Indecisive investor attitudes carry over into the week ahead where two major events are seen shaping outlooks.

The U.S. Federal Reserve will conclude a two-day monetary policy meeting on Wednesday afternoon with the release of the FOMC Statement. We expect the Fed to confirm an end to its second Quantitative Easing program (QEII) and indicate that further quantitative easing measures are totally dependent on new economic data developments. The Fed's current stance calls for economic growth to pick-up in the 2nd half of the year. Also on our Fed radar is the outside chance for Fed officials to mention inflationary targets, but with inflation still seen as "transitory", there will probably be little to no change in their message.

The other market moving event on the horizon is the ongoing Greek debt crisis. Greek officials have said the country will face default by mid-July if the European Union and the International Monetary Fund do not release the next phase of bailout funds by then. Over the weekend Euro-zone finance ministers delayed a final decision on extending those emergency loan funds to Greece until they impose harsh austerity measures.

EU leadership issued this statement on Monday morning, "The assessment showed that debt sustainability hinges critically on Greece sticking to the agreed fiscal consolidation path, the plans of collecting EUR 50 billion in privatisation proceeds until 2015, and the structural reform agenda which will promote medium-term growth."

Since restructuring government leadership positions largely failed to improve national sentiment surrounding new spending cuts, Greek Prime Minister George Papandreou is now seeking government approval to enact his own austerity plan through a "vote of confidence", which will be taken on Tuesday night. Failing to agree on tough spending cuts would lead market pariticipants to believe the Greeks are not serious about making long-term concessions to pay back their debt. Also in the news, European Union leadership will meet at a Summit later in the week to make key decisions on boosting the EU bailout facility. The main mission of EU leadership is to avoid a "credit event" where Greece would be considered in loan default.

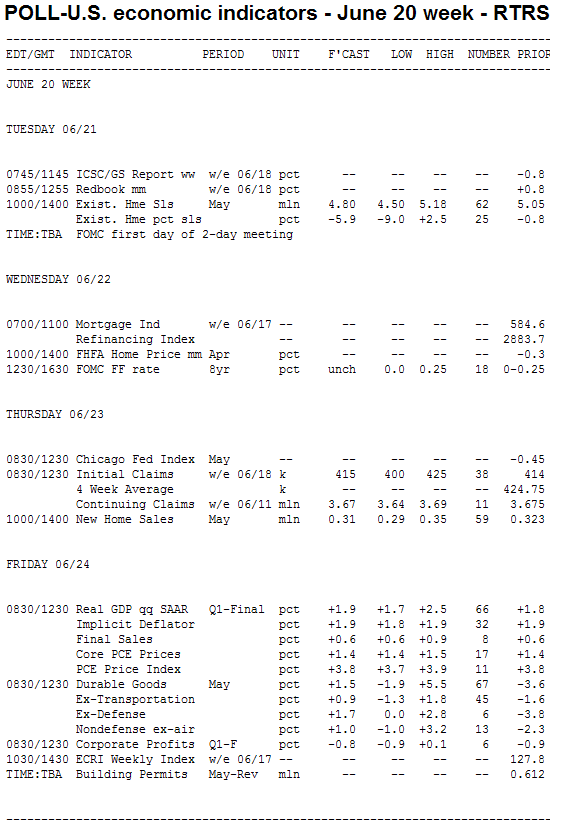

Other than those two stories, the economic calendar is pretty thin with no events on Monday and only Existing Home Sales on Tuesday. The FOMC Statement on Wednesday. Then on Thursday we get a regional business activity index (we got two bad updates last week) plus Jobless Claims and New Home Sales. The week wraps up on Friday with Final Q1 GDP and Durable Goods Orders.

The bond market is stuck in "wait and see" mode as stocks teeter on a major technical collapse. Trading strategies are very short-term in nature as investors are waiting for new directional guidance.

The 10-year

Treasury yield is beginning the week below 2.90% as equity

markets continue to bleed. The

10-year Treasury yield is more than four basis points lower at 2.8964%

in early trading. The two-year note yield is relatively stable at

0.37% and the 30-year Treasury is four basis points lower at 4.16%. The 2s/10s yield curve spread is 3 basis points tighter at 253 basis points wide. The Fannie Mae 4.0 MBS coupon is +5/32 at 100-27.

S&P 500 futures are poised

to begin the week 8 points lower at 1,257 while the Dow looks to

open 64 points lower at 11,874.

"Equities snapped a six-week

losing streak last week, but will need to deal with expected weak

housing market data this week and a rejection of further stimulus from

the Fed," noted economists at BMO Capital Markets.

Light crude

oil continued to plummet over the weekend, dropping 1.38% to a

four-month low of $91.73 per barrel. Gold prices declined 0.12% to

$1,537.30.

Key Events This Week:

Monday:

No major economic data.

Treasury Auctions:

11:30 - 3-Month Bills

11:30 - 6-Month Bills

Tuesday:

10:00 - The pace of Existing Home Sales is set to decline

in May after an unexpected 0.8% drop in April, which left the pace at

its lowest since February. This decline is expected to be steeper: the

consensus looks for a 6% downturn to an annualized pace of 4.75 million

units. With sales already down nearly 13% from last year, a rebound

isn't looking likely until June.

The Pending Home Sales Index,

which anticipates this index by looking at contracts that have been

signed but not finalized, fell 11.6% in April.

That alone implies

a double-digit percentage drop in May, yet mortgage applications to buy

homes were only 2% lower in May, implying a smaller sales decline,

according to IHS Global Insight.

"The wild card is how active

investors were in the market during the month," they said. "Our

projection is that existing home sales will drop about 6% in May to a

4.75 million rate, with investors playing a slightly larger role in May

than in April."

Economists at BBVA note that with forecasts

ranging from a 9% decline to a 2.4% gain, there is much uncertainty

surrounding the real estate market.

"Ample supply of price-

reduced or distressed properties should positively impact existing home

sales," they said. "Nevertheless, low consumer expectations, weak labor

markets, and downside price risk are pushing housing demand away from

ownership to a more defensive rental position. Therefore, we expect

existing home sales to decline on a seasonally-adjusted basis in May."

Treasury Auctions:

11:30 - 4-Week Bills

Wednesday:

12:30 - Following a recent speech wherein Fed chairman Ben Bernanke strongly implied that a third round of quantitative easing would not be in the monetary cards, the FOMC Meeting Announcement could be key in setting the market's tone this week.

"We

think the Committee will adopt more ambivalent language about the labor

market and current economic activity but will reiterate that it expects

a faster pace of growth to resume in the months ahead," said economists

at Nomura Global Economics. "The FOMC is also likely to acknowledge

that 'measures of underlying inflation' have increased but remain below

the rate considered consistent with the dual mandate."

Economic

data has only become worse since the late April meeting: unemployment

rose from 8.8% in March to 9.1% in May, core consumer price inflation

climbed from 1.2% to 1.5%, and GDP estimates fell to a 1.5% to 2% range.

Nomura

believes the policy statement must reflect those changes, as the

previous one called said recovery was "proceeding at a moderate pace"

and it called labor markets "improving gradually."

Bernanke's comments on June 7, that the recovery has been "frustratingly slow," is a little more up to date.

"The

key questions will be about how the Fed views the present combination

of weak growth and higher-than-expected inflation," said IHS Global

Insight. "Does the Fed still expect growth to pick up after a soft first

half? Is it still confident that the upward creep in core inflation

will be contained? And what would be the trigger points for growth or

inflation that would make the Fed change the status quo - either to pump

in more quantitative easing, or alternatively to start shrinking its

balance sheet and preparing for a rate hike?"

2:15 - Fed chairman Ben Bernanke holds a post-FOMC meeting press conference to elaborate on the policy statement.

Thursday:

8:30 - Initial Jobless Claims finally saw a decent-sized,

16k decline last week. Yet at 414k, claims were still above the 400k

mark the for 10th straight week. The median estimate looks for a smaller

decline to 410k this week, indicating that job growth in June is

limited at best.

Economists at Citigroup were slightly more

optimistic: "Initial jobless claims likely continued to retreat during

the week ended June 18. Though the four-week moving average remained

above the 400,000 threshold, it was still 20,000 below the mid-May

level. This bodes favorably for payrolls ahead."

10:00 - After posting a surprise 7.3% jump in April, the annual rate of New Home Sales is

anticipated to fall to 310,000 in May, down from 323k in April. Why the

change? Answer: why the gain in April? Economists point out it was

little more than statistical noise as the market for single-family homes

continues to scrape along the bottom.

"While improvements in housing starts and building permits add some upside risk to our May forecast, we do not believe these small gains give us sufficient reason to expect new home sales will break free of the relatively stagnant trend," said economists at Citigroup. "Construction activity increasingly has been driven by additions and alterations, rather than new dwellings. The low level of sales - both new and existing - suggests that people are choosing to stay in their homes. As a result, investment in renovations has not fallen much at all during the housing downturn."

11:00 - Treasury will announce the terms of 2,5, and 7-year debt to be auctioned in the following week.

Friday:

8:30 - New Orders for Durable Goods are

anticipated to recover with a 1.6% gain in May, following a 3.6%

setback in April and a 4.6% jump in March. The April losses were

attributed in part to "contagion effects" related to Japanese

earthquake, according to economists at Nomura, who point out that key

components for assembling cars became unavailable.

"The high-tech

sector also suffered from a disruption in the supply chain and orders

for Boeing's planes slowed to just two units," they added. "In May, we

expect a rebound from April's decline, though lingering effects from

Japan may still be evident. Boeing orders also improved to 27 units for

the month. We forecast that total orders rose with an increase of 1.2%

in demand for non-tranportation durable goods and a gain of 0.6% in

non-defense orders."

Analysts at IHS Global Insight added: "The

message from recent regional surveys is that manufacturing growth has

slowed sharply, but we will still probably see a rise in durable goods

orders in May, as some special factors that hurt April unwind."

Forecasts for new orders range from a 2.3% decline to a 3.5% gain.

Despite

recent volatility, analysts at Citigroup note the growth-trend "has

been fairly steady and solid" with core capital goods orders up 11% over

the past year and total orders excluding transportation up 7%.

8:30

- The final release of the week should tell a tale of slightly

better-than-assumed but still tepid growth in the first-quarter. The

"final" revisions to Q1 GDP are expected to bring the growth number up one-tenth of a percentage point +1.9%.

Economists at IHS Global Insight are much more optimistic than the crowd, forecasting a Q1 GDP figure at 2.5%.

"Almost

all of the new and revised evidence over the past month for the first

quarter has come out on the plus side for GDP - notably for inventories,

foreign trade, and consumer spending on services," they argued. "A 2.5%

growth rate for the first quarter would fit better with survey evidence

which suggested that the economy was doing well at the beginning of the

year - but it won't change the fact that all evidence is pointing to a

slowdown in the economy in the second quarter, when we expect growth to

be only around 2%."

CURRENT GUIDANCE: There's a weird feeling in the air. Stocks are teetering on a major technical breakdown and bonds smell fear but are waiting for new guidance to be offered. If stocks fail to mount a recovery rally in the near future, we could be looking at another leg lower in Best Execution mortgage rates. While this "feeling" ties together well with our long-term outlook, it's still speculative in nature. We say that because the timing of such a move is "at any moment". And until it happens, stocks are gonna put up a fight. This "scratching and clawing" in equities implies the potential for loan pricing volatility remains high. Remember, it was only last week when Best Execution Mortgage Rates were teetering on a shift higher because stocks had put together a decent intraday rally effort. We may have dodged a bullet, but we're not out of the woods yet. The past few days provide a perfect example of how quickly unfriendly fluctuations can occur in the mortgage market.