A "risk-off" environment helped bonds rally last week and led mortgage rates back into record low territory. Weak economic data around the world and continued "can kicking" in Europe sparked a sell-off in stocks and pushed the benchmark 10-year Treasury note yield below 2.00% for the first time ever.

In the week ahead investors will be searching for a bottom in both equities and interest rates. Stock markets are already set to begin the week more than 1% higher. The collapse of Muammar el-Qaddafi's hold on power in Libya has buoyed optimism - rebels took control of Tripoli, the nation's capital, and detained two of Qaddafi's sons. The main event in the day's ahead will however be the Global Central Bankers Conference in Jackson Hole, Wyoming.

"Global equities are looking to start the week on a positive note following another down week for stocks," said economists at BMO Capital Markets. The question on investor minds is, 'What Will Bernanke Do?' they added, looking ahead to the Fed's Jackson Hole meeting later in the week.

In MND's view, Fed Chairman Ben Bernanke will use the bully pulpit to begin laying the foundation for another quantitative easing program, which was already set in motion at the most recent FOMC meeting when the Fed downgraded its outlook with a significant change in monetary policy rhetoric.

The two-year Treasury yield is two basis points up at 0.21%, the 10-year Treasury yield is six basis points higher at 2.13%, and the 30-year yield is two basis points higher at 3.42%. The 2s/10s yield curve is 5 basis points steeper and production MBS coupons are 6-12 ticks weaker in price.

The S&P 500 is ready to open +1.96% at 1,145.50 while Dow futures are 1.55%% better at 10,928. MND sees rally resistance in S&P futures at 1150. Light crude oil is starting the week 1.35% higher at $83.37 per barrel. Gold prices are 1.22% higher at $1,874.50, on path to break the $2k mark sometime this month, for the first time ever.

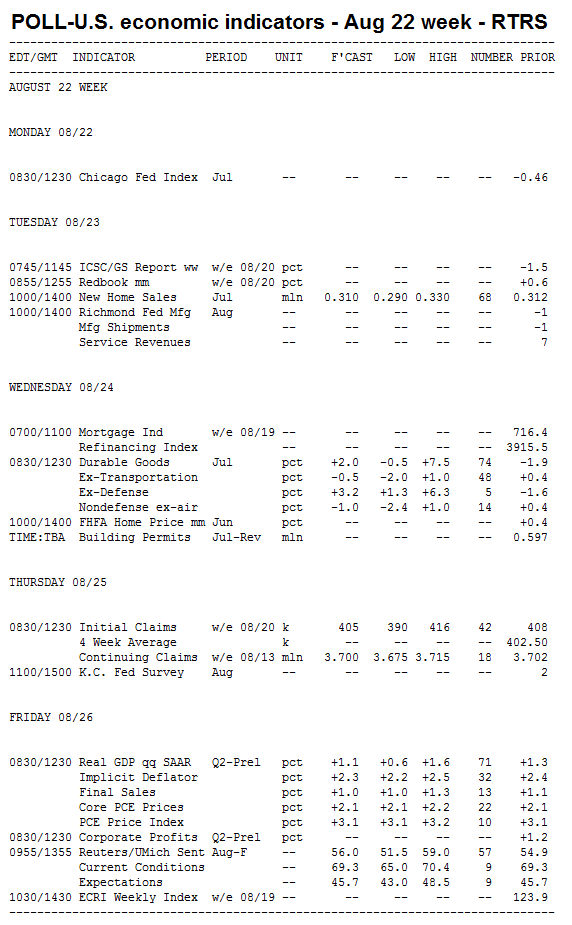

Key Events This Week:

Monday:

8:30 - The Chicago Fed's National Activity Index doesn't often receive much attention, but with the possibility of a double-dip recession on every investor's mind, it will be worth watching this time. The index, according to BMO, incorporates 80 economic indicators to provide a monthly snapshot of overall economic growth.

The June figure, released last month, was a lower-than-expected -0.46 and included a downward revision to the prior month. This month's figure is not expected to improve, and deterioration could confirm double-dip fears.

"A negative number means the economy is growing below trend," added BMO, noting the recession signal is a figure below -0.7.

Treasury Auctions:

- 11:30 - 3-Month Bills

- 11:30 - 6-Month Bills

Tuesday:

10:00 - New Home Sales are anticipated to continue scraping along the bottom in July, with no reasons for optimism in the coming months. The annualized pace of sales was reported at 312k in June and 315k in May; the consensus prediction for July is 315k.

"The number of new homes for sale is now the lowest in the nearly 50 years for which the data have been collected," noted economists at Citigroup. "With demand remaining at such low levels, we expect that builders will allow inventories to fall further."

Economists at Nomura Global Economics added: "Not only did mortgage application volume remain soft in July, building permits also declined. According to the Census Bureau, only houses sold prior to being built or those that are built for sale are counted as a new home sale, so softness in building permits in July would indicate weak new home sales."

Treasury Auctions:

- 11:30 - 52-Week Bills

- 1:00 - 2-Year Notes

Wednesday:

8:30 - New Orders for Durable Goods are expected to surge in July, but the major jump is due almost solely to the transportation sector, specifically to civilian aircraft orders and a moderate rebound in motor vehicle sales. The median estimate is for a 2% increase, with some estimates as high 7.4%, following a 1.9% cut in the prior month.

"One hundred 737's - that was the American Airlines order from Boeing on July 27," said economists at IHS Global Insight. "It was worth about $7.7 billion at book prices. If the planes appear in the government's orders data in this report, headline durable goods orders will be strong."

Optimism ends there. Excluding the transportation sector, forecasters assume a 0.4% drop.

"If the aircraft orders don't hit the government's books until August, then July will be a damp squib," IHS Global Insight says. "The aircraft leverage is massive, because the rest of the picture looks gloomy, with orders for non-defense capital goods ex-aircraft likely to fall 2.2% as June's seasonal surge in turbines orders disappears."

Treasury Auctions:

- 1:00 - 5-Year Notes

Thursday:

8:30 - Initial Jobless Claims disappointed markets last week by rising 9k to 408k, but the four-week average continued to fall, coming in at 402,500 - the lowest since mid-April. So the report continues to provide optimism that the nonfarm payrolls report for August won't be terrible. This week economists expect to see 400k new claims, with estimates ranging from 390k to 420k.

"The continued improvement in jobless claims despite downbeat data elsewhere is encouraging and moderately constructive for employment ahead," economists at Citigroup said. "Separately, beneficiaries likely were little changed, keeping the insured rate at 2.9% a third week. The insured rate has been largely constant over the last six months despite the uptick in the national rate."

Treasury Auctions:

- 1:00 - 7-Year Notes

Friday:

8:30 - Bad as the advance estimate of second-quarter Gross Domestic Product was, preliminary revisions are expected to be even lower. Economists anticipate April to May growth to come in at +1.1%, down from an original estimate of 1.3%. First quarter growth was even more dismal at +0.4%. With fears of a double-dip recession being the concern du jour, this report is sure to get a lot of play.

"We expect the big downward revisions to be to inventories and net trade," said economists at IHS Global Insight. "Nonresidential construction spending, state and local construction, and consumer spending should all be revised up. The figures will reinforce the picture of an economy barely maintaining forward momentum, and at risk of tipping back into recession."

"The mixture of revisions," added Nomura, "will likely include higher consumer spending and stronger construction of non-residential structures, which will be outweighed by a slower inventory buildup and a wider-than-expected trade gap."

Economists at Citigroup look for Q2 GDP at just 0.9%, owing to lower inventories and trade.

"Domestic demand actually should be adjusted higher because construction spending was marked up," they said. "Still, this report confirms that growth tailed off in the first half and that the weakness was not confined to temporary forces, such as bad weather, supply disruptions, and higher energy prices."

9:55 - Consumer Sentiment can't get much worse. At mid-month it fell from 63.7 to 54.9, the lowest of any point since May 1980. President Obama's approval ratings have dropped to new lows and markets have continued to be volatile, with the Dow Jones Industrial Average declining another 325 points, or 2.92%. Economists could hardly have been more wrong last time around; they now predict a slight uptick to 57, with forecasts ranging from 54.8 to 60.

"The second pass at August consumer sentiment will likely show no significant change," said forecasters at Citigroup. "The dramatic drop in early August came amid dramatic financial market turmoil. While the daily swings have moderated recently, the negative wealth shock to consumers remains large."

"Consumers face many headwinds such as poor job prospects, depressed home prices, high food prices, and volatile equity markets, while the European debt issue has reared its ugly head again," added IHS Global Insight. "Since the mid-August reading, the equity markets have been in a tizzy and fears of a global economic slowdown have increased. However, world oil prices have taken a major hit in the past couple of weeks and this will eventually offer some relief to household budgets at the gasoline pump."

10:00 - Federal Reserve chairman Ben Bernanke speaks to the Kansas City Fed conference in Jackson Hole. This is his first appearance since the Aug 9 FOMC meeting. His speech is titled "Near- and long-term Prospects for the US Economy."

"We do not anticipate that extreme measures, such as QE3, will be suggested in this year's meeting," said economists at Nomura, noting Bernanke used his speech last year to describe "additional stimulus" and then followed up by announcing QE2 a few months later.

"The deflation risks that were present at the time of last year's meeting are absent," they added. "We expect Chairman Bernanke to reiterate the Fed's tools for easing and seek to restore confidence in the central bank's ability to respond to shocks as they arise. He may also explain the role of the Fed's balance sheet - in terms of size and composition - in monetary policy."

MND GUIDANCE: If you missed the boat on record low mortgage rates last November/October, the opportunity is still out there for the taking. And we think you should jump on it as soon as possible. The risks involved in floating have greatly expanded to include (1) lenders taking it upon themselves to negatively adjust rate sheets (to slow loan production) and (2) interest rates finding a bottom and moving higher on their own. The frustration of missing out on "high 3's" and instead getting "low 4's" seems nowhere near as bad as the frustration of missing out on a refi opportunity (moving from 5% to 4.25% for instance) altogether.