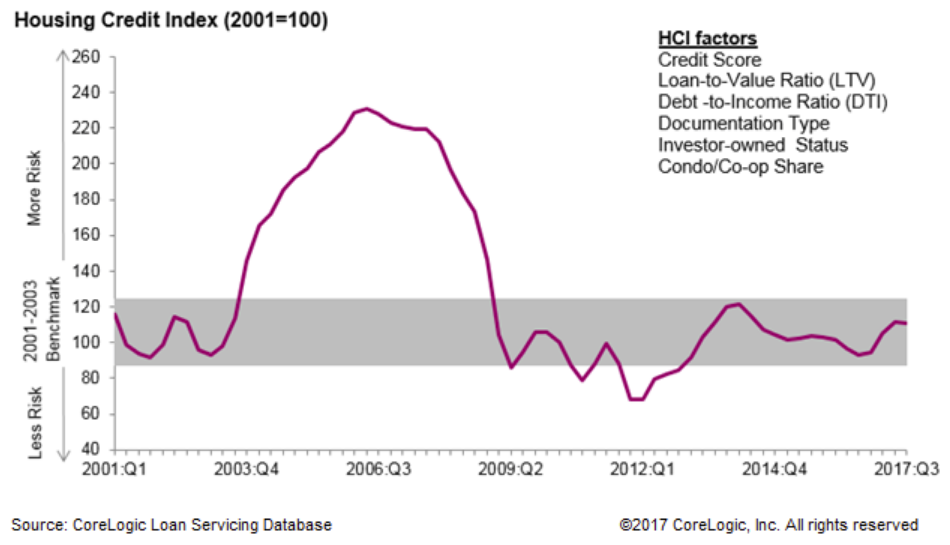

Mortgage credit risk has edged up over the last year, but CoreLogic says that it remains well within an acceptable range, comparable to that of loans issued in the early 2000s. The company analyzed six credit risk attributes in newly originated loans, and has released the results of its Housing Credit Index (HCI) for the third quarter.

The company's index indicates the relative increase or decrease of in credit risks in the following categories; borrower credit score and debt-to-income (DTI) ratio, loan-to-value (LTV) ratio, portion of loans that are investor-owned, the condo/co-op share, and documentation level.

The HCI rose 18 points between the third quarter of 2016 and the same quarter this year, increasing from 93.1 to 111.1. Despite the increase, the company says the risk level is still within the HCI benchmark range of 90 to 121, based on the HCI value for 2001 to 2003; years considered to have a normal baseline for risk.

The increase in risk was attributed, in part, to a shift in the purchase loan mix toward investor loans and an increase in the refinance loan mix of borrowers with lower credit scores and higher DTIs. The change in refinance loans may reflect the rise in the FHA-to-conventional share of activity.

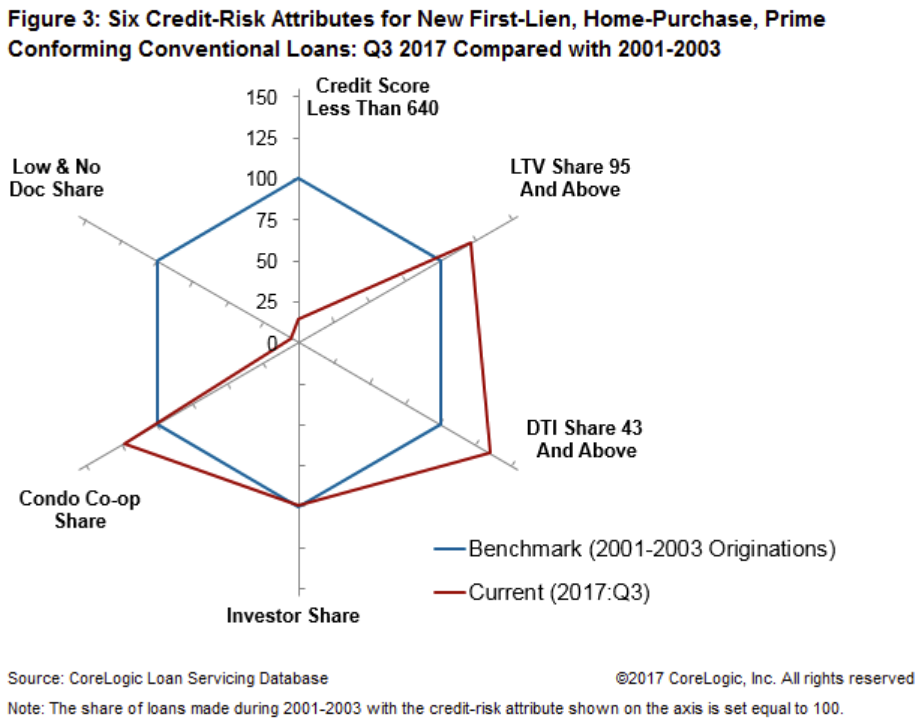

CoreLogic highlighted some of the findings behind the HCI score, comparing some of them to 2001, the first of the baseline years.

- Credit Score: The average credit score for homebuyers increased 7 points year-over-year, from 739 to 746. However, the share of homebuyers with credit scores under 640 was 2 percent compared with 25 percent in 2001. In other words, the Q3 2017 share was less than one-tenth of the share in 2001.

- Debt-to-Income: The average DTI for homebuyers in Q3 2017 was unchanged from Q3 2016 at 36. The share with DTIs at or above 43 percent was 22 percent, down slightly from 24 percent in Q3 2016, but up from 18 percent in 2001.

- Loan-to-Value: The LTV for homebuyers dropped by almost 2 percentage points year over year, down from 86.4 percent in Q3 2016 to 84.9 percent in Q3 2017. In Q3 2017, the share of homebuyers with an LTV greater than or equal to 95 percent has increased by almost one-third compared with 2001.

- Investor Share: The investor share of home-purchase loans increased slightly from 4 percent in Q3 2016 to 4.4 percent in Q3 2017.

- Condo/Co-op Share: The share of home-purchase loans secured by a condominium or co-op building increased from 10 percent in Q3 2016 to 11.5 percent in Q3 2017.

- Documentation Type: Low- or no-documentation loans remained a small part of the mortgage market in Q3 2017, increasing from 1.5 percent to 2.2 percent of home-purchase loans during the past year.

Frank Nothaft, chief economist for Core Logic, says, "The CoreLogic Housing Credit Index is up compared to a year ago, in part reflecting a shift in the mix of loans to the purchase market, which typically exhibit higher risk. Further, the Index shows higher risk attributes for both purchase and refinance loans, although the risk levels still remain similar to the early 2000s.

"When looking at the two most recent quarters in which the mix of purchase and refinance loans were similar, the CoreLogic Housing Credit Index for each segment remained stable. Looking forward to 2018, with continuing economic and home price growth, we expect credit risk metrics to rise modestly," he said.