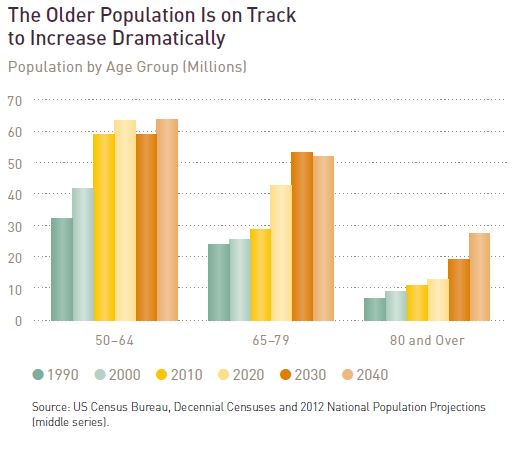

Housing America's Older Adults, a new study conducted by Harvard's Joint Center for Housing Studies for the AARP Foundation points to the problems for housing as America's population enters a period of unprecedented aging. A combination of the baby-boom generation and increasing longevity means that the country's 50-and-over population will increase about 20 percent by 2030 to 132 million people. In 15 years one in five Americans will be at least 65, a total of 73 million, an increase of 33 million in just two decades. By 2040 there will be more than 28 million persons over age 80, three times the number in 2000.

Housing, the study says, is the linchpin of well-being and ensuring the older adults have the housing they need to enjoy high quality, independent, and financially secure lives has taken on new urgency, not only for individuals and their families but for the nation as a whole.

Housing is the largest single item in most household budgets and the cost of housing directly affects the financial security of the household as well as its ability to build wealth. For older adults access to stores, services, social networks and transportation prolongs independence and for senior with health issues housing that also provides support and services can reduce the need for long-term care, a cost often paid by public funds. But, the study says, the nation's housing stock is not prepared to meet the escalating need for affordability, accessibility, social connectivity and supportive services for an aging population.

Among the deficits the study sees are:

· A lack of affordability for lower income seniors which might force them to choose between shelter and food or healthcare.

· Basic accessibility features in housing that would allow seniors to age in place.

· A transportation and pedestrian infrastructure ill-suited for those who can't or don't wish to drive.

· Disconnects between housing programs and the health care system. This can also put seniors at risk for premature institutionalization.

In addition to the implications for society these issues are intensely personal for older persons and their ability to remain independent and enjoy a high quality of life.

As the population grows older it will also become more diverse and this diversity will cause significant shifts in housing demand. Older Asians and Hispanics are more likely to live in multi-generational households than whites or blacks which will affect not only the demand for institutional care but also the financial, personal, and housing situations of family members. As a group, minorities have lower homeownership rates, lower incomes, and fewer assets, all factors in housing options.

As life expectancy increases so will the numbers of persons with disabilities requiring costly long-term care at the same time as the number of lower-income older adults will also increase even if their percentage remains the same.

The younger baby-boomers, now in their 50s, are less financially secure that previous generations following the Great Recession. Members of this large age group might not be able to cover the costs of appropriate housing or long-term care. This cohort is also less likely to have children and thus fewer family members to assist in their care.

The vast majority of those over 50 live independently, many are still in the workforce and some are still caring for children, for aging parents, or both. More than three-quarters of those over age 80 still live in their own homes and aging in place is the preference of most people.

Many older people do opt to move when they retire, the children leave home, or conversely return as adults. Sometimes it isn't an option. The death or disability of a spouse or needing more affordable housing because of a reduction in income can force moves. And on the other hand, fully a quarter of respondents said they would stay in their homes because they could not afford to live elsewhere.

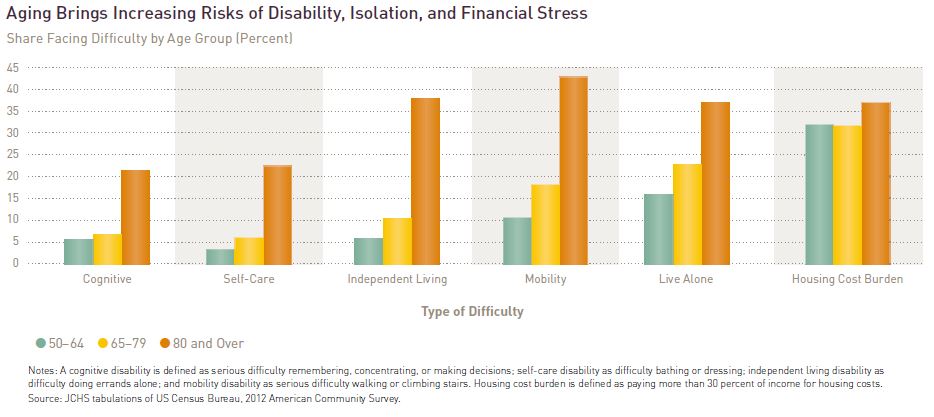

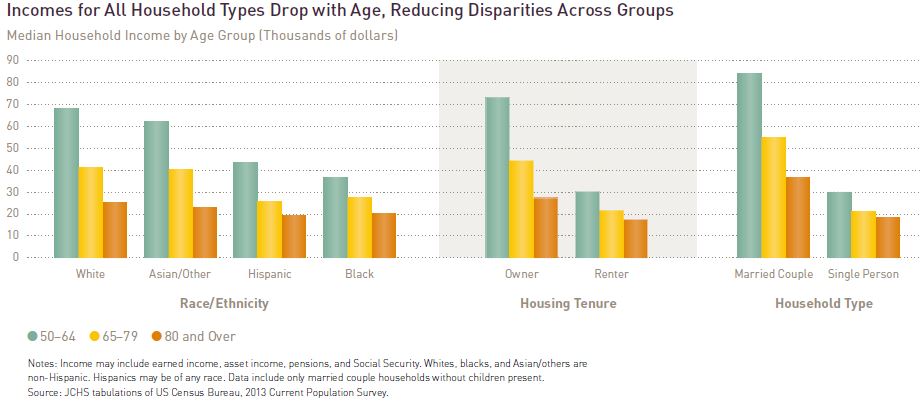

The study notes that, despite the trend to living longer and healthier, most adults and their families will ultimately face challenges of aging and many of the trends common to aging converge over time. Disability rates are higher among lower income groups in the 50-to 54 age group (a 7 percent rate among those with $60,000 or more in household income; 33 percent among those earning under $30,000), but by age 85 more than two-thirds of individuals have a disability regardless of any other demographic factor. Among disabilities, problems with mobility are the most common. Income also drops with age and reduces earlier income disparities by race and housing tenure.

The study said it is unknown whether the next generation will follow the current one in preferring to age in place or if new housing options might appear. However ensuring that they can stay in their homes affordably, comfortably and safely presents several challenges.

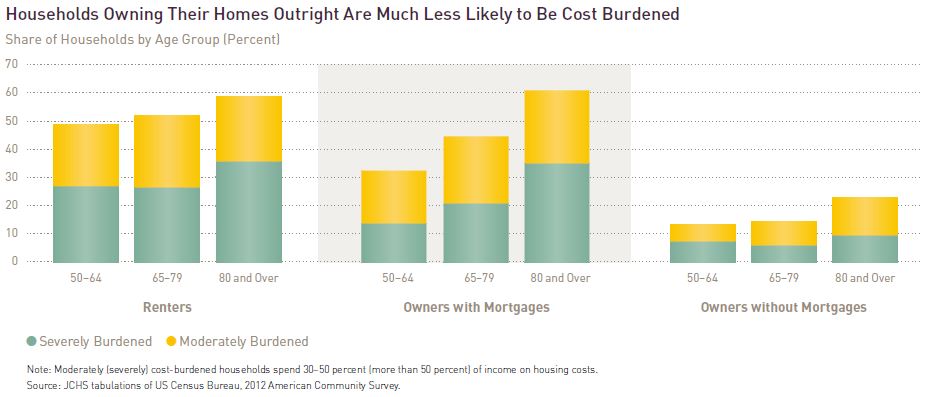

The first, as mentioned earlier, is financial. A third of adults over age 50 pay more than 30 percent of their income for housing and of those over 65 about 30 percent of renters and 23 percent of owners with mortgages are considered severely housing burdened - paying more than 50 percent of income on housing. Among severely cost-burdened households over age 50, 43 percent spend less on food and 59 percent less on healthcare and save significantly less for retirement. Older homeowners are in a better position as many do not have mortgages and even with mortgages have greater wealth in the form of equity they can draw on to support themselves or pay for long-term care.

Given the varying circumstances of older adults there is a range of responses needed to meet their needs. At the individual level adults and their families must plan for confronting the realities of aging. Financial preparations, including building savings, managing debt, obtaining long-term care insurance are important steps toward self-sufficiency as are wise choices about where and in what type of housing to live and home modifications to make will make it more possible to age safely and happily in place.

However many people simply lack the resources to do this preparation. Long-term insurance or assisted housing situations are expensive and those living in locations without social connections or family nearby may find themselves increasingly isolated as they decline physically. Thus the study says it is critical that public and private sectors take steps to ensure the support is there to provide housing, transportation, health, and service options for older persons regardless of income.

The study points to several entrepreneurial efforts in the areas of design, urban planning, health and wellness, social engagement and finance. Some cities and states are advancing housing, transportation, and walkability initiatives and developing codes to promote accessibility in private homes. Other initiatives seek to link housing with long-term care. Private companies are seeing opportunities in designing and marketing new housing technologies and services to the growing older population. A broader conversation, however, is needed to spread these efforts so that more people will be able to benefit from them.

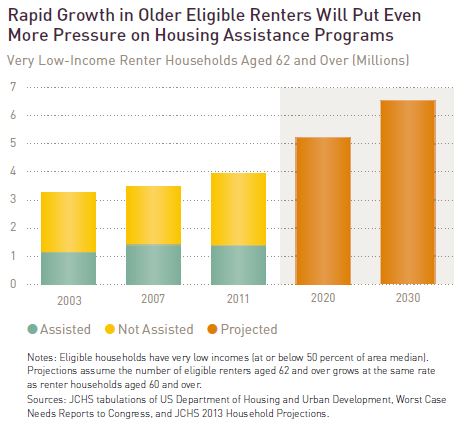

The study says that first there must be an expansion of federal efforts, especially rental assistance which currently reaches only a fraction of older renters with low incomes and high housing costs. There is also a need to fund more housing with supportive services, few such units have been added in recent years. In addition there need to be changes made to Medicare and Medicaid so as to better coordinate affordable and accessible housing with long-term care.

Where homeowners have equity reverse mortgages can be helpful in allowing them to age in place. But that program has not been broadly used and has had negative impacts in some cases. The study suggests changes to this federal program such as limiting the amount of draw down in the first years and providing mandatory counseling to potential borrowers.

State and local governments can take steps to promote accessibility and expand housing and transportation options. New construction can be required to include some accessibility features. There could be tax incentives and low-cost loans so homeowners can modify houses to accommodate persons with disabilities. Local governments could modify zoning to allow construction of accessory apartment and encourage mixed-use developments that merge housing with services and/or transportation. State Medicaid programs should reorient funding to enable aging-in-pace rather than institutionalization.

Local governments, particularly those with growing older populations, need to ensure that a range of services are available including volunteer opportunities, educational programs, adult day care and meals, and medical and wellness services.

As the private sector is beginning to realize, the growth of the older population provides many opportunities to innovate. Some areas where substantial opportunities exist is in helping older adults to modify their homes, delivery services, and developing new housing models that promote independence and integrate residents with the larger community.

The study concludes that, while there are significant challenges, the potential is there for older adults to have a higher quality of life than ever before and for communities to be more livable and vibrant as a result. This will require concerted efforts at all levels of government and by private and nonprofit sectors. It will also require advocacy from older adults themselves.