Fannie Mae's economists said Friday that housing indicators continue to be mixed. In the company's April Economic and Strategic Research report Senior Vice President and Chief Economist Doug Duncan and his staff pointed to a balance of positive and negative signals in recent weeks.

First, the economy as a whole seems to have largely rebounded from the deteriorating financial conditions earlier in the year with the stock market back at 2015 levels along with some commodity prices, narrowing risk spreads, and a decline in the trade-weighted value of the dollar. However, the economists say, even if the dollar continues to weaken net exports will still subtract from growth throughout the rest of the year.

The economists say any rate hike at the April meeting of the Federal Open Market Committee is 'off the table." Increasing labor force participation and subdued wage pressure suggest the Fed leadership feels less urgency for the second rate hike and while core inflation has picked up recently the Fed will look for more concrete evidence that such firming will be sustained.

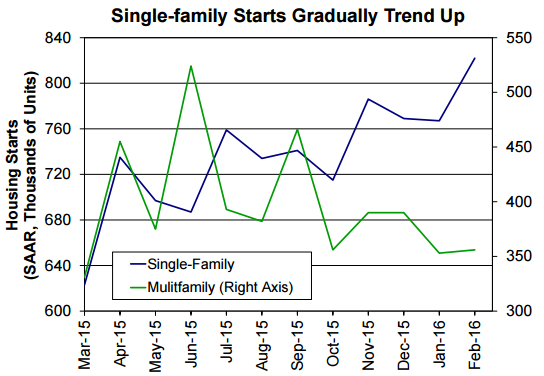

Housing positives include a gain for housing starts in February (though this has since been squashed by March's numbers), the first in three months and increasing strength in the single family sector. Despite continuing to trend down after hitting a post-recession peak last June, the multi-family segment remains positive. This is especially important in some energy-dependent markets where new supplies of units were coming on-line just as energy prices started to be felt.

On the negative side, the report cites a sharp drop in existing home sales in February along with only a modest recovery for new home sales after a drop in that sector in January. New home sales, they say, have moved sideways over the past year and builders' confidence as measured by the National Association of Homebuilders/Wells Fargo's Housing Price Index has softened since peaking at a 10-year high in October. That index however did stabilize in March although the forward looking component fell to its lowest level in a year.

Fannie Mae points to low inventories as one cause of the softness in home sales, especially lower-priced homes. The inventory of completed new homes remains extremely low by historical standards and that may be discouraging buyer traffic. While housing completions have been increasing from 2010 lows those homes have been concentrated in large and less affordable homes.

The existing home supply is also lean; listings are not keeping pace with demand and the tight market has tended to boost prices disproportionally at the lower end. Even as interest rates decline to 2016 lows the strong price appreciation is eroding affordability for potential first-time buyers whose incomes are not keeping up with the gains. Fannie Mae sees a great deal of pent-up demand among young adults, many of whom continue to live with their parents and will likely rent rather than buy when they finally establish their new households.

Rent increases will probably moderate as more new multi-family supply comes on line and that will take some pressure out of core inflation. However again the new supply is tilted toward Class A properties and the tighter supply of lower-rent Class B and Class C units will command larger rent increases, especially for new tenants. "Elevated rental cost burdens will hurt purchase affordability by inhibiting renter's abilities to save for down payments," the report says.

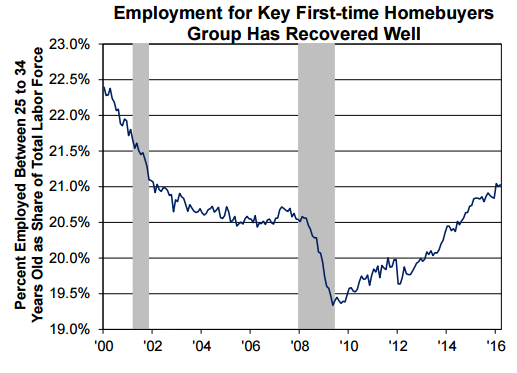

Potential first-time buyers are seeing good labor market news. Employment among those 25 to 34 years of age has increased at a healthy pace and their share of the total labor force has risen to the highest reading since 2002 although part of that is based on the sheer numbers in that age group. "A sustained increase in income among young adults, more construction of starter homes, and continued introduction of new loan products geared towards those with low down payments would go a long way toward bringing more potential homebuyers into the housing market. More first-time homebuyers should lead to more trade-up buyers spurring organic housing demand amid declining investor and international demand."

The bottom line: Fannie Mae's economists are holding to most of their earlier forecasts. They do see total mortgage originations declining about 9.0 percent in 2016 to $1.56 trillion with a 40 percent refinancing share. That share will drop to 31 percent in 2017 and originations will not increase enough to sustain overall levels. Total production volume will drop next year to $1.43 trillion.