Equity markets soared in the final 110 minutes of trading on Tuesday, but optimism appears to have petered out overnight.

After the Federal Reserve released a statement after 2pm Tuesday indicating that policy would remain extremely loose until mid-2013, the market's initial reaction was a textbook flight to safety, magnified to exaggerate the point for the students who don't get it.

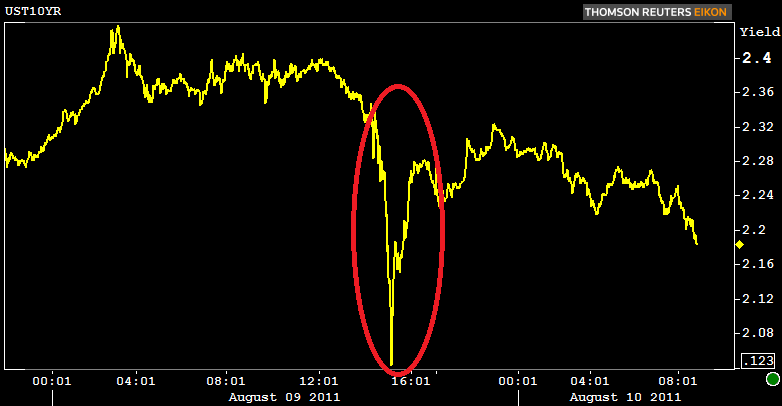

Equity markets, once up about 2%, dropped into negative territory as cash sprinted to safe havens. A graph of Treasury yields brought to mind Wile E. Coyote meeting a cliff: the two-year yield dropped 12 basis points to 0.16% (its lowest ever) in a matter of minutes, while the 10-year nearly broke the 2% barrier (its intraday low was 2.03%)

Within the hour, markets had completely reversed: Much has been written about the Dow finishing 429 points higher on the day, yet its 3.98% rally was the weakest of three indexes. The S&P 500 climbed 4.74% and the Nasdaq closed 5.29% higher.

Treasuries ended the day firmer but were nowhere close the highs of the session. The two-year finished at 0.20%, the 10-year at 2.27%, the 30-year at 3.64%.

The sense that markets had been oversold spread globally. In Asia, shares in Japan and Hong Kong rebounded 1.05% and 2.34%, respectively. In the ongoing European session, London's FTSE 100 was recently up 1.20% and Germany's DAX had ascended 2.20%.

But an early morning read Wednesday shows the market still hasn't found a clear direction.

The two-year yield is four basis points lower at 0.17%, the 10-year is four basis points lower at 2.24%, the 30-year yield is one basis points lower at 3.64%. And the Fannie Mae 4.0 MBS coupon is +17/32 at 104-07 after reaching a new record high of 104-12 yesterday.

S&P 500 futures are 20.00 points lower at 1,151.75, and Dow futures are 182 points off at 10,998.

Meantime, light crude oil jumped 3.64% overnight to $82.21 per barrel, while gold prices rose 0.91% to $1,758.80

Key Events Today:

10:00 - Wholesale Inventories grew 1.8% in May and were up 15.5% over the last 12 months. The June report is expected to see another large increase, at 1%, though there is "notable downside risk to this forecast because of the outsized jump in May of 1.8% and the delayed feed through of lower petroleum prices," according to Nomura Global Economics.

Economists at Janney Capital Markets warn about listening to perpetual optimists who can spin the inventory story both ways.

You'll see them "say that a) inventory builds mean future sales prospects are great or b) inventory liquidations mean that sales are ahead of plan and therefore we'll need more production to keep up," Janney notes. "That double standard is inherently unfair, and those optimists are claiming that inventory builds so far in 2011 imply stronger second half prospects. We disagree, as the builds could just as easily reflect slower-than-anticipated sales."

2:00 - Economic commentary on the Treasury Budget Statement for July is sparse. The median estimate is a deficit of $140 billion; estimates of the gap range from as little as $90 billion to much as $147 billion. These compare with a July 2010 deficit of $165 billion and a July 2009 deficit of $180.1 billion

"The budget deficit in July likely ran narrower compared with -$165 billion in the same month of last year because of strong corporate tax receipts performance during the month," said economists at Nomura Global Economics. "We forecast a July 2011 budget deficit of $147 billion."

Treasury Auctions:

1:00 - 10-Year Notes