A "flight to safety" led benchmark bond yields and mortgage rates lower last week.

Poor economic data combined with ongoing EU contagion concerns and three strong Treasury fundraisers all contributed to a bond market rally. Adding a little more uncertainty to the outlook was the U.S. debt ceiling debate, which once again failed to find positive progress as ideological differences among U.S. political leadership have led to a stalemate, prompting ratings agencies to issue credit rating warnings on U.S. debt securities. After writing this issue off as a "non-event" for most of the year, interest rate traders, especially those in the long-end of the yield curve, finally seem to be accounting for a potential short-term U.S. default. READ MORE

The "flight to safety" seems to be back in motion today as renewed debt concerns in Europe have the S&P 500 ready to drop 0.65% at the open while the Dow looks to shed 0.61%. The benchmark 10-year Treasury is starting the week four basis points lower at 2.87%, while the two year is slightly firmer at 0.355% and the 30-year yield was two basis points lower at 4.22%. Mortgages are lagging the Treasury rally. The Fannie Mae 4.0 MBS coupon is -2/32 at 100-23.

The most recent worries stem from the results of Friday's stress tests, in which the European Banking Authority suggested eight of the 90 participating banks had failed; the aggregate capital shortfall was nearly €2.5 billion euros. That news helped gold prices jump above the $1,600 per ounce mark for the first time ever. The precious metal's price rose 0.72% overnight to $1,601.60; if sustained, this would mark the 11th straight session of rising prices.

Amid all this turmoil, Goldman Sachs released a note announcing it had cut its estimate for U.S. GDP growth in the second and third quarters. The bank now expects growth of 1.5% and 2.5%, respectively, down from 2% and 3.25%. And a good morning to you, too, Goldman.

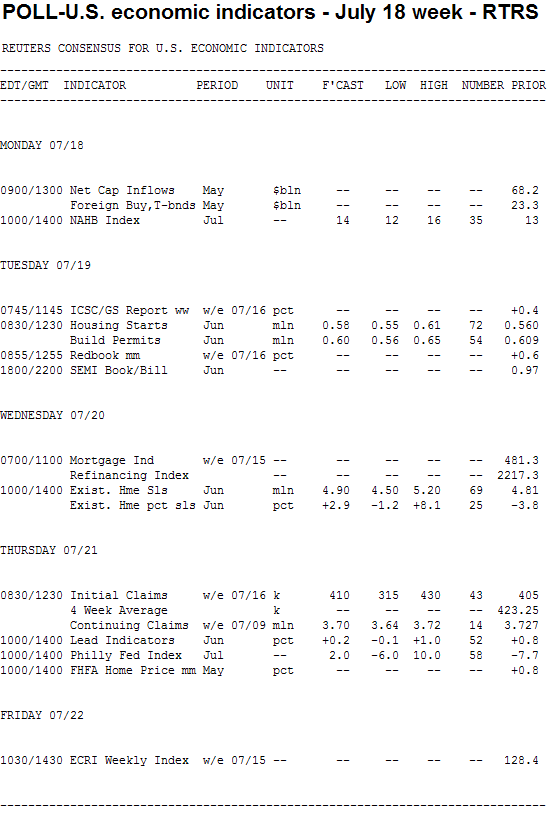

The week ahead holds little new economic data, leaving market participants to focus on U.S. budget issues, EU debt contagion concerns, and financial earnings.

Key Events This Week:

Monday:

10:00 - The Housing Market Index had been fairly steady at severely depressed levels for the past eight months and in June it fell another three points to 13, its lowest since September. Considering that a score of 50 indicates optimism, that drop was a very poor sign indeed. The index might rebound slightly this month, but until this index rises above to at least 20, there's little to gain on a monthly basis.

"The typical factors are to blame: weaker buyer demand and excess supply being the most evident, and leaving the value proposition firmly skewed away from new properties and towards the existing," said economists at Janney Capital Markets. "We see some effects of the homebuilding stagnation in the recent ratings downgrades of the only two (formerly) investment grade firms, Toll Brothers and MDC. With little reason for optimism on the horizon, we'd expect builder sentiment to remain below the 'neutral' level of 50 for at least several years to come."

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

3:00 - The monthly settlement process begins for Class C TBA MBS Coupons (GNMAs)

Tuesday:

8:30 - Economists are anticipating the pace of Housing Starts to jump to a pace of 575,000 in June, up from 560k a month before. The small improvement is to be led by single-family homes - the most important category - as well as multi-family units (permits for those structures jumped 21% in May).

"We look for a slight improvement in housing starts in June, led by single-family structures," said economists at Citigroup. "But starts should remain in the range that has existed for the past year. Although we anticipate a pullback in building permits, we do not see this as a fundamental deterioration. Multifamily permits jumped last month and we wouldn't be surprised by a reversal. Single-family permits have been fairly steady (at an extremely low level) since the recovery began and we don't expect much change in this trend."

7:30pm - Thomas Hoenig, president of the Kansas City Fed, on monetary policy and agriculture.

Treasury Auctions:

11:30 - 4-Week Bills

EARNINGS: Bank of America, Wells Fargo, Goldman Sachs, and Bank of New York Mellon will release their 2nd Quarter Earnings Statements

Wednesday:

10:00 - Existing Home Sales are anticipated to rise to an annualized pace of 4.9 million in June, up from 4.81 million in May. The Pending Home Sales Index, which looks at contracts that have been signed but not finalized, thereby offering a sneak peak of this index each month, jumped a strong 8.2% in May. Some economists are thus quite a bit more optimistic than the consensus, with forecasts as high as 5.2 million units.

However, "mortgage applications to buy homes declined in April, May, and June, suggesting that the PHSI may be overstating demand," said economists at IHS Global Insight. "Our call is that existing home sales probably increased 4% to a 5-million-unit annual rate in June."

Economists at Citigroup were equally nonchalant about the Pending Home Sales Index, predicting that existing home sales "likely remained range bound in June" as buyer traffic was weak.

Meantime, economists at Janney Capital Markets said the figures should get a boost from the recent decline in mortgage rates.

"Fannie May 30 year mortgage rates declined to an average of 4.23% in June, down from 4.59% in April, equivalent to a roughly 4% decline in monthly payments," they noted. "There's a lag between when lower mortgage rates begin benefiting home sales, but the supportive effects of these lower rates should start to show through in the June and July data. As a result, we're anticipating a meaningful increase in home sales from May's 4.81 million pace back up to the 5.0 - 5.2 million area for the coming two months. That's not enough to make a significant dent in the huge amount of inventory still on the markets, but it's a slow start to working through years of buildup."

6:15 - Federal Reserve Bank of New York Markets Group Vice President and FOMC System Open Market Account Manager Brian Sack speaks before the Money Marketeers of New York University.

Thursday:

8:30 - Initial Jobless Claims fell more than anticipated to an 11-week low of 405,000 in the period ending July 9. The 22k drop allowed the four-week average to fall 4k to 423k, but economists said little was gained from the report given the volatility and seasonal issues (i.e. auto plant retooling).

"We suspect the dip was more a function of strong seasonal adjustments - attributable to annual retooling in the auto industry during the 4th of July holiday week - rather than a signal of improvement in the labor market," said economists at Nomura Global Economics, echoing many others.

Economists at Citigroup noted that if claims stay at the same level this week, the four-week moving average would retreat to its lowest level in three months. Here's to hoping.

8:30 - Federal Reserve Bank of Chicago President Charles Evans discusses monetary policy issues in wire service media interview with Bloomberg, Down Jones, Market News and Reuters representatives,

10:00 - Most forecasters assume the Philadelphia Fed Survey will rebound into positive territory in July after dropping nearly 12 points to -7.7 last month. That wasn't just the first contraction since September, but the largest contraction since July 2009. But with auto manufacturing ramping back up in the third quarter, the mean estimate this month is +5.0; the range is from -4.8 to +10.

"The Philadelphia Fed's manufacturing survey showed weakness in June, despite reports of Japan supply lines beginning the process of normalization," said economists at Nomura. "We look for some improvement in July index to 2.5 from -7.7 in the prior month."

10:00 - Federal Reserve Chairman Ben Bernanke testifies on the Dodd-Frank Act before the Senate Banking Committee

10:00 - Leading Economic Indicators, a composite index designed to track turning points in the economy, is anticipated to rise 0.3% in July. That would follow a stronger 0.5% rise in June and a weak 0.2% decline the month before (both numbers were recently revised).

The largest contributors, according to Nomura, "will be the interest rate spread and real money supply, both reflecting the Fed's ongoing economic support," while "a decline in the stock market and consumer expectations are the notable negative contributors for June."

Economists at Citigroup look for a 0.5% gain.

"The biggest positive contribution was from real money supply growth, whose expansion in nominal terms was boosted by a decline in prices," they wrote. "The yield curve was once again a large contributor to the monthly gain. Otherwise, most gauges fell during the reference period, with the greatest weakness in consumer expectations and building permits. The projected monthly increase in the overall gauge likely lifted the year-to-year rate to 6.1%."

11:00 - Treasury announces the terms of 2-year, 5-year, and 7-year debt to be auctioned in the following week

Treasury Auction:

1:00 - 10-Year TIPS

EARNINGS: Morgan Stanley will release its 2nd Quarter Earnings Statement

Friday:

No significant events.