Incidents of fraudulent mortgage applications remained stable in the second quarter of 2015. CoreLogic, in its Fraud Report for the quarter, estimates the number of applications with indications of fraud at 12,814. This is an increase from the 11,100 applications that appeared fraudulent to some extent in the same quarter of 2014. While the numbers are large, as a percentage of all applications the share shrunk from an already miniscule 0.69 percent to 0.67 percent.

CoreLogic's Mortgage Application Fraud Risk Index, decreased by 8.9 percent nationally from its Q2 2014 level. Despite the size of that annual change the company says the risk has stabilized. It increased only 0.7 percent from the first to the second quarter of this year.

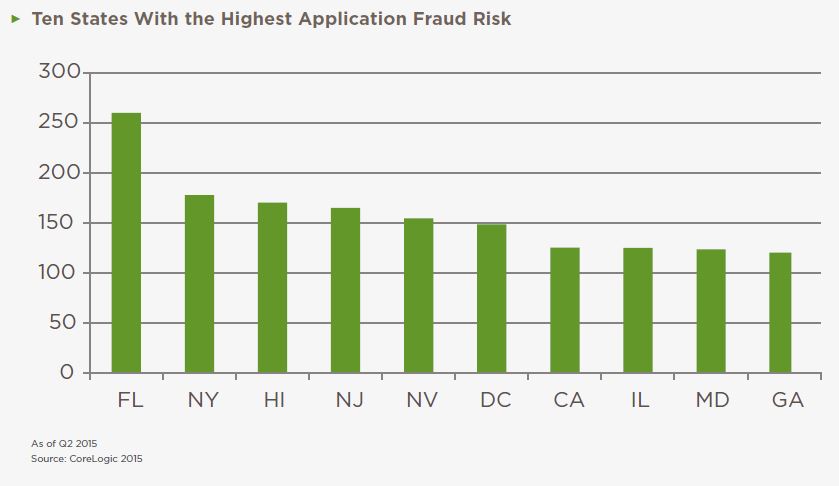

Florida remains the state with the highest overall fraud risk with an index just over 250 (we could not find a national index number in the report) while New York has moved from third position last year to second place this year with an index around 175. Rounding out the top five are Hawaii, New Jersey, and Nevada.

The largest increase in risk, 17.1 percent, was in Louisiana followed by the District of Columbia at 9.1 percent, an increase large enough to push it into the top ten in 6th position. Hawaii, Delaware, and Pennsylvania all had increases in the 7 percent range.

CoreLogic's index is based on data for six indexes that look at fraud related to employment, identity, income, occupancy, property, and undisclosed mortgage debt. Incidences of all of these types of fraud fell in the second quarter except for undisclosed mortgage debt which rose 1.7 percent compared to the second quarter of 2014 and was up 0.8 percent from the first quarter of 2015.

- Employment application fraud occurs when an applicant intentionally misrepresents job-related information such as name of employer or length of employment. This type of fraud decreased by 7.0 percent year-over-year and by 1.6 percent quarter-over-quarter.

- Misrepresentation of income decreased on applications by 7.3 percent since the second quarter of 2014 although it increased for two quarters during that interval. It was down 3.1 percent compared to Q1 of his year.

- Property application fraud was down 7.4 percent year-over-year. While it was up early in the 12 month period it fell by 13 percent from the first to second quarters of this year. This type of fraud occurs when the property value of collateral is intentionally misrepresented as being higher than market value.

- Occupancy application fraud, which occurs when an applicant deliberately misrepresents his or her intention to occupy a property to obtain a better rate or terms, decreased by 17.1 percent. Only 0.1 percent of that decline occurred in the most recent quarter.

- Identity fraud showed the greatest decrease at 22.7 percent and was down 6.3 percent quarter-over quarter. Identity fraud is when an applicant alters, creates, or uses a stolen identity to obtain a mortgage.

CoreLogic points out that multi-closing fraud risk is also a concern. This is a scheme that takes advantage of the lag between closing a loan and recording the documents to solicit multiple loans on a single property. As property values have risen so have home equity line of credit closing schemes.

CoreLogic pointed to several microeconomic factors that affected the mortgage market and the fraud rate over the 12 months ending in June. Interest rates fell from 2013 through April 2015, increasing the number of well qualified borrowers in the refinance market and increasing home values have enabled many homeowners with previously marginal equity to purchase a different property, refinance, or take out a home equity line.

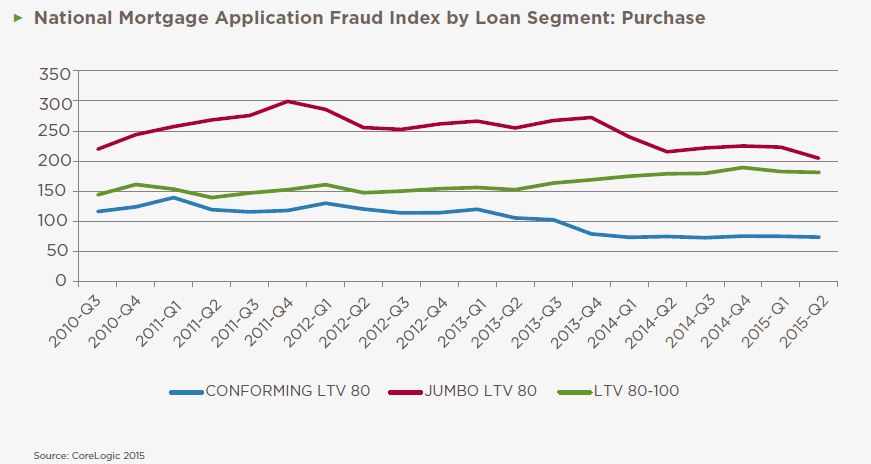

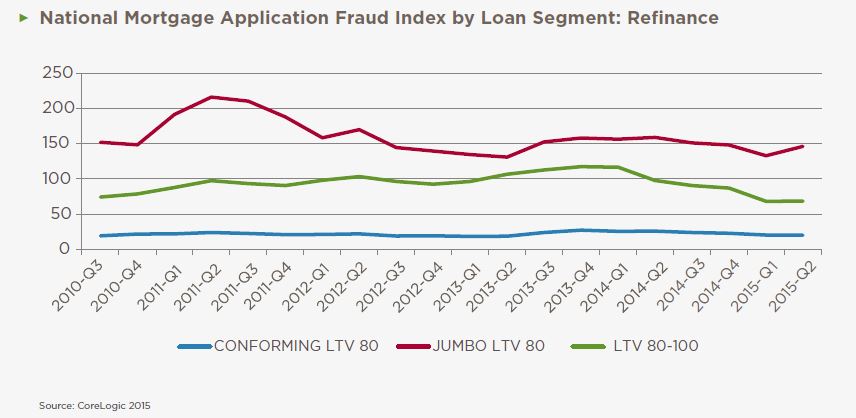

Among the various loan segments jumbo loans with loan-to-value (LTV) ratios of 80 percent or less have the highest fraud risk both for purchase mortgages and for refinancing, followed by higher LTV conforming loans. The lowest risk is for conforming loans with rations of 80 percent or less.

There are clearly geographic fraud "hot spots" as can be seen from the map below. While overall fraud trends are stable to decreasing for most of the country, CoreLogic makes special note of the Miami area. It is already the highest risk core-based statistical area in CoreLogic's index and in addition its house prices seem to be overheated and are accelerating at a far greater pace than rents for single-family homes. This suggests the prices may not be a good indicator of sustainable values. The combination of risk factors makes Miami an area warranting scrutiny.