Almost one year ago Mark Palim, Fannie Mae's Vice President of Applied Economic and Housing Research, analyzed what impact rising rates might have on the housing recovery. When he wrote about this for the company's website last July, rates which had recently (in May) bottomed out at 3.35 percent had increased by 116 basis points to 4.51 percent.

At that time Palim said there was no historical precedent for knowing the impact on the housing market of an interest rate change, either up or down, because of a Federal Reserve policy of quantitative easing but we could review the history of large interest rate movements. He examined two such periods since 1990; a 14-month period from October 1993 to December 1994, when mortgage rates increased by 237 basis points (from 6.83 percent to 9.20 percent) and a longer period with a smaller rate increase, October 1998 to May 2000, when rates increased by 180 basis points (from 6.71 percent to 8.51 percent). Palim concluded that that rate changes don't have much impact on pries but do contribute to a decrease in home purchase volume and an increase in the use of adjustable rate mortgages (ARMs.) That latter change, he said, might be muted this time by the new Qualified Mortgage (QA) rule.

Rates continued to rise through that summer, reaching 4.57 percent in September. Since then they have oscillated in a relatively low range to a low of 4.10 percent and last week stood at 4.17 percent. This week the economist revisited his analysis in an article for Fannie Mae's FM Commentary titled "Mortgage Rates and the Housing Recovery - A Year Later" to see what the impact has and will have on the housing market and if his July 2013 assessment was correct.

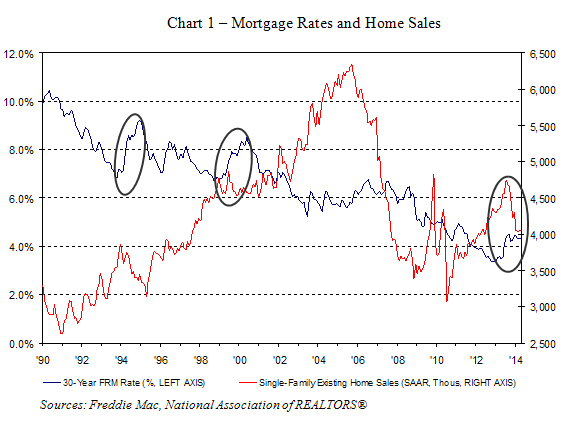

Home price and sales data through last April, he said, shows a general pattern consistent with history and his expectations in 2013; a sharp adjustment to higher mortgage rates tends to precipitate a reduction in the volume of sales rather than a decline in prices. Chart 1 shows that rising rates (80 basis points from May 2013 to April 2014) were met with a drop in existing single family homes sales of 7.7 percent. There has been an ever larger drop, 14.5 percent, from their recent high in July 2013 of 4.75 million units.

In April 2013 home prices according to several national readings including Case-Shiller and CoreLogic, were rising by double digits. Prices have continued to rise since then but the annual appreciation is no longer accelerating. Chart 1 shows the year-over-year change in home prices in April 2014 was 10.5 percent having peaked at 11.9 percent in February 2014 (CoreLogic HPI). The continued strong appreciation in home prices occurred during a period when mortgage rates rose by 80 basis points.

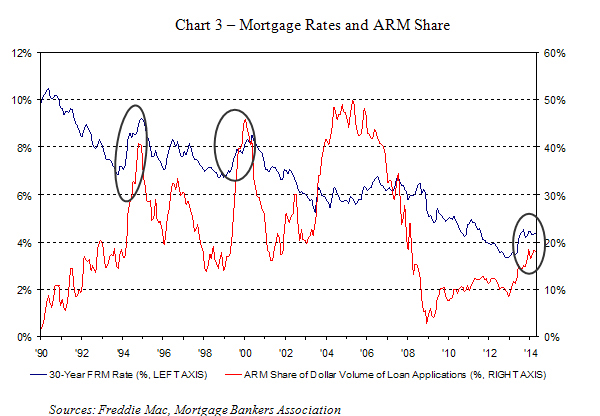

During recent earlier periods of sharply rising interest rates, the ARM share of mortgage applications according to the Mortgage Bankers Association rose to over 40 percent by dollar volume. This time, Palim says, the rise in the ARM share is nowhere near that. Since April 2013, the ARM share has risen from 11.2 percent to 18.0 percent in April 2014. "We believe this is likely due to tighter underwriting standards for ARMs, including the impact of the Ability-To-Repay rules, and recognition by some borrowers that if they opt for an ARM today, when their rate resets they are more likely to be paying a higher rate when interest rates rise to levels more consistent with historical norms."

Looking forward to the remainder of this year, Palim expects that mortgage rates will rise to the upper end of the range established over the past year as the economy recovers from what he calls a soft patch during the first quarter of 2014. Tight inventories and investor demand kept home prices rising well ahead of the growth in household income in 2013 but he expects that dynamic to wane of the course of 2014. The Federal Housing Finance Agency (FHFA) purchase-only home index which forms part of the Fannie Mae Economic and Housing Outlook, forecasts an increase of about 5 percent in home prices in 2014 compared to a 7.6 percent gain in 2013. Palim said that home sales, despite the rebound from recent lows earlier this year, will post a small decline, its first in four year, compared to 2013.