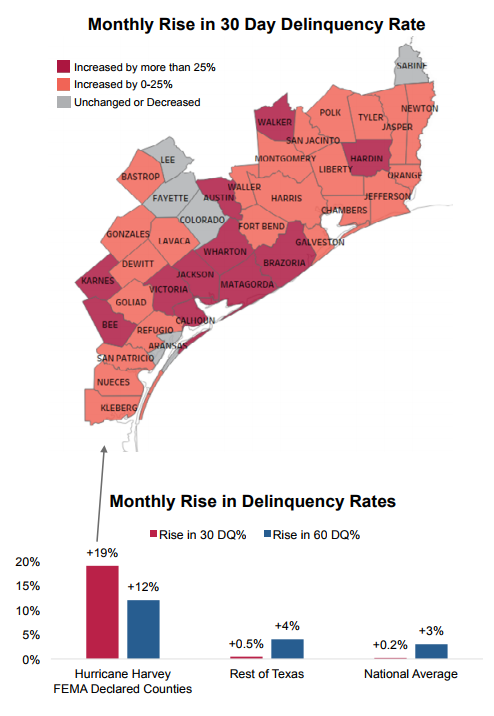

Even though Hurricane Harvey didn't hit the Houston area until very late in August, its effects are already being felt on mortgage performance. Black Knight's Mortgage Monitor for August, released on Monday, reports that, in the Federal Emergency Management Agency (FEMA) disaster designated counties, delinquencies were at close to a 17-year low before the storm, but spiked 16 percent in August, taking the rate to a 3.5 year high. Loans that were 30 days past due were up 19 percent and those 60-days or more were up 12 percent. Whether attributable to Harvey or not, the national rate jumped 0.72 percent to 3.93 percent.

Breaking the numbers down further, there were over 6,700 new 30-day delinquencies that could be attributed directly to the storm while another 1,000 borrowers who were already behind missed another mortgage payment. The report says that based on observations from earlier storms, the heaviest impact on loan performance won't come until September.

The Monitor reported earlier that, extrapolating from the experience provided by Hurricane Katrina that hit Louisiana and Mississippi in 2005, there could be as many as 300,000 borrowers who will miss one or more mortgage payments because of Harvey and perhaps 160,000 could become seriously delinquent.

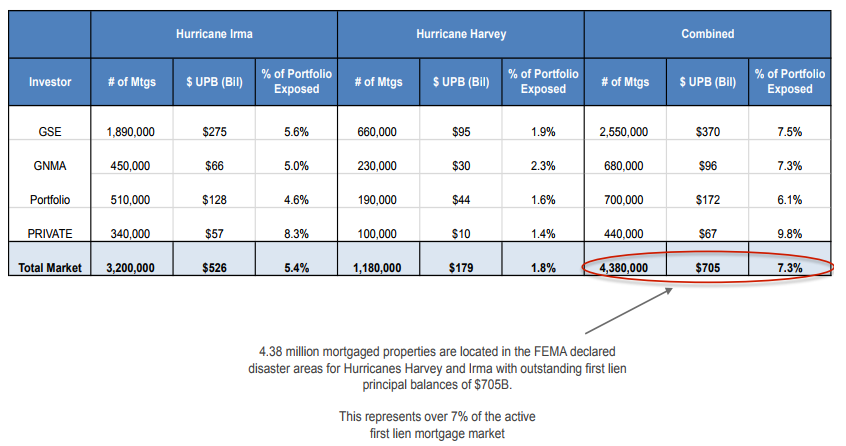

Hurricane Irma, hit two weeks later and the two are already considered among the five costliest hurricanes in U.S. history. The combined number of mortgaged properties within the areas surpasses even Superstorm Sandy in 2012 when 3.75 mortgaged properties were counted in FEMA disaster areas, although the UPB exposure in Sandy was higher.

Only now are post-Irma mortgage payments coming due, but figures provided by Black Knight indicate that mortgage performance may sufferer more from that storm than from Harvey. Their report lays out some comparisons between the housing finance conditions in the two areas before the storms that may not bode well for the aftermath.

First, Harvey's greatest damage may have been done been in an area that had largely recovered from the housing crisis. As noted, the delinquency rate was extremely low and home prices in Houston were at an all-time high, while home prices in Florida remain 17 percent below their 2006 peak. Only one metropolitan area in the FEMA designated disaster areas, The Villages, had returned to within 15 percent of its price peak. Other areas, like Cape Coral and Fort Meyers remain 25 percent below their peak.

The 39 counties impacted by Harvey have an estimated 1.18 million mortgaged residential properties. These properties account for $179 billion in unpaid principal balance (UPB), nearly one third of the total in Texas, and 2 percent of the entire country's first lien market. Seventy-five percent of these properties are located three counties, Harris, Fort Bend, and Montgomery.

The 48 disaster areas affected by Irma include over 90 percent of Florida's mortgaged properties and $526 billion in UPB; 5 percent of the U.S. Market. Nearly three times the number of borrowers were impacted by Irma as by Harvey.

Further, before Harvey made landfall, the average combined loan-to-value ratio (CLTV) for homeowners in the affected areas was 53 percent. This is the lowest average CLTV since before 2004 and means homeowner equity in the affected areas was about $131,000 per borrower. Fewer than one-half percent of homeowners in the area were in negative equity, one-seventh the national average, and less than 4 percent of properties had CLTV ratios of 90 percent or greater.

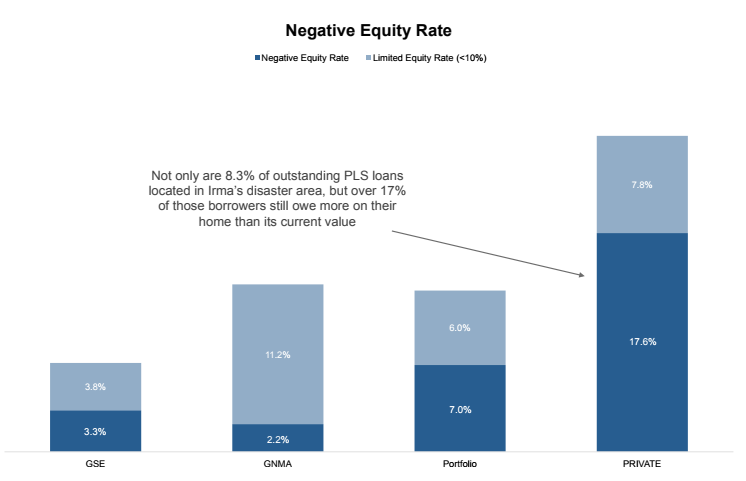

Again, Florida is a different story. The Monitor estimates that of the 3.2 million borrowers impacted by Irma, 170,000 (5.3 percent) were still in negative equity positions with another 180,000 (5.6 percent) having equity of less than 10 percent. The average mark-to-market CLTV for Irma-impacted counties is 57 percent, higher than both Harvey's as noted above and the national average which is also 53 percent. Nationally, just 2.8 percent of homeowners with mortgages (1.4 million borrowers) remain in a negative equity position.

Black Knight estimates that investors have a total of nearly 4.4 million mortgages in the two affected areas, with a total UPB of $705 billion. This means that 7.3 percent of their total portfolio is exposed. However, 5.4 percent of their portfolio is exposed in Irma impacted areas alone.

By volume, the GSEs and Ginnie Mae have the most exposure (3.2 million loans, $466 billion in UPB), but in terms of share of total portfolio exposed, private-label securities (PLS) are most impacted. Nearly one out of every 10 loans remaining in a PLS was impacted by one or the other of the storms. Not only are 8.3 percent of outstanding PLS loans connected to properties within Hurricane Irma-related disaster areas, but over 17 percent of those same borrowers remain in a negative equity position with an additional eight percent having less than 10 percent equity. All in, as many as one in four PLS loans in Hurricane Irma's path had limited equity available, prior to any potential home price impact due to storm damage.

As Black Knight Data & Analytics Executive Vice President Ben Graboske explained, even though Harvey-impacted borrowers received heavy damage, against which they were largely uninsured, they have a greater equity stake, which may bode well for long-term recovery. He noted that the average CLTV in that area was right on par with the national average and the per-borrower average equity "works out to a lot of skin in the game, and will likely serve as strong motivation for borrowers not to walk away from a storm-damaged home."

"In Florida, Hurricane Irma impacted a much larger portion of the state. The 48 FEMA-declared Hurricane Irma disaster areas include over 90 percent of the state's mortgaged properties. To put this in perspective, that means that by balance, over five percent of all mortgages in the U.S. are included in Hurricane Irma's disaster areas. Unlike Houston, though, where all-time-high home prices have contributed to a significant reduction in negative equity, home prices in Florida remain 17 percent below their 2006 peak.

He adds, "In addition, over 75 percent of mortgages in the Hurricane Harvey footprint are held in Fannie Mae, Freddie Mac or Ginnie Mae securities. Therefore, the bulk of borrowers affected by the storm will be able to find assistance under the various foreclosure moratoriums and forbearance programs that have been instituted. While we have already seen an early spike in delinquencies in Hurricane Harvey-impacted disaster areas, with many more likely to follow in September's data, the combination of available assistance and healthy equity stakes on the part of borrowers are both very positive signs for the long term."