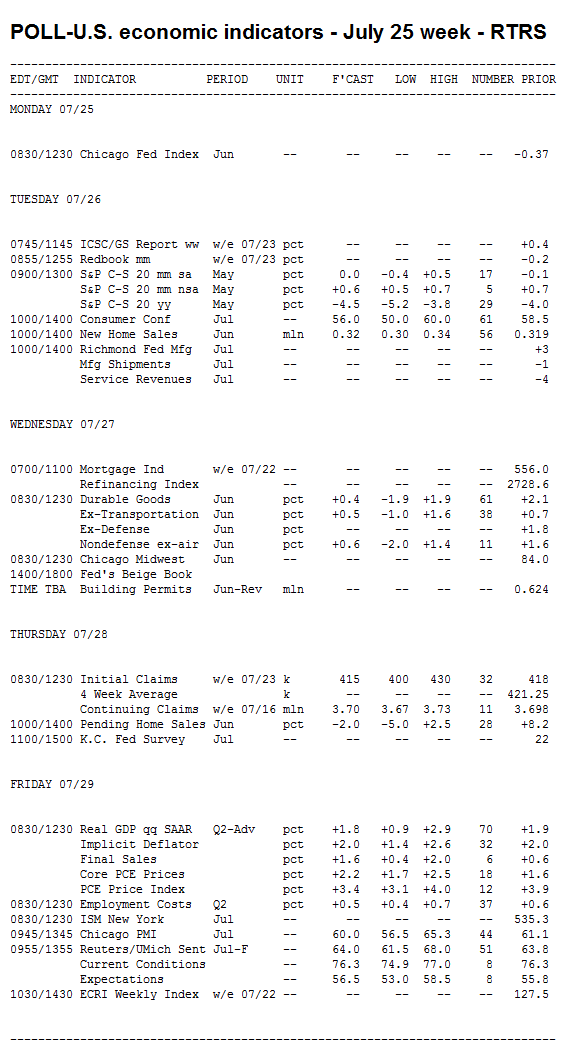

The debt ceiling debate is expected to be the primary mover of money in the week ahead. There will however be plenty of economic data to digest along the way. We'll hear how the weak June jobs report impacted Consumer Confidence. We'll get an update on home prices and sales. The Federal Reserve's Beige Book will provide an anecdotal summary of economic conditions across the country. Last but not least, a sneak peek at 2nd Quarter GDP numbers will print on Friday morning. And if that wasn't enough, Treasury will auction $99 billion in government debt (notes) between Tuesday and Thursday.

Even with a wide variety of scheduled reports and data on the calendar, the politics of money and banking are expected to steal the spotlight. U.S. lawmakers failed to compromise on a budget deal over the weekend and markets are not reacting favorably. Domestic stock futures are lower and benchmark interest rates are rising as a result.

The yield curve is bear steepening as longer-dated debt underperforms. The benchmark 10-year note is currently -14/32 at 100-30 yielding 3.015%. The 2s/30s portion of the yield curve is 4bps steeper at 391bps wide. 2s/10s are 3bps steeper st 260bps wide. The Fannie Mae 4.0 MBS coupon is -10/32 at 100-11. READ MORE: Rate Movers: Political Gamesmanship and Curve Spreads

S&P stock futures are -9.25 at 1331.75 while Dow futures are off 85 points at 12,542. Gold and the Euro are rallying.

Monday:

No significant data.

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

Tuesday:

9:00 - The S&P Case-Shiller Home Price Index is expected to post another gain thanks to seasonal boosts. Economists expect the index of 20 metropolitan home prices to rise 0.6% in May. That would put prices at 4.7% lower from the same level last year.

"Even though lower mortgage rates in recent months have improved homes' affordability, [the] supply and demand imbalance is a catalyst for further declines in home prices, which we see as likely to persist into 2012 at this point," said economists at Janney Capital Markets.

"The months' supply of existing homes up for sale remains even worse than in late 2010 and well worse than we had anticipated, suggesting that the price situation will continue to deteriorate well before it improves," they added. "Even the creator of the index, Robert Schiller himself, described the housing markets as 'stuck in the doldrums.'"

10:00 - Recent job reports expecting to their their toll on this month's Consumer Confidence index. The consensus view is for it to fall to 57.9, compared with 58.5 one month ago and 61.7 the month before.

"Consumers are being inundated with negative news about the economy and are faced with solutions to the debt ceiling issue that feature either tax increases, benefits reductions or both," explain economists at Citigroup.

"Little has happened in the way of good news for consumers," added forecasters at Nomura Global Economics. "Lower gas prices were quickly usurped by stock market volatility and the debt ceiling impasse. Confidence has slipped in the past few months and the early June sentiment survey showed further declines. We expect the consumer confidence measure to slide further to 55.2 in July."

10:00 - Expect New Home Sales to be roughly flat in June. The market forecast looks for an annualized pace of 320,000 home sales in June, just 1k up from last month and 6k down from April. Upside risks include strong building permit activity the last two months, offset by the recent decline in mortgage application volume.

"These sales have been in a range for the past year, slightly below the levels right after the recession," said economists at Citigroup. "However, we anticipate that sales will remain toward the high end of the range, given the uptick in housing starts and the small pickup in the housing market index, which signaled that homebuilders are seeing slightly better sales. ... Demand is still running below supply. This would be the fiftieth consecutive month of declining inventories."

2:00 - Thomas Hoenig, president of the Kansas City Fed, will speak before the House Financial Services Committee's Subcommittee on Domestic Monetary Policy and Technology. His talk is on "The Economy and Monetary Policy."

Treasury Auctions:

11:30 - 4-Week Bills

11:30 - 52-Week Bills

1:00 - 2-Year Notes

Wednesday:

8:30 - Coming off a strong 2.1% jump in May, New Orders for Durable Goods are only expected to rise 0.3% in June. Recent strength has been helped by Boeing but economists have mixed views about its sales this month following the 49th Paris Air Show. To escape volatility from a possible drop in aircraft orders, economists will look at the ex-transportation component; this month it is anticipated to climb 0.5%, following a 0.7% gain the month before.

"Durables orders have remained one of the relatively few bright spots in US economic performance though the current summer soft patch, adding on about 7% year to date, with 2% of the orders expansion coming in May alone," said economists at Janney Capital Markets.

Added economists at Citigroup: "Durable goods orders likely were little changed in June, after some wild swings thus far this year. But the stability in the expected headline figure masks a decline in the turbulent transportation sector and a healthy increase in the more stable ex-transportation series. Once again, a drop in aircraft orders likely dominated the change in transportation orders, but a rise in motor vehicle assemblies probably tempered the downswing."

An opposite read comes from Nomura: "Durable goods orders should get a bit of a boost from additional orders placed at Boeing in June. The value of orders in categories such as primary and fabricated metals is expected to be held back somewhat by lower commodity prices. Overall, we expect durable goods orders to have increased by 0.8% in June, ex-transportation increasing by 0.6% and ex-defense by 0.3%."

2:00 - The Beige Book, the Federal Reserve' anecdotal summary of economic conditions across the country, should reflect another poor month of employment gains and give some much-needed commentary on where the manufacturing sector is following supply-chain disruptions from Japan.

Treasury Auctions:

1:00 - 5-Year Notes

Thursday:

8:30 - Initial Jobless Claims jumped 10,000 to 418k in the week ending July 16 - the survey week for nonfarm payrolls. Early July can be a tough time to glean the data because auto plants tend to shut down for retooling, thus skewing the numbers, but the eight weeks with a four-week average above 420k gives some idea of many people are continuing to lose their jobs on a weekly basis.

"Initial jobless claims probably fell by 8,000 after an above-forecast rise," said economists at Citigroup. "Now past auto factory shutdowns and the Minnesota budget impasse, the figure hopefully should be a clearer gauge of underlying employment activity. If our estimate is correct, the four-week moving average retreated to the lowest level since mid-April."

10:00 - Economists anticipate the Pending Home Sales Index to shed 2% in June. How helpful this index is a matter of debate right now. In April it posted an 11.3% decline, only to post an 8.2% recovery the following month. By those standards, a 2% decline looks stable.

"Part of the April weakness appears to have been due to inclement weather/flooding in the Midwest and South, so we were not surprised to see a significant recovery in the following month," said economists at Deustche Bank.

Deustche Bank noted that contract signings are recovering swiftly and were up 13.4% from year ago levels.

"Pending home sales rose strongly in May and across all regions," added economists at Nomura Global Economics. "The pending home sales index typically has up to a two-month lead-time over existing home sales and MLS listings suggest another increase in this metric in June."

12:45 - Jeffrey Lacker, president of the Richmond Fed, speaks on economic recovery.

2:30 - John C. Williams, president of the San Francisco Fed, speaks on the economy.

Treasury Auctions:

1:00 - 7-Year Notes

Friday:

8:30 - The key release this week is second-quarter GDP. Unfortunately, it's not key for its ringing endorsement of economic optimism. Citigroup analysts said Q2 GDP "will likely show that the first half of 2011 was the worst two-quarter period since the beginning of the recovery." The consensus forecast expects quarterly growth at 1.7%, annualized

"The rather thorny results we are anticipating from next Friday's second quarter growth figures are apt to have a somewhat chilling effect on economic sentiment," said economists at Janney Capital Markets, who mention stalled consumer spending activity, significant weakness in housing investment, and a downward trajectory in government spending, and uncertain exports.

"The details of the report are likely to show a gloomier picture of the economy," added economists at Nomura Global Economics. "If our expectations are met, more than half of real GDP growth in Q2 came from inventory accumulation rather than an increase in final demand. We expect real personal consumption to increase by only 0.6% q-o-q."

9:45 - The Chicago Business Barometer, an index of the services and manufacturing industries, is expected to remain at robust levels in July. The mean prediction is 60.0, down slightly from 61.1 a month before but a full 10 points above the growth threshold.

"Business activity in the Chicago area has been more robust than the national average, and apart from the May reading has not shown any weakness associated with the overall economic slowdown in the first half of the year," said economists at Citigroup. Even the May reading wasn't bad at 56.6.

9:55 - There's little reason for Consumer Sentiment to improve with daily headlines warning the U.S. could lose its AAA ratings or even default on its debt. The outlook is shaped by fewer government services and higher taxes, coupled with estimates that unemployment will remain elevated for the coming years. So don't be surprised some economists are projecting this sentiment survey to fall to 56.5 from 61.1 a month before. The consensus estimate is a higher though, at 60.

"The May and June payroll numbers were very disappointing, personal income growth has slowed down, and core price inflation - inflation excluding energy and food prices - has increased," said economists at IHS Global Insight. "Stock market volatility and the dismal state of affairs on the housing front are pushing household net worth down as well. The only good news has been the recent drop in gasoline prices - which reached $4.00/gallon in mid-May and now stand at $3.74/gallon. In July, however, gasoline prices have edged upward."

10:00 - Residential Vacancies and Homeownership data for the second quarter 2011 will be released

ONGOING GUIDANCE: Floating in this environment is a crapshoot. Both stocks and bonds are maneuvering through major market uncertainties. Market participants are focused on news headlines regarding U.S. budget issues, EU debt contagion concerns, and financial earnings. That puts the direction of mortgage rates at the mercy of factors which don't exactly adhere to schedules or expectations. Yes there's still room to float longer term deals, but if home loan borrowing costs start to rise in the near future, it won't be long before Best Execution rate quotes are being pressured higher, making us more inclined to advise locking short-term floats (those that must lock in less than 15 days).

CURRENT GUIDANCE: Until/unless we see bond markets get back to a stable or improving pattern, risks vs. rewards favor locking. See our Ongoing Guidance above...