Are the big companies who have purchased large number of single-family homes over the last few years looking for a quick profit or are they in the buy-to-rent business for the long haul? Freddie Mac, in its latest issue of Insight & Outlook says there are going indications it might be the latter.

Landlording single family detached houses is generally assumed to be a sideline. A 1996 survey found that three quarters of such dwelling units were held by individuals or partnerships which owned fewer than 10 units and others have estimated that about half are the only rentals held by their owners.

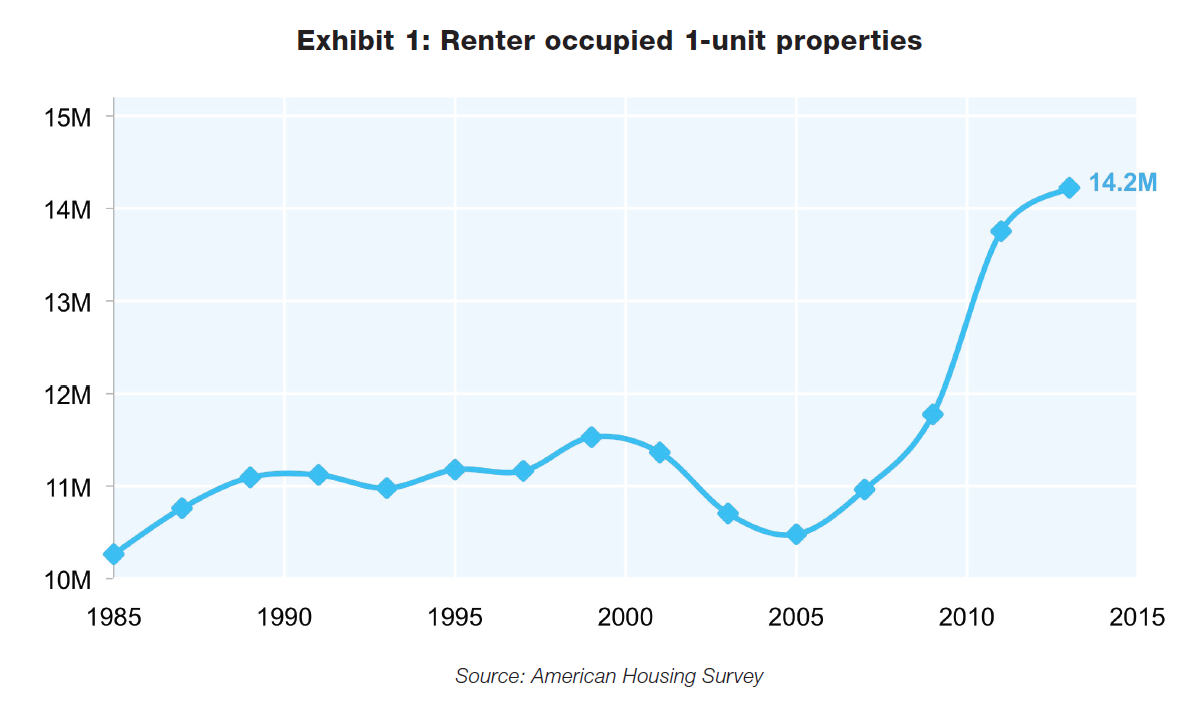

Single family units have not traditionally made up much of the market anyway, accounting for about 10 million rental units during the housing boom. With the recession however the numbers climbed rapidly to 14 million, about 35 percent of the market, in 2013. This came about through millions of foreclosures, tight credit which left many unable to purchase a home, and relocations for employment in a market not conducive to selling houses.

Freddie Mac says that a new single family rental model began to appear in 2012 when a few large investors, backed by private equity, started accumulating portfolios of single-family homes with the intention of renting and managing them. The business model of these buy to rent (B2R) firms was different than that of those that manage large apartment complexes. Intuitively big complexes should be more cost efficient to manage and maintain than scattered site properties. They can be loaded with standardized systems and appliances making maintenance and repairs more efficient. The costs of non-living areas such as landscaping can be spread across multiple units. Staff and equipment can be located on site. Obviously these advantages don't pertain to single-family houses.

The collapse of home prices is one explanation for the emergence of B2R companies. Buying cheaply offsets some of the higher maintenance and management costs while the decline in homeownership generated new demand for all rentals and for single family rentals for those not attracted by apartment living.

But if the collapse of prices was the sole motivation the article says, buying to rent should be a temporary phenomenon. Alternatively, if there is a permanent cultural shift from home ownership to renting, particularly for families, and these new companies have learned to manage networks of single family homes efficiently then large scale B2R may be here to stay.

Freddie Mac cites a recent study by James Mills, Raven S. Molloy, and Rebecca E. Zarutskie that looked at the business models of the eight largest B2R firms, tracking their property purchases from 2012 to 2014. The study focused exclusively on detached home sales and divided the purchasers into groups; individuals and corporate investors broken into groups by the number of homes purchased per year, including a category for the eight large B2R firms.

The study found that B2R remains a small part of the single-family market. Those eight companies purchased $16 billion properties over the three years and never exceeded a 2 percent market share in any year.

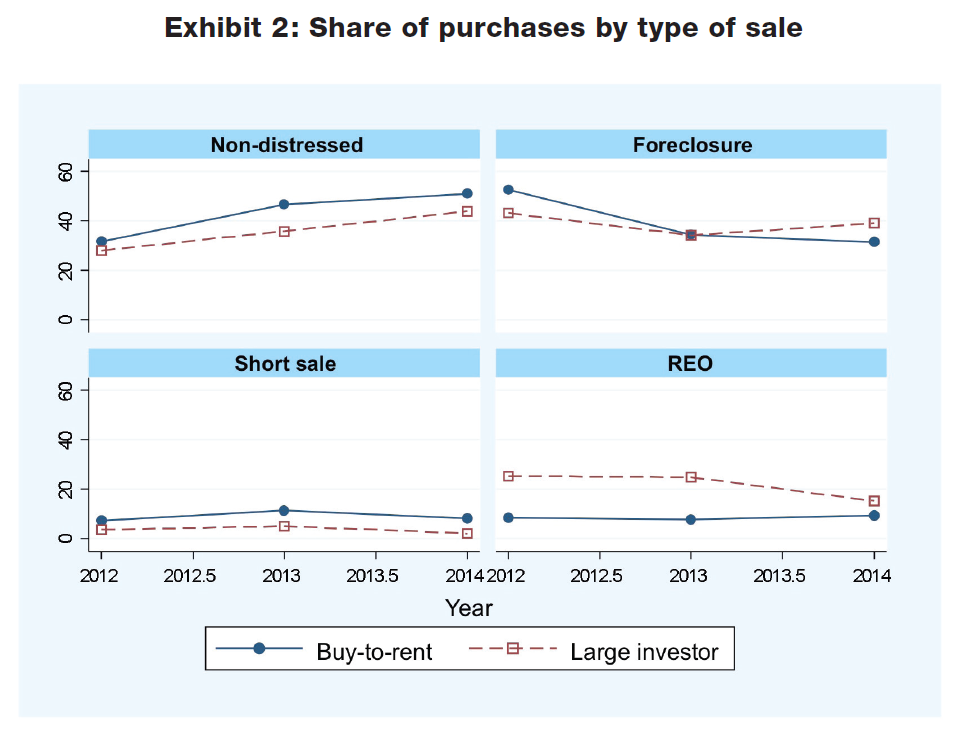

The firms, as might be expected, did buy distressed properties but each year non-distressed properties formed a larger share of purchases - from around a third in 2012 to about half in 2013 and each year they purchased a higher share of non-distressed properties than other large investors. They also purchased a relatively smaller share of lender-owned properties (as opposed to foreclosures and short sales) which tend to be in poorer condition, than did other investors. They spent more on repairs and renovations, an average of 20 percent of the purchase price of each unit while purchasing homes that tended to be newer, larger, and on smaller lots than those purchased by other large investors. Such homes should have less need for renovation and repairs, yard maintenance is reduced, and the larger size suggests a decision to concentrate on family tenants - all indicative of a longer term strategy.

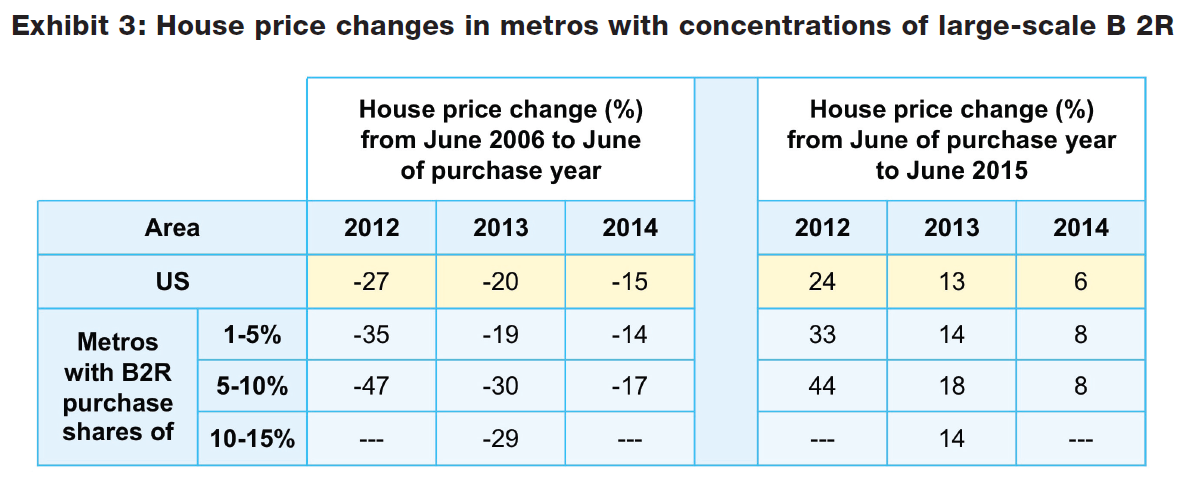

The B2R firms concentrated purchases in a few metro areas, particularly in the Southeast and even constituted a major market in some; for example accounting for 12 percent of single-family purchase in Atlanta in 2013. They also tended to purchase homes that were more tightly clustered within a metro area than did other investors. The reason for this is not clear - do clusters promote easier management of long-term acquisitions or represent a concentration in price depressed areas with a greater change of larger and quicker recoveries?

The chart below shows on the left the house price decline from the national peak to the average time homes were purchased and the right panel compares house price recovery from that purchase point to the middle of 2015. While those areas with significant B2R investment in 2012 did show higher appreciation than the national average (44 percent v. 24 percent) that difference narrowed significantly for purchases over the next two years.

Freddie Mac concludes that the emergencies of large-scale B2R firms potentially represents a new feature of the single-family rental market sector. "While the data is mixed, there are some signs that large-scale firms intend to manage their large portfolios of single-family rentals as an on-going business."