for a new job or to accommodate a growing family, will accept a marginal increase in financing costs to do so.

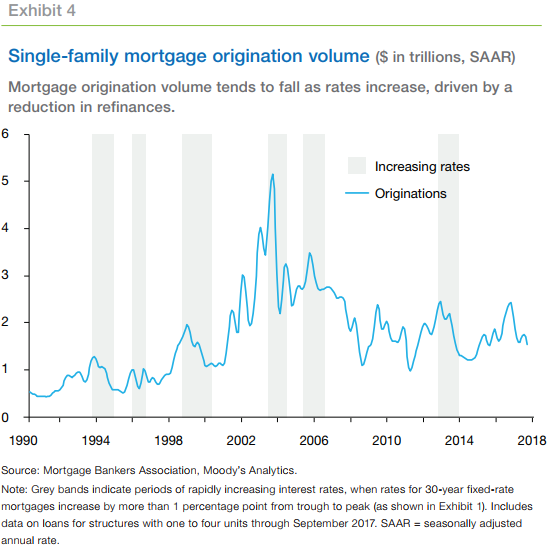

The next group affected are mortgage lenders. They thrive on volume, but as rates rise, demand for mortgages, especially for refinancing, falls. Exhibit Four shows that, when rates increased, mortgage originations typically declined by over 40 percent. This is another reflection of the lack of motivation for fixed-rate borrowers to refinance when rates rise. What remains is cash-out activity and refinances to rid borrowers of FHA insurance once homeowners achieve sufficient equity.

While originations begin to decline as rates rise, negative changes in real estate sales are typically delayed a few months, and decisions to buy or sell a home are only modestly affected to the downside by rising rates. As noted, some households must move, thus sustaining the purchase volume. Depending on the specific conditions of the housing market, the downside to real estate agents of lower volume can be offset by an increase in house prices.

The link between buying and selling decisions means a drop in the demand for homes is usually accompanied by a drop in the supply of homes. The coordinated moves of supply and demand have offsetting effects on price-lower demand decreases price and lower supply increases price. Exhibit 6 shows the Freddie Mac National House Price Index from 1990 to June 2017 as being unresponsive to movements in interest rates.

In the current market, price increases are driven by low supplies of both new and existing homes coupled with historically low rates. "As mortgage rates increase," Freddie Mac's economists say, "the demand for home purchases will likely remain strong relative to the constrained supply and continue to put upward pressure on home prices. However, the combination of increasing rates and increasing house prices would be a double hit to affordability for first-time home buyers."

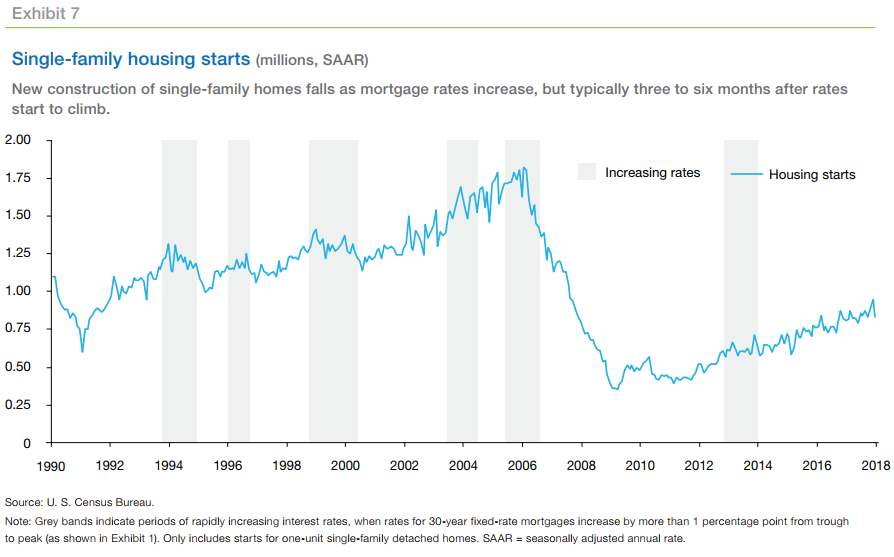

Home builders are also affected by rates as fewer home sales ultimately mean less demand for construction of new homes. This group actually gets a double whammy; squeezed by a fall in demand then by an increase in the cost of construction financing. Exhibit 7 contains the recent history of single-family housing starts since 1990, with seasonal adjustment. The reaction to rising rates here is also a delayed one.

In a second part of the Outlook piece McManus and Yannopoulos look at the risk factors driving rates and look at three scenarios for the next cycle of mortgage rates. We will summarize that in an upcoming article