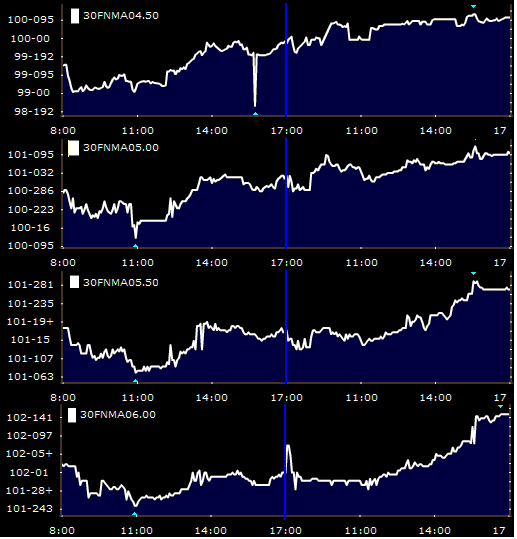

In the early to mid morning hours the recent down in coupon bid bias towards 4.5's and 5.0's prevailed as buyers looked to reduce prepayment risk exposure.... but then, early in the afternoon something odd happened...the entire coupon stack rallied in a relatively similar fashion. So today was sort of a down in coupon up in coupon kinda day!!!

If this makes no sense to you I am saying that 4.5 to 6.5 prices were bid up in a parallel fashion. This should help illustrate:

FN 4.5: +14/32 at 100-11+

FN 5.0: +8/32 at 101-09+ GN 5.0: +11/32 at 101-09

FN 5.5: +9/32 at 101-27 GN 5.5: +12/32 at 101-25

FN 6.0: +14/32 at 102-15 GN 6.0: +19/32 at 102-08

FN 6.5: +12/32 at 102-29 GN 6.5: +18/32 at 102-24

I would like everyone to pause for a moment and take out your HP 12-C Financial Calculator

Please calculate the spread between the FN 6.5 and the FN 4.5....

(102-29) - (100-11)= 82/32=256 bps!

That is a really, really, reeeeeally tightly compacted coupon stack. This spread should be between 600-800 bps. Looks like there are some confused buyers out there...or maybe the 6.0's and 6.5 just look relatively cheap...perhaps but this cant last much longer, something has to give here...maybe in the form of the bid migrating back towards the middle of the stack... 5.5's maybe...either way this spread is abnormal. I guess we need to expect the unexpected when there is an invisible hand (Ben/Hank) guiding financial markets towards the light at the end of the tunnel

Well wait a minute here is an interesting thought...

I said that the current down in coupon trend continued early in the session to mitigate prepayment exposure in portfolios. As I mentioned last night....Is this expectation of a massive refi boom overblown? Are lending guidelines too tight for any sort of boom to take place? Are the self-employed borrowers across the US going to have to wait another year in order to bolster tax returns so they can qualify for a mortgage? Only got a few responses to this question last but I believe it is a possible "Devil's Advocate" tact for buying higher yielding coupons like the 5.5s. Just a thought...doesn't mean rates are going higher anytime soon but it could potentially be one of those "DOH" moments for the MBS portfolio manager who finds out prepays were not as broad as expected and they could have actually made more yeild. Let us know what you think. We like to hear what you have to say...I started a discussion in the MBS Forum. You can access by clicking on the link below.

Are Fed/Treasury Funded Low Mortgage Rates Enough to Spark a Refi Boom?

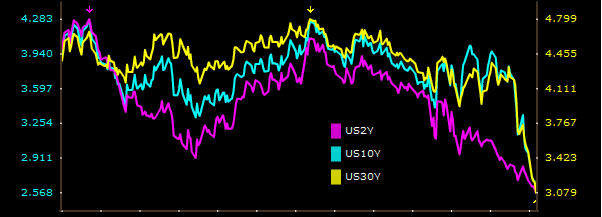

Since the current craze seems to be uncharacteristic deviations from the norm...lets talk about Treasuries and their recent relentless plunge towards ZERO.

News that other Central Banks besides the US are drastically cutting interest rates helped Treasury yields fall further towards the nothing range overnight. The Bank of England reduced the official Bank Rate paid on commercial bank reserves by 1.0 percent to 2.0%. The ECB cut their benchmark lending rate by 75 bps to 2.5%, which by the way is the BIGGEST CUT EVER. There was humor is this rate cut by the way....Jean-Claude Trichet refused to provide any forward looking comment on the outlook for future rate cuts. I think he may be a bit embarrassed about the stubborn stance he took on inflation, you remember, the one he refused to give up until Bernanke and Paulson started printing money. Last but not least we have Sweden's Riksbank, the show stealer , they cut their benchmark lending rate 175 bps to 2.00%. Its bad everywhere people, don't feel like we're going through this alone.

After rallying overnight the US Treasury session opened with a bit of profit taking. Yay finally some spread tightening......NOT!!!!! Unfortunately the selling only gave desperate, duration hungry buyers and short positioner's the opportunity to buy the on dip.

And then it happened...call Guinness...towards the day's end equity market sold off and the yield on the long bond (30 yr) dropped to 3.05%. That's a record low! The 30 yr swap spread is now -31.75. Negative swap spreads make my brain hurt...this implies that the 30 yr Swap has less credit risk than a 30 yr US Treasury....what a backwards world we operate in these days. I wont go into specifics lets just say this doesn't make any sense...but again...that IS the theme lately. Nonsensical Ridiculousness

The 2 yr note closed yielding 0.83%, the 5 yr ended the day at 1.50%, and the 10 yr at 2.56%...once again we EXPECT to see at least the 30 yr selling tomorrow, hopefully the 10yr too....

Here are some quick economic data notes:

US initial jobless claims for the week ending November 29 came in just a hair better than expected at 509,000...down 21,000 from the prior week. Even though claims slowed, the four-week moving average increased to 524,500 which is the highest level since December 1982. Do you remember the 1982 recession? It was a nasty one!

October Factory orders fell off 5.1%...the largest decline in eight years

The CEO's of GM, Ford, and Chrysler were on Capitol Hill today. A positive feeling was taken away from the session when Senator Dodd (who is quite the comedian...funny car jokes Sen. Dodd...really good material you had today)..anyway he said he believed some sort of deal would be reached for automakers. This will help Stocks down the road, whether or not money is taken from MBS and moved to stocks...we don't know yet but we will say we don't think the stock lever is too tightly wound...mostly because the "invisible hand" is babysitting mortgages.( I hope someone catches my nerdy "Wealth of Nations" sarcasm)

I don't want to leave out the important mortgage/housing specific speech given by B52 Ben Bernanke...don't worry he didn't drop any bombs.

Ben used the Indy Mac loan modification strategy that FDIC Chairwomen Sheila Bair has aggressively pushed to be the foundation a potential recovery plan. Ben noted the plan could be modified in a way that might "increase the incentive of servicers to be aggressive in reducing monthly payments". The bad news is this will mean more government spending.

Ben also proposed some alterations and adjustments to mortgage insurance premiums for borrowers utilizing the Hope for Homeowners program. I am sure most of you who are retail, broker, and bank based lenders do not want to hear this sort of talk. Hope for Homeowners doesn't really appear to require the need for 3rd party originators. It appears that most lenders won't even allow a broker or correspondent originator to participate in this program. Is that the general sentiment?

This speech didn't make a lot of progress in our eyes...if you heard something we didn't please point it out to us.

The big event tomorrow is Non-Farm Payrolls. This number is expected to be brutal. We just need the data to NOT be more brutal than the already appalling anticipated numbers.

After yesterdays ADP report we expect job losses to be around 325,000-345,000 and the unemployment rate to be around 6.8 -6.9%. If the numbers are worse than expected I hate to say Treasuries could rally on...

AH YES THE LOCK FLOAT RECOMMENDATION....If you are super jumpy and feel satisfied with whats on your rate sheet right now then use the 101-00 on the FN 5.0 as your jump ship lock level. For short time floaters with a little bit thicker blood... you can continue to use the 100-25 price level as your bailout point. But only do so if the trend turns negative and the price of the FN 5.0 meanders its way down to 100-25. A quick sell off isnt a reason to panic in this "Quantitative Easing" environment.

I need to make sure everyone is aware of our longer term stance. We feel that Hank and Ben will make their presence known in Mortgage Rates World by continuing to artificially lower rates to the 4.00-4.50% level. I know I played the Devil's advocate but that doesnt mean we think Hank and Ben are just going to give up trying to save housing because guidelines are too tight or there isnt enough equity in homes. Investors havent passed through all the MBS gains yet....if you have some time to float.... we say let the float boat enjoy the wind a little longer