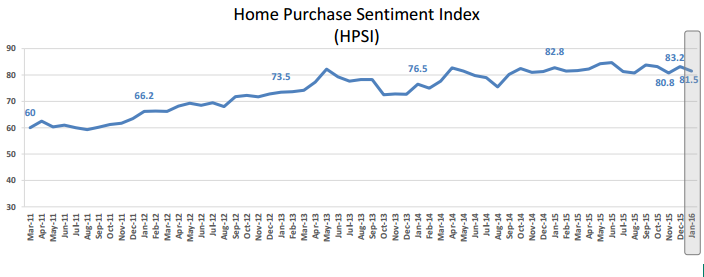

Affordability is becoming an issue based on more than just rising interest rates and rising home prices according to the latest Home Purchase Sentiment Index (HPSI) from Fannie Mae. That index dipped by 1.7 points from December to January, resulting in a reading of 81.5. Those results, the company said, reflected in part housing affordability constraints based on wages.

The HPSI distills answers to six critical questions from the monthly National Housing Survey into a single number. The survey is conducted by Fannie Mae among a sample of 1,000 consumers, both homeowners and renters and is intended to gather their current views and forward-looking expectations of housing market conditions and address topics that are related to their home purchase decisions. The questions used to construct the index are those questions consumers as to whether they think that it is a good or bad time to buy or to sell a house, what direction they expect home prices and mortgage interest rates to move, how concerned they are about losing their jobs, and whether their incomes are higher than they were a year earlier.

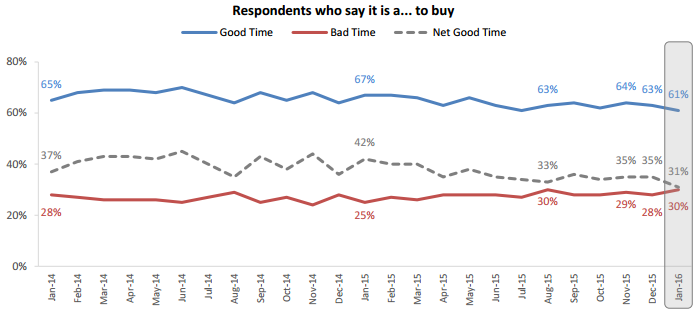

It was that last issue that caused some affordability concerns in the January results. The share of consumers who reported that their income was significantly higher than it was 12 months ago fell 3 percentage points after climbing 9 percentage points on net in December. There was also a 4 point decline in the number of respondents who said it was a good time to buy a house. That continued a net downward trend in that response throughout 2015. It now stands at61 percent, a survey low with a net between positive and negative answers of 31 points.

"Housing affordability is being constrained because the pace of growth in real income has not kept up with gains in real home prices as demand has grown faster than supply," said Doug Duncan, senior vice president and chief economist at Fannie Mae. "On the bright side, consumers have been increasingly positive about their ability to get a mortgage, suggesting that credit tightness is not the main issue limiting housing market activity today, a feeling that we also see conveyed by lenders in our Mortgage Lender Sentiment Survey®. We expect further progress in the HPSI to be limited until income growth picks up or supply, particularly in lower-priced homes, expands more rapidly."

While four of the six HPSI components decreased in January, Good Time to Sell rose by 1 point to a net of 9 percent and Mortgage Rate net expectations stayed the same at negative 52 percent. The latter number is derived from a total of 57 percent who expect rates to rise while only 5 percent expect them to fall. Fewer respondents on net said house prices will continue to rise, down 3 points to 37 percent. Overall, the HPSI is down 1.3 points since this time last year.

An all-time survey high was maintained as 85% of respondents say they are not concerned about losing their job however the net positive responses to this question fell 1 percentage point to 71%. The net share of respondents who say their household income is significantly higher than it was 12 months ago fell 3 percentage points to 12%.

The National Housing Survey asks its rotating panel of respondents over 100 questions, comparing survey answers with those over the history of the survey which began in June 2010. The phone survey seeks to track attitudinal shifts. The January 2016 National Housing Survey was conducted between January 1, 2016 and January 25, 2016. Most of the data collection occurred during the first two weeks of this period.