CoreLogic has released figures showing that residential real estate in 14 of the 100 top real estate markets in the country were overvalued in the second quarter of 2015, twice the number as in Quarter 1. By overvalued CoreLogic means these markets have increased well above their long-term sustainable prices as measured by each area's real disposable per capita income.

The Austin-Round Rock metropolitan area has what is by far the largest degree of excess valuation as measured by CoreLogic's Home Price Index - 42.3 percent above its sustainable level and 31.2 percent higher than at its peak level prior to the 2007 downturn. Prices in Austin increased 10.4 percent in 2013 and 16.3 percent in 2014.

Houston-The Woodlands-Sugarland was second on the CoreLogic list with 25.4 percent overvaluation, and prices 22.7 percent above the pre-2007 peak. Three of the four remaining large Texas markets also made the list - Dallas-Plano-Irving at number eight, San Antonio-New Braunfels in ninth place, and Fort Worth-Arlington in 12th place.

CoreLogic said the Texas markets are well above their pre-2007 peaks partly due to strong job growth and partly due to the boom-bust cycle that occurred in most of the country. The oil and gas boom fueled job and population growth I the area between 2006 and 2014 but oversupply has put downward pressure on energy prices which may intensify over the next few years and impact some of the high-flying Texas markets.

Charleston-North Charleston in in third place, overvalued by 13.4 percent although less than 1 percent above its pre-crash peak. It is followed by Miami-Miami Beach-Kendall, 20.6 percent above its sustainable level but still 25.3 percent below its peak, and Washington-Arlington-Alexandria DC-VA at 19.2 percent while remaining 11.5 percent off of pre-2007 prices.

Markets that have joined CoreLogic's list since the first quarter of 2015 are Knoxville in sixth place, overvalued by 14.4 percent, number seven, Philadelphia at 14.2 percent; Nashville-Davidson-Murfreesboro-Franklin (tenth place, 12.3 percent) and Cape Coral (number 11 at 11.1 percent overvaluation). Numbers nine and ten, Silver Spring-Frederick-Rockville, Maryland (10.1 percent) and Denver-Aurora-Lakewood (10.0 percent) are also new to the list this quarter.

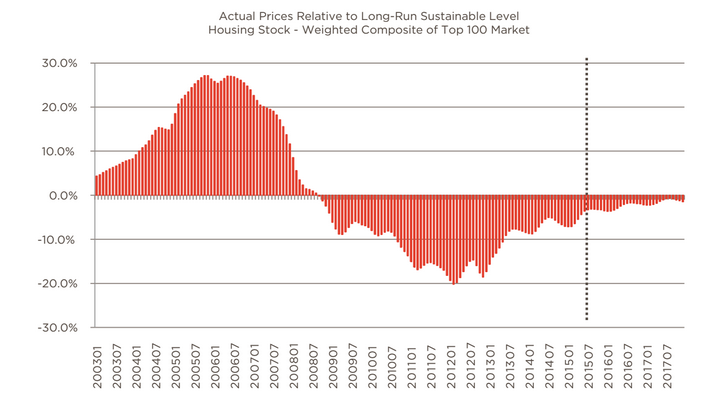

The figure above shows the gap between home prices and the long-run sustainable values for the weighted average of the 100 markets. From 2005 to 2007 home prices were more than 10 percent above sustainable levels then they fell quickly to more than 10 percent below that level from 2010 through 2013. Since then, as home prices continued to rise, the gap narrowed to 3.6 percent below the sustainable level at the end of the second quarter. The gap is expected to remain within the normal range, shrinking to 1.5 percent by the end of 2017.