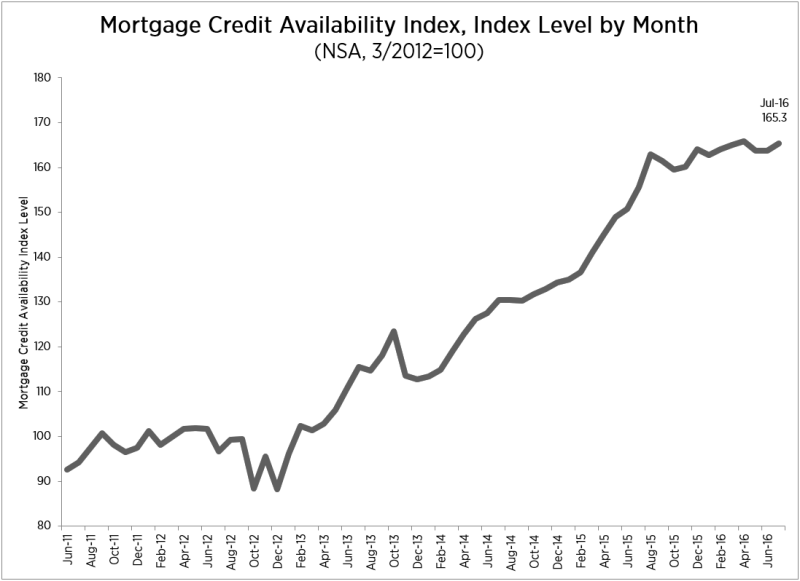

The Mortgage Bankers Association (MBA) reported that its Mortgage Credit Availability Index increased by one point in July, and announced that its methodology for constructing the index had changed. An increase in the index, which analyzes data from Ellie Mae's AllRegs® tool and MBA's survey of lenders, indicates that lending standards have eased.

The index, which was benchmarked to 100 in March 2012, increased to 164.3. Of the four component indices, the Jumbo and Government MCAIs saw the greatest increase in availability (both up 1.3 percent) over the month followed by the Conventional MCAI (up 0.7 percent), and the Conforming MCAI (up 0.1 percent).

The change in methodology has raised the relative values of the MCAI. For example, the index level for June as reported under the old index was 119.8. The change increased that value to 163.3

Lynn Fisher, MBA's Vice President of Research and Economics said "In the three years since its inception, we have been monitoring the MCAI, always looking for opportunities to improve the series and provide a more accurate gauge of credit availability. We expanded our historical series to cover over 10 years of historical data, and followed that with the introduction of four MCAI sub-indices (Conventional, Government, Conforming, and Jumbo) to help users better understand what is driving changes in the overall MCAI.

"Today we are excited to announce an updated methodology that responds more effectively to changes in the marketplace and better accounts for the frequent addition and subtraction of investor offerings," he said. "While using the exact same data, this updated methodology does a better job of reflecting new loan programs that did not exist in the base month of the index. In addition we are redefining our conforming and jumbo indices to be restricted to conventional loan programs only. Previously, conforming and jumbo status was determined solely by loan size. In the new methodology, high balance FHA and VA loan programs are not included in the jumbo category."

Fisher explained, "The main difference with this change is that the prior methodology had shown a tightening of credit over the past few months. The new methodology shows a modest loosening of credit availability over this time period, in line with other indicators of credit availability. This is a result of new jumbo loan offerings that did not exist in our 2012 base period becoming more popular and prevalent in recent periods. Our new methodology captures the addition of these new loan offerings more effectively and better aligns with anecdotal evidence of loosening credit conditions over the last seven months."

"The overall credit availability increase in July was driven by an uptick in programs that allow for refinancing among relatively lower credit score borrowers. We observed this trend in both the conventional and government programs."