Is the volatility over? Only a fool would say yes for certain, but so far, markets are calm.

Treasury movements are relatively modest. The two-year yield is one basis point softer at 0.19%, the 10-year yield is two basis points firmer at 2.28%, and the 30-year yield is three basis points firmer at 3.75%. The Fannie Mae 4.0 MBS coupon is -1/32 at 104-07.

Equities are on the rise which, if sustained, would mark the third day of gains. S&P 500 futures are 5.75 points higher at 1,182.50and Dow futures are 34 points higher at 11,284.

"Some stability appears to be returning to markets," said economists at BMO Capital Markets. "But businesses remain wary that the U.S. government isn't doing enough to arrest its massive budget deficit and that European governments aren't doing enough to avert financial contagion from infecting the banking system."

Light crude oil fell 0.56% from Friday to $84.90 per barrel, while gold prices stumbled 0.28% to $1,737.30.

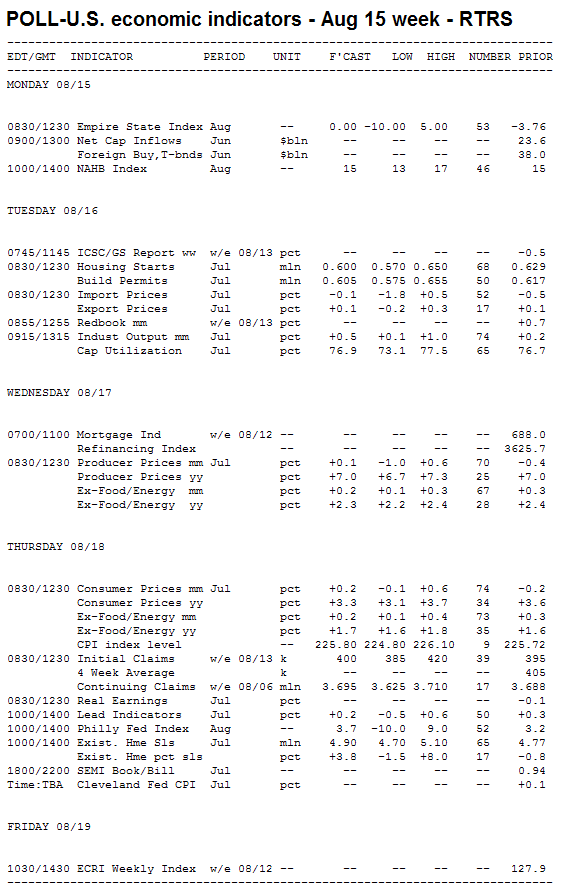

Key Events This Week:

Monday:

8:30 - Summer manufacturing has been weak in New York. The Empire State Manufacturing Index has contracted the last two months, with scores of -.3.8 in July and -7.8 in June, which are the only negative readings going back to November 2010. Whether this index digs out of contraction will set the tone of expectations for other regional reports to come this month. The median forecast just ahead of the release is zero; forecasts range from -10 to +5.

"The early-month timing exposes the August index to downside risks," said economists at Nomura Global Economics. "The July survey was conducted prior to the peak of anxiety over the debt ceiling impasse so those concerns could be reflected in the August survey."

10:00 - Keep your expectations for the Housing Market Index low, for it has provided no positive news for a couple of years. The index ticked up a decent two points in July, but the overall level is so low, at 15, that these moves can be safely be ignored until a true trend upwards is established.

According to Nomura, the index hit a record low of 8 in January 2009. So things have been worse. But only a score above 50 indicates that homebuilders are optimistic about the housing sector. We've got a long way to go.

1:25 - Dennis Lockhart, president of the Atlanta Fed, speaks on the U.S. economy.

Treasury Auctions:

- 11:30 - 3-Month Bills

- 11:30 - 6-Month Bills

Tuesday:

8:30 - It's tough to predict what will happen with July Housing Starts given that the June report was such a mystery. Housing starts somehow soared 14.6% June - beating forecasts by 12 percentage points - with single-family starts jumping 9.4% and multi-family starts rocketing 30.4%. The news was welcomed, yet the number of permits issued in the month, which tend to anticipate starts. rose only 0.2% and suggested the jump was only temporary.

Economists at Citigroup said this mismatch indicates a pullback in housing starts this month.

"The June figures for both single- and multi-family starts jumped surprisingly," they wrote. "However, fundamentals in housing have not improved materially and the recent weakness in the economy suggests that housing construction will remain soft."

Economists at IHS Global Insight added: "Our view is that the spike was probably a bad reading. For July, we are likely to see an offsetting drop."

The median forecast anticipates a drop in the annualized rate of starts to 600k, down from 629k a month before but still up from the 549k rate from two months previous.

9:15 - Warm weather, new manufacturing jobs, and auto assembly plants reopening should all help Industrial Production to climb 0.5% in July. The gain would follow a meagre 0.2% posting in June and a 0.1% cut in May. Second-quarter production had been disrupted by the earthquake-tsunami disaster in Japan, but motor vehicle output rebounded in July and suggests optimism for this index.

"We look for a huge rise in July industrial production, led by gains in motor vehicle assemblies," said economists at Citigroup, citing auto production and predicting a print of 0.8%. "Although plants were shut down for retooling for the new model year, production ramped up later in the month to a pace higher than before the Japan tragedy. The lift in auto sector output accounts for most of the expected gain in overall production."

Economists at Janney Capital Markets were a little more reserved, expressing much uncertainty about the report.

"The outlook for auto industry output, a major portion of the industrial production results, has gotten somewhat complicated by ongoing supply chain disruptions from the Japanese earthquake," they wrote. "Even U.S. auto manufacturers rely on parts produced in Japan, including many built in factories affected by the Sendai earthquake and aftermath. Adding to the complexity was an unusually hot July ... July was actually the fourth warmest month for the US ever recorded. We believe the auto and weather trends are mostly offsetting, however, and production will track relatively closely to its recent levels."

Treasury Auctions:

- 11:30 - 4-Week Bills

Wednesday:

8:30 - Expectations range widely for July's Producer Price Index. Following a 0.4% cut in July, the median forecast is +0.1%, and predictions go from -0.5% to +0.4%.

Economists at Nomura point out that energy prices increased in July but declined on a seasonally adjusted basis. Those at IHS Global Insight pointed out that "no big moves in energy or food items are anticipated this month."

So why the range of predictions? It may be due to the timing of the report.

"We think producer prices reversed last month's decline due to a pop in gasoline prices. Already, we see that the jump in energy prices will be short-lived," said economists at Citigroup. "But the PPI uses a mid-month to mid-month survey period, and during that time there was a notable price rise. Excluding food and energy, prices have consistently run in the 0.2% - 0.3% range, and that includes some recent, hefty increases in light vehicle prices related to shortages from the twin disasters in Japan."

1:20 - Richard Fisher, president of the Dallas Fed, speaks on Fed functions and monetary policy.

Thursday:

8:30 - July's Consumer Price Index isn't expected to produce major headlines. Economists forecast a 0.2% gain in the index, reversing a 0.2% fall the month before. With spending from consumers stagnant, inflation isn't much of a threat except for food and energy prices. Those are also anticipated to be tame this month, as gas prices declined roughly 0.5% in the month.

"Gasoline prices at the pump fell only slightly in July, while the seasonal factors expect a much bigger drop," said economists at IHS Global Insight. "That will translate into a seasonally-adjusted price increase for gasoline of around 5%. Food prices at the store should climb a bit faster, driven by rising prices for meat. Outside of food and energy, price increases should edge down to 0.2% from 0.3% in June, with a possible modest dip in clothing and accommodations after big increases last month."

Economists at Citigroup added: "If energy prices follow the path of current futures, the 12-month inflation rate will drop from the current 3.5% to below 2% by early 2012."

8:30 - This week's Initial Jobless Claims report aligns with the survey week for the monthly study compiled by the Bureau of Labor Statistics. Economists must be praying the result is in line with the recent trend.

The last report showed new claims fall 7k to 395k, the lowest figure since early April. Not just a temporary blip either, as the four-week average fell to 405k, its lowest since mid-April.

"The downward trend in jobless claims and better-than-expected job creation in July is at odds with the Fed's 9 August FOMC statement when it characterized the labor market as deteriorating," said economists at Nomura Global Economics.

10:00 - The Philadelphia Fed Survey has outperformed New York counterpart recently. In July it came out of an ugly contraction to report a score of 4.7, indicating a much slower rate of growth than earlier in the year while suggesting that, at least, that deterioration was over.

"A data release in line with our expectation would show that industrial activity continues to grow in the region, but remains markedly slower than prior to the 11 March Japan earthquake," said economists at Nomura Global Economics.

10:00 - July's Leading Economic Indicators index, a composite measure designed to track turning points in the economy, is expected to rise 0.2% following a gain of 0.4%. Recent turmoil in the financial markets began on Aug. 1 and so shouldn't show up in this index. That might be comforting, yet it also limits the value of this report.

Economists at Citigroup look for a 0.4% uptick.

"The healthy gain reflects outsized contributions from real money supply growth and the yield curve, as well as strong readings from jobless claims and stock market components," they wrote. "The increase was capped by weakness among consumer and business confidence measures, and a drop in building permits. If our estimate is correct the leading index strengthened on a year-to-year basis."

However, they look for deterioration in August thanks to financial market turmoil, lowered expectations for growth, and deployment of additional policy stimulus measures to stem the tide.

10:00 - The final data point of the week, Existing Home Sales, is expected to have something positive to say about July. The index was plagued by a wave of cancellations in the previous month, which cut the annualized pace of home sales to 4.77 million from a prior 4.81 million.

"Buyers are somehow failing to make it to the settlement table, perhaps stymied by credit problems," said economists at Janney Capital Markets. "While access to mortgage lending is relatively easy for prime credits, the number of foreclosures that have occurred over the last four years have effectively knocked 5% of potential homebuyers out of the markets - and that doesn't even consider the suddenly marginal credits of individuals who may have missed a few credit card payments or who are presently unemployed."

Assuming cancellations return to normal levels, the median forecast for July is 4.85 million, as economists predict improvement based on an uptick in contracts that have signed but not finalized.

"If there is risk to the forecast it would be to the downside in the event contract cancellations run high, as was the case in the June data," said economists at Nomura.

11:00 - Treasury will announce the terms of 2-,5- and 7-year debt to be auctioned in the following week

Treasury Auctions:

- 1:00 - 5-Year TIPS

Friday:

1:45 - Sandra Pianalto, president of the Cleveland Fed, speaks on "The Evolving Financial Services Industry and the Outlook for U.S. Economic Growth."