Since early 2014 the Federal Reserve has held out two goals that must be achieved before it raises the Federal Funds rate, "maximum employment and inflation of 2 percent." In an Inflation Chart Book report this week Wells Fargo's Economics Group examine why inflation, or lack of it, should not preclude the anticipated September liftoff.

Economists Sam Bullard and Sarah House write that weak inflation has been the biggest impediment to the Fed normalizing monetary policy this year and inflation, while rising over spring and early summer is still not where policymakers would like it to be. Increases in the personal consumption expenditure (PCE) deflator (2.4 percent) and the Consumer Price Index (CPI) (3.5 percent) over the last three months suggests that inflation should continue to move back toward the Fed's target but these headline gains are in near-term jeopardy.

Bullard and House cite the following economic factors as stoking their concerns.

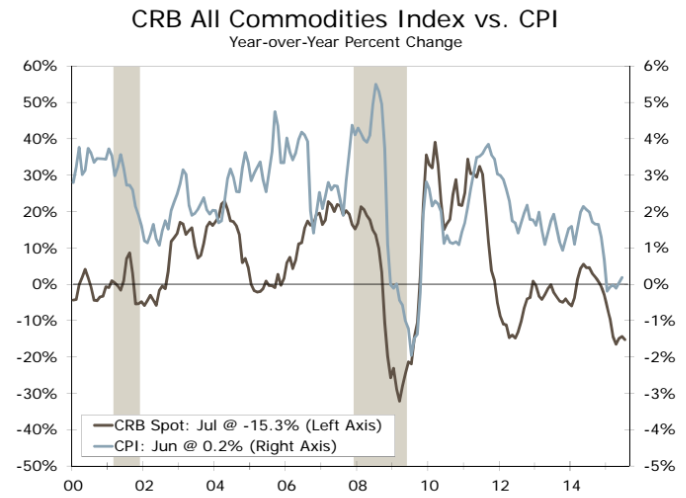

Commodity prices, including those for energy, industrial metals, crops, and livestock have tumbled recently due primarily to renewed jitters about the Chinese economy. The dollar has also continued to strengthen. The result has been an increase in the broad trade-weighted dollar index of 2.6 percent over the last month. Oil prices have fallen more than 20 percent since the end of June and the CRB metals index is at the lowest level in five years. As commodity prices tend to show up almost immediately, the 3.7 percent drop in the CRB index will likely be felt in the July inflation figures.

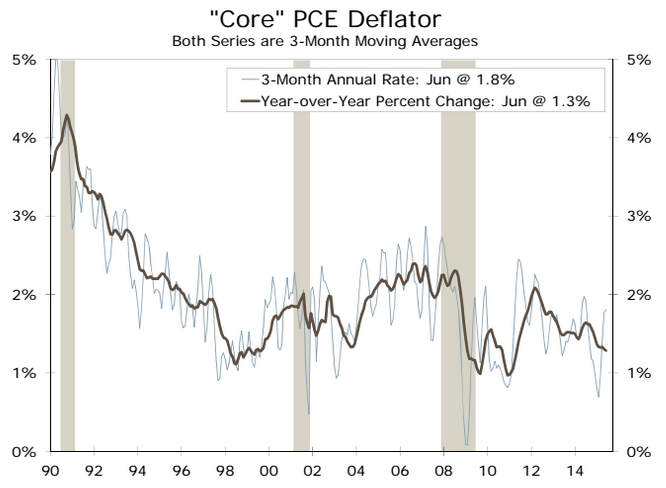

The authors speculate that a 10 percent drop in the CRB, if sustained would slice off 0.4 points from year-over-year inflation but will have a more modest impact on core inflation. The core PCE deflator increased at a 1.7 percent annualized clip over Q2 and core CPI inflation is up at a 2.3 percent pace in the past three months amid further gains in shelter, transportation and medical care costs. But will this be enough?

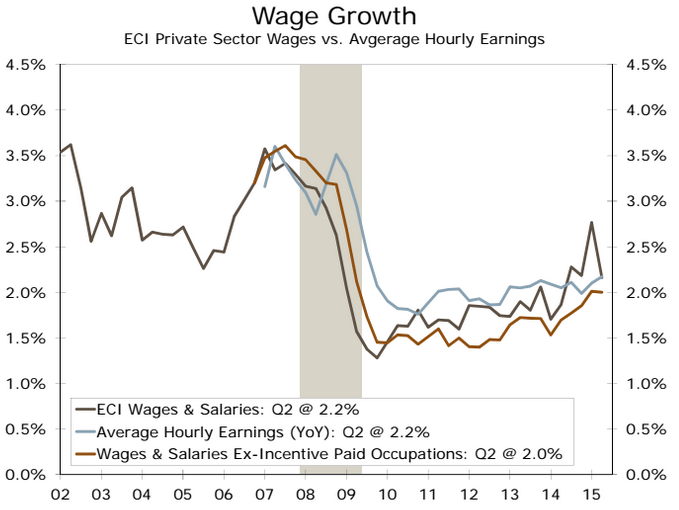

Wage inflation continues to be soft and the latest number on average hourly earnings (AHE) and the Employment Cost Index (ECI) have cast some doubt on how close the labor market is to full employment. The authors say the June AHE and Q2 ECI may have overstated the weakness in labor costs; there remains no definitive uptrend in wage growth but no abrupt slowdown either.

Core inflation, even if it improves some, is likely to stay below the 2 percent Fed target at least through next year but this alone does not preclude it from beginning to raise rates later this year. The effects of monetary policy lag implementation and the FOMC has been clear about its willingness to act as long as it looks as though inflation will hit their target within a year or two. The Fed began to lift rates in the 2004-2006 tightening cycle when the PCE deflator had risen only 1.4 percent on an annual basis and demonstrated a 1.6 annualized rate in the prior three months - close to the rate today. The difference however, the economists say, is that in 2004 commodity prices were trending higher and the dollar was weakening.

The headwinds from those two factors are not new although they have intensified over the last month. Almost all FOMC members anticipated that rates would lift off this year even when the most optimistic forecast only put the core PCE deflator up by 1.6 percent in the fourth quarter. Fed Chair Janet Yellen has increasingly emphasized that an earlier liftoff may allow a more gradual tightening which she views as the prudent approach.

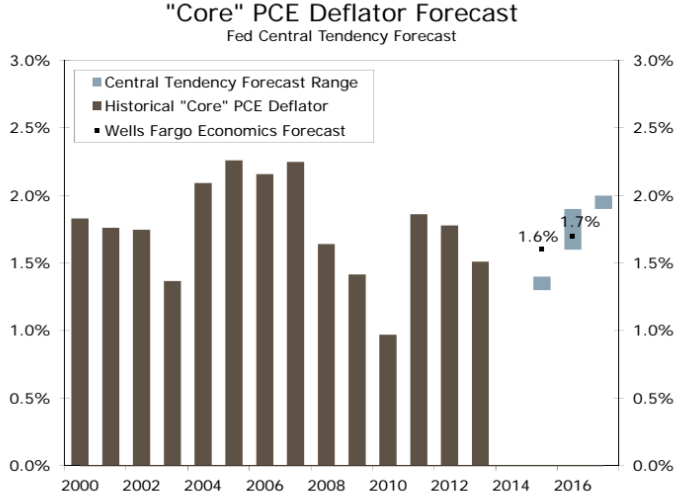

Bullard and House conclude, "We look for core and headline inflation to move gradually higher in the second half of this year, with the core PCE deflator moving up to 1.5 percent by year-end. With core inflation showing clear signs of a pickup and further tightening in the labor market supportive of stronger wage growth, our base case remains for the Fed to begin raising rates in September."