Anyone who has been paying attention must know that the national homeownership rate, which has been dropping for over a decade, is now at a 50-year low. But while many experts say it will continue to shrink, Freddie Mac's Economic and Housing Research Group are taking, not really a contrarian view but a more nuanced one. In an Outlook article headlined by Sean Becketti, chief economist and Len Kiefer, Deputy Chief Economist, lay out their arguments for questioning the pessimism.

The homeownership rate in the US peaked at 69.2 percent in the last half of 2004, the middle of the housing boom but since the housing crash, the recession, and its aftermath has declined to less than 63 percent. The economists say this decline has triggered debate among housing experts, "especially among those who view broad access to homeownership as a signature achievement of American economic policy." There is particular concern about the drop among demographic groups that have historically had lower than average rates such as African Americans among whom the rate has dropped from the 2004 peak by 8 percentage points to 41.7 percent, the lowest of any ethnic group.

According to some experts the national rate could fall even further with 60 percent not being out of the question. The article looks at how likely it is the projections are right and why experts make them. Who will own those homes? Will groups hard hit over the last decade be stuck indefinitely at lower rates than the population as a whole?

While a concern to economists, the rates today are not low by historical standards. For most of the first half of the 20th Century homeownership rates varied between 44 and 48 percent. Then, post-World War II, the G.I. Bill, the institutionalization of the 30-year fixed rate mortgage, creation of VA, FHA, Fannie Mae and Freddie Mac all played a role in pushing the rate over 60 percent by 1960 and to its ultimate 2004 peak.

Any forecasts of the future presume it will look much like the past. Homeownership rates are no exception, relying primarily on historical differences across age and demographic groups and on Census estimates of the growth (or decline) of those cohorts. Homeownership increases with the age of a group, rapidly in early years as people marry, start families, and advance in their careers while gains after age 35 are at a much slower pace. There are also ethnic/racial disparities with white, non-Hispanic households (Whites) having rates typically 18 to 28 percentage points higher than African-Americans (Blacks), Asians, and Hispanics even after accounting for differences in income and education.

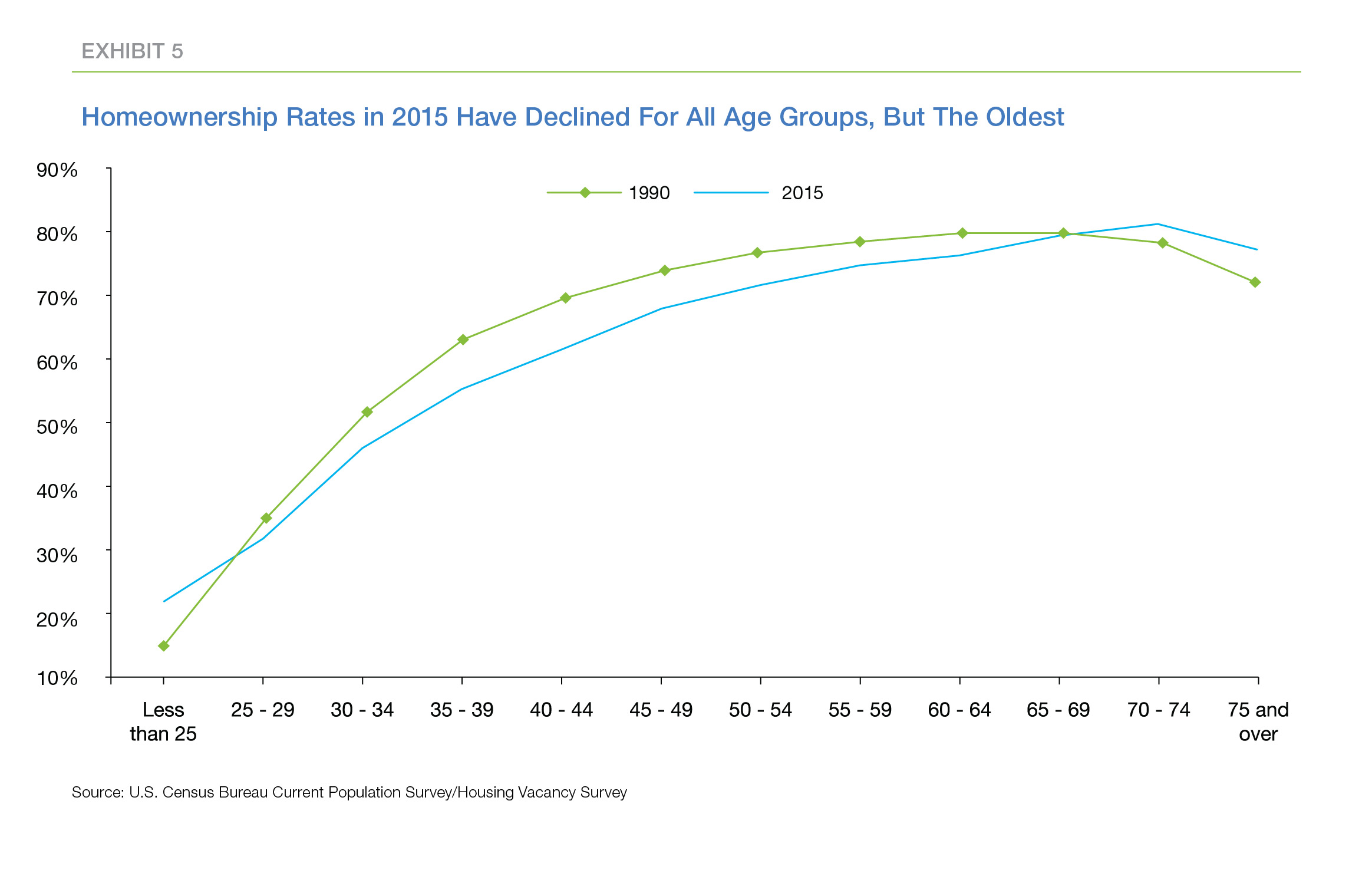

If these age and demographic differences never changed, homeownership projections could be very accurate just by knowing the projected path of each group for every future year, but of course it's not that simple. Becketti says age- and demographic-specific differences in homeownership rates are not immutable. For instance, Exhibit 5 compares the relationship between age and homeownership in 2015 to the relationship in 1990. Those in the age 30 group had a higher ownership rate in 1990s than they do today, perhaps because of today's high student debt burden or maybe cause of tighter credit policies. Alternatively, the appeal of homeownership might be shrinking, in part in reaction to the housing crash. Most likely, it due to a combination of the above that accounts for much of the uncertainty about projections.

Changes in the housing and mortgage industries, in public policy, and social attitudes, future macroeconomic shocks like the Great Recession can alter the future. In 20 years today's Millennials may not act exactly like today's Baby Boomer 55-year-olds - or they might. This is where experts begin to part ways.

Todays 60- to 64-year-olds had a rate of 63 percent when they were 35 to 39; today it is 13 points higher. But Millennials have a rate eight points lower than their contemporaries of 25 years ago. Do the Millennials portray a permanently changed attitude? If so, their rate 20 years hence may be around 68 percent-13 percentage points higher than it is today but 8 percentage points lower than today's Boomer rate, reflecting both the effects of age and generational differences. But perhaps Millennials are only in transition and will catch up to their predecessors as the effects of the recession ebb.

Experts have argued on both sides. Prominent (although far from alone) in the debate are The Joint Center for Housing Studies (JCHS) and Urban Institute (UI). Freddie Mac looks at their approaches "to emphasize the central role played by increasing diversity in projecting future homeownership rates and to question the critical assumption that the historical gaps in homeownership rates between demographic groups either cannot or will not be narrowed in future decades."

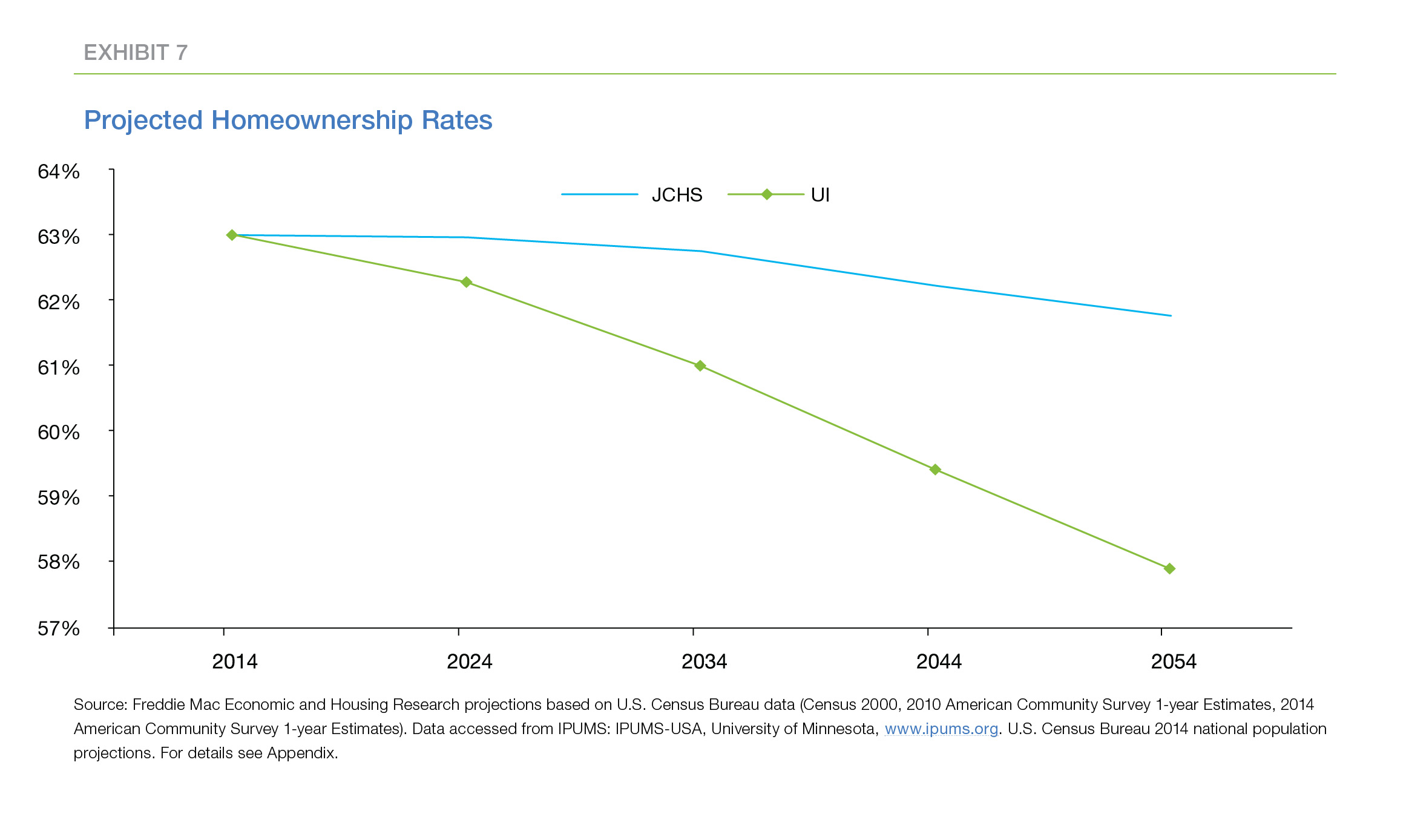

Exhibit 7 below compares two long-term projections of the homeownership rate. The solid line represents the JCHS approach, that is, it assumes that 20 years from now today's 35-year-olds will behave like today's 55-year-olds. The dashed line represents the UI theory that generational differences will persist over time.

JCHS projects homeownership will remain around 63 percent until 2024 and then will fall steadily, reaching 62 percent by 2054. UI projects an immediate and much more severe drop with the homeownership rate falling below 60 percent by 2044.

While the numbers are different, the shape of both of these projections portray a relatively stable homeownership rate for a decade followed by a steady decline and represent the conflicting influences of an aging but more diverse population.

The country is aging and the larger share of older Americans accounts for the near-term stabilization in the projected homeownership rate. But counterbalancing that is the expected increase in diversity. Whites comprise 73 percent of the Baby Boom generation but only 59 percent of Millennials are non-Hispanic whites. "If historical demographic differences in homeownership rates persist, this increased diversity eventually will produce a lower homeownership rate."

The UI approach projects a homeownership future similar in shape, but at a much lower level. This reflects the lower homeownership rate of Millennials compared to Gen Xers and Boomers when they were the same age. UI assumes that this difference represents a permanent characteristic of the Millennials rather than a temporary deviation from historical norms and arrives at a more pessimistic view than does JCHS; projecting a three-point lower homeownership rate by 2044. Both approaches assume that demographic differences will persist; maintaining the gaps between whites and other ethnic groups.

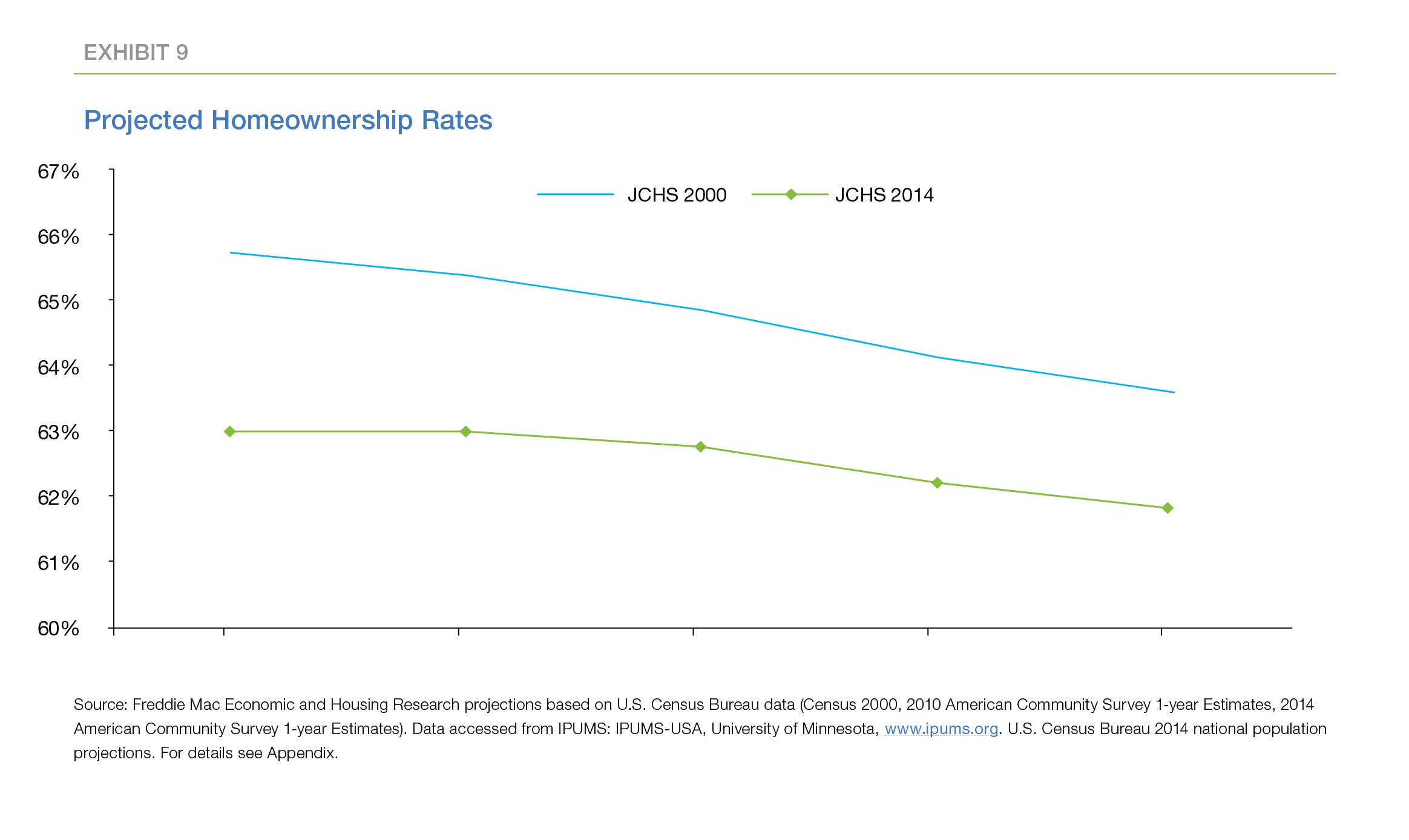

Both approaches have troubling aspects but Freddie Mac's economists find them overly pessimistic and while it uses the JCHS projections it changes the starting point. In Exhibit 9 the higher, solid line represents a projection based on the Census data only through the year 2000 while the lower, dashed line carries information through 2014. The earlier data suggested the homeownership rate in 2014 would be almost 66 percent, when, in fact, it turned out to be more than three percentage points lower. The gap between the two projections narrows a bit over time but still exceeds two percentage points as late as 2054.

The years since 2000 have, of course, been turbulent and both JCHS and UI approaches "project future homeownership rates by, in essence, applying some fancy arithmetic to current conditions. These approaches do not-nor do they claim to-incorporate future macroeconomic disruptions, significant policy changes, or shifts in social attitudes in their calculations. These types of influences ultimately will determine how accurate or off-target the JCHS and UI projections are."

Freddie sees at least three types of unforeseen influences.

- The future of housing finance is not yet sorted out and no one knows the fate of the GSEs or the consensus that will be reached on housing finance.

- Millennials may finally commence to marry, start families, and buy homes at the faster pace posted by previous generations. This catch-up has been predicted many times by many analysts and may eventually occur.

- Third, the factors accounting for the lower homeownership rates of non-white demographic groups may be overcome. This would include narrowing the education and income gap as the U.S. becomes a majority minority country and elimination of constraints on access to credit. The system today is designed for mass production of mortgages and the ability to track and evaluate borrowers and some creditworthy borrowers don't fit into today's easily evaluated categories. However, as the population becomes more diverse it will become increasingly expensive to overlook them and profit-oriented financial institutions will be motivated to find better ways to serve them.

Freddie's economists conclude the JCHS and UI approaches provide useful starting points to the discussion of homeownership; helping to "quantify 'the things that may be only' if current patterns of behavior are unchanged. However, the points listed above remind us that the actual future will be determined by a combination of industry evolution, unforeseen economic shocks, societal shifts, and the difficult policy choices that our nation has yet to make."