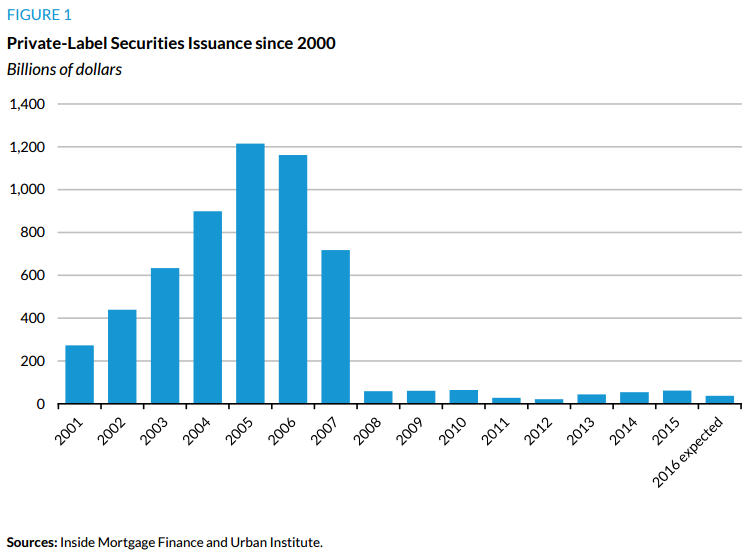

While securitization of auto loans is about 16 percent higher than it was in 2001 and agency mortgage-backed securities (MBS) are up over 50 percent, the issuance of private-label securities (PLS), which collapsed in the housing crisis, has not rebounded. They are down by more than 70 percent since 2001 and 95 percent since they peaked in 2005. In a paper written for the Urban Institute's Housing Finance Policy Center, Senior Fellow Jim Parrott discusses why, when capital is flowing through virtually every other secondary market channel, is it avoiding this one and what might be done about it.

Parrott says right now the PLS economics just don't work. Issuers can't match the yield of government backed issues relative to the risks and they can't compete with portfolio lenders because banks have a lower cost of funds, better capital treatment and are willing to price aggressively give their returns they are getting. This will eventually change as banks find more attractive investments.

Many policymakers have called for a drastic reduction in loan limits, making banks wary of taking more risk than they do now and leaving the new field open to PLS. But Parrott contends this, rather than creating a vibrant PLS market, would result in something of a "secondary market desert" in the space left behind by government-backed lending. Some investors might enter, but not many, and those that did would be chasing yield only for the lowest risk borrowers.

The second problem he sees is the lack of a reliable securitization infrastructure. The one that had existed, where investors could rely on issuers, underwriters, and ratings agencies to evaluate the quality of the securities and on trustees, servicers, and attorneys to protect their investment, was exposed by the housing crisis to be far weaker than investors thought. They no longer trust those who were supposed to guide and protect them.

To top it off, they question whether the government will respect their property rights in another choppy market. Local governments have "flirted" with eminent domain and the federal government seemed willing to allow servicers to drain investors' collateral to satisfy penalties for their own alleged wrongdoing. "All in all, where before investors saw a well-developed system of parties looking after their interests, now they see a dizzying array of risks over which they have little control," Parrott says.

Consequently, investors now expect to protect their interests with detailed contractual provisions coupled with enough transparency and tools to enforce those protections. They want to take the responsibility for understanding and managing their risk into their own hands-because they no longer trust others to do it for them.

Parrott calls reversing this "a monumental lift," one that requires creation of an extremely complex, and often much more expensive, deal structure to provide the needed certainty. One that defines in granular terms representations and warranties, due diligence standards and disclosures, breach reviews and servicing oversight, bondholder communication and recourse, and many other dimensions. Even with an incentive, and sufficient time and resources, those that might be willing to attempt this lift may still find that the existing economic are still too much of a challenge to make sense of the risks involved in the effort.

So, things are in a bind, because only after someone goes to the trouble of fixing the gaps in the existing system will there be a return of the PLS market. This leaves us with a Catch-22: "only with a strong market is it worth spending the time and money to take the steps necessary to create a strong market. "

Add to this the regulatory complexities; exactly how to apply TRID or the qualified mortgage rule for instance, may result in different answers from each of the three or four entities charged with reviewing loans. This could lead to a dizzying escalation of more documentation and disclosures that would bury even modest, one-off attempts at PLS issuance.

Parrott has some concrete suggestions for building the infrastructure needed for the PLS market to take off again. We will summarize these suggestions and their possible ramifications in a subsequent article.